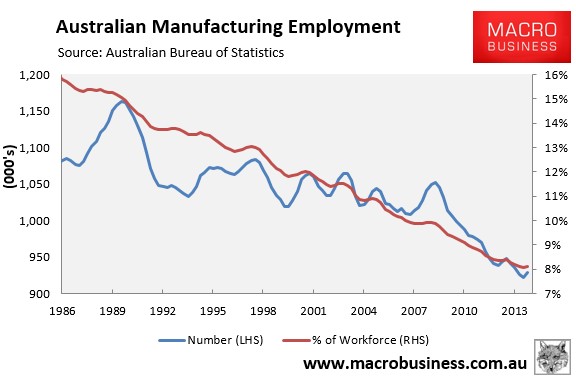

While the manufacturing sector continues to gasp for air, with manufacturing employment and capital investment both in the gutter:

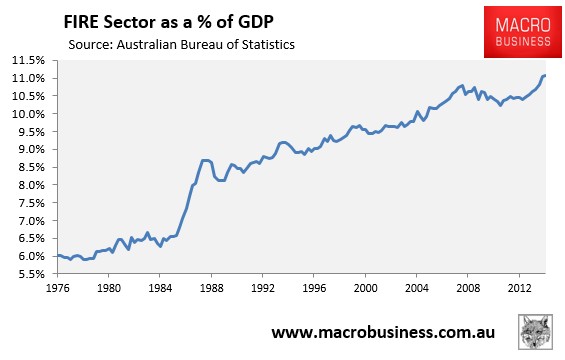

Yesterday’s national accounts release for the June quarter confirmed that Australia’s FIRE economy – Finance, Insurance and Rental, Hiring & Real Estate Services – continues to grow from strength to strength, rising to a new record high 11.1% share of the Australian economy (see next chart).

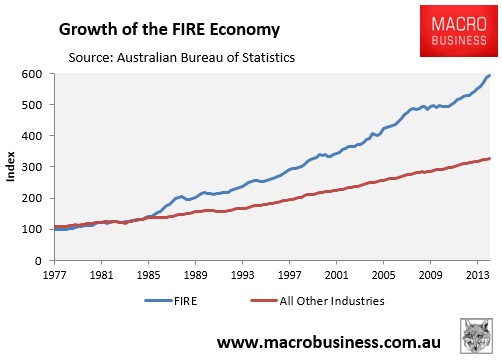

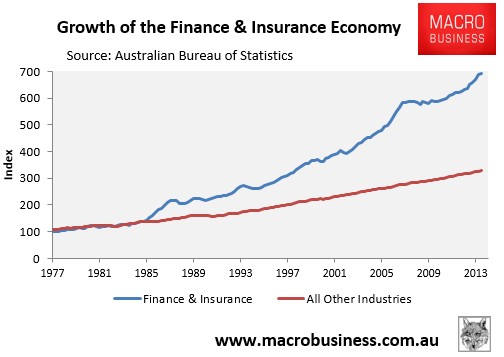

In fact, since financial markets were first deregulated in the mid-1980s, the FIRE economy has grown at nearly twice the pace of the rest of the economy:

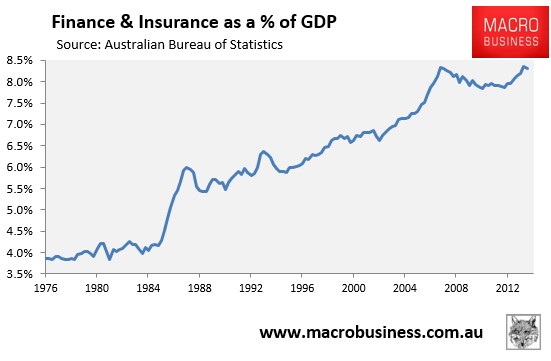

The situation is even more extreme if Rental, Hiring & Real Estate Services is removed from the mix, with the Finance and Insurance sector growing at well over double the pace of the rest of the economy since deregulation,, although is share of the economy (8.3%) is a whisker off the all-time high reached in the March quarter (see below charts).

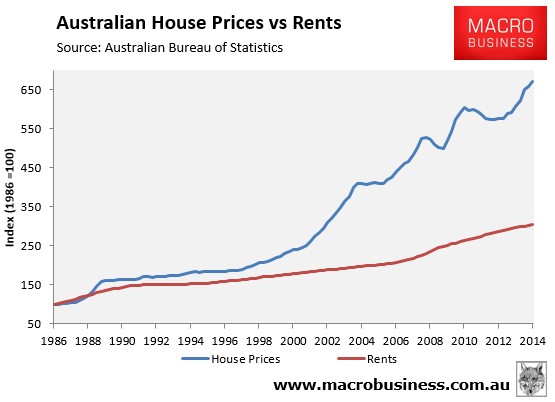

Anyone seeking an explanation as to why Australia’s FIRE economy has expanded so briskly only has to view the below chart, which shows Australian house prices decoupling from rents at roughly the same time as the FIRE economy’s growth decoupled from the rest of the economy (of course compulsory superannuation has also contributed):

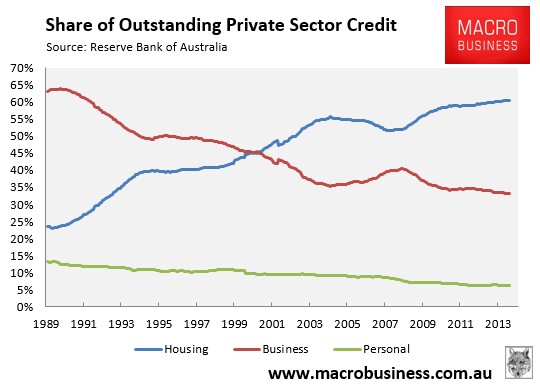

In short, the deregulation of the financial sector ignited credit growth, most of which has been channeled into housing at the expense of business, inflating Australian home values in the process:

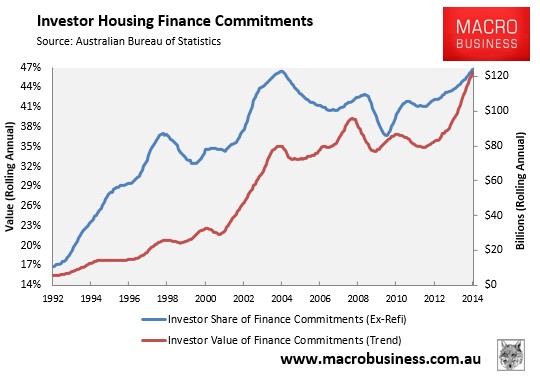

A key ingredient behind the surge in credit growth, house prices, and the FIRE economy’s growing share has been the explosion of property investors, whose absolute size and share has risen inexorably over the past two decades, and exploded over the past year, of course assisted by Australia’s peculiar tax laws (e.g. negative gearing):

And with overall housing credit growth expanding at 6.5% in the year to July 2014 – faster than nominal GDP (3.3%) – the FIRE economy is set to continue pushing to new highs.

Like Frankenstein’s monster, the financial sector, which once acted merely as an enabler of the productive economy, is now pulling its master’s strings, killing killing-off the productive economy in the process.