From the Shadow RBA today:

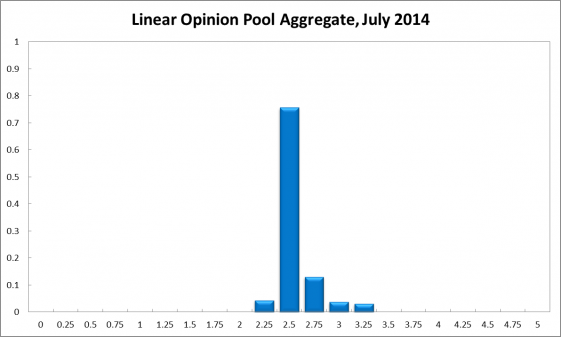

New inflation and growth data suggest that the RBA’s low interest rate setting ought to come to an end soon. Inflation is close to the upper target band, consumer confidence has bounced back from the temporary drop in May and GDP growth remains solid. Though some weakness in the labour market remains, the majority of Shadow Board members is arguing for an interest rate increase in the foreseeable future. That said, the CAMA RBA Shadow Board’s conviction that the cash rate ought to remain at 2.5% in August remains strong; it attaches a 71% probability that this is the appropriate setting. The confidence attached to a required rate cut has fallen one percentage point to 5%, while the confidence in a required rate hike has risen to 24%.

Headline inflation in Australia rose to 3% (year-on-year) in the second quarter of 2014, hitting the top of the RBA’s inflation target band of 2-3%. Core inflation in the same period has also edged up to 2.81%, suggesting that the increase in prices is broad-based. With domestic growth looking solid and other economic indicators (e.g. consumer confidence, business confidence, inventory stocks, private sector credit) pointing to a continuation of the economic expansion, the case for an increase in the benchmark policy rate is increasing. Furthermore, among the Board members, concern about inflated asset prices, resulting from low interest rates, is rising. The biggest factor holding interest rates in check appears to be the unemployment rate which currently stands at 6% and is unlikely to improve significantly.

The Australian dollar remains relatively strong, hovering around 93 US cents. Some uncertainty remains about the federal government’s budget, with the Senate unlikely to pass significant sections of the budget announced in May.

The global economy appears to be improving. US second quarter GDP roared back to 4% (annualized), after an unusually weak first quarter. This is supported by a further reduction in the US unemployment rate. The Federal Reserve is continuing with its phase-out of quantitative easing, and financial markets are beginning to price in an interest rate rise in the medium term. China’s economy is steadying; the European economies are still languishing, but not worsening. Some global risks remain, in particular geopolitical conflicts (Syria, Ukraine, Middle East) but also economic and financial problems (slowdown of the BRICS countries, Argentine default).

The consensus to keep the cash rate at its current level of 2.5% has fallen 5 percentage points to 71%. The probability attached to a required rate cut is up a percentage point to 5% while the probability of a required rate hike has risen to 24% (20% in July).

The probabilities at longer horizons are as follows: 6 months out, the probability that the cash rate should remain at 2.5% is unchanged at 47%. The estimated need for an interest rate increase equals 45% (41% in July), while the need for a decrease equals 8%. A year out, the Shadow Board members’ confidence in a required cash rate increase has risen further to 65% (61% in July), the need for a decrease fell to 9% (11% in July), while the probability for a rate hold slipped two percentage points to 26% (28% in July).

Note: Saul Eslake resigned from the CAMA RBA Shadow Board and did not vote in this round. His vacancy on the Board will be filled as soon as a suitable replacement has been found.

The comments of Warwick McKibbin over the past two months are worth noting. In July:

In my view current Australian interest rates are too low. The problem is that monetary policy is aimed at stimulating non-mining parts of the economy particularly housing construction. Monetary policy should focus on the growth rate of nominal GDP as a benchmark to guide interest rates. Given the current growth rate of nominal GDP of around 4-5 percent per year, a neutral monetary policy would be a risk adjusted interest rate of at least 4.5 per cent. Allowing for risk adjustment, this suggests the Australian policy rate should be closer to 3 per cent and possibly even 3.5 per cent. The current stance of monetary policy is at risk of increasing demand for assets, which will drive up the price of those assets. Unless there is a supply response, that will lead to pure capital gain and ultimately a bubble which will be costly to clean up. Australia faces a shift in global portfolio preferences towards Australian assets as well ultra-loose monetary policy in major countries that experiences a financial crisis causing a search for robust currencies. This means the usual channel of loose monetary policy through weakening the $A is no longer viable even if it was the goal. The focus on generating economic growth should be on the supply side of the economy through cost reductions (productivity improvements) improving competitiveness. There is not much a central bank can do about this except intellectual leadership in the debate.

And August:

With domestic goods price inflation rising to the top of the RBA’s inflation target band and asset price inflation clearly rising to uncomfortable levels the current policy interest rate in Australia is too low. Monetary policy is too expansionary. The dilemma for the RBA is how to get back to a more neutral interest rate given global policy settings. The strong Australian dollar will continue while foreign investors search for yield and the international adjustment of monetary policies continue to drive global currencies. Clearly the policy answer lies outside the domain of monetary policy. The current problem in Australia is in the settings of fiscal policy and the lack of appropriate structural adjustment policies. In a world of significant geo political risks and economic uncertainty the blocking of policy reform by the Australian Senate is making a bad situation worse by hurting consumer confidence. There is little that monetary policy can do to negate the near term and more serious long term economic damage caused by the current political standoff.

With respect, this is right in theory but falls down on the political economy. Put another way, the diagnosis is spot but the cure is wrong and is not outside of the domain of monetary policy. McKibbin has been arguing this European course of internal deflation for two years. His approach is much better than the German austerity model in that it endorses infrastructure spending to support growth during the structural adjustment but the problems are twofold:

- it is obvious that the infrastructure spend is going to be made on the basis of pork not policy rigour so any productivity dividend will be pot-luck if not entirely absent

- the debt needed to build the infrastructure will mostly rely upon implicit government guarantees (infrastructure bonds) and if projects are poorly chosen (with a lousy productivity payoff) then all they will do is add to the debt burden and problems when the AAA is lost.

The bubble is real and must be dealt with. The structural adjustment is vital. Quality infrastructure has a role to play. But the answer is macroprudential because it pushes the reform agenda back onto the government without relying on them to produce a solution they’re incapable of delivering.