It appears MB is getting through to the brighter elements of Australian economics. Stephen Walters of JP Morgan has penned a nice note sketching the outlines of what will be an historic event for the Australian economy:

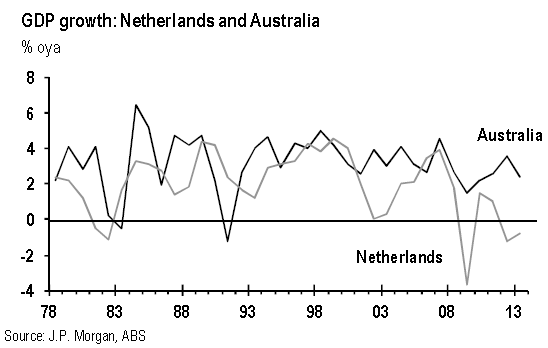

The Australian economy’s unprecedented golden era of growth without recession now stretches across more than two decades. We have reported 23 straight years of positive annual GDP growth, beginning immediately after what then- Federal Treasurer Paul Keating infamously called “the recession we had to have” in 1990-91. Only one economy in the modern era has managed to avoid recession for longer: the Netherlands, whose citizens managed a 27-year stretch of uninterrupted growth from the early 1980s (first chart). This impressive achievement, though, ended badly for the Dutch during the Great Recession and the subsequent Euro area crisis; after falling 4.2% during the great recession, real GDP in Europe’s seventh largest economy has fallen in nine of the last 12 quarters.

No such Dutch disease?

In Australia, there have been setbacks since the last recession, in which GDP has fallen in a discrete quarter, including during the global recession of 2008-09. There have not, however, been consecutive quarterly GDP declines to satisfythe accepted definition of recession. In fact, Australia’s economy has expanded in 87 of the 90 quarters since the end of the last recession. There have been three technical recessions in GNE, but never in GDP. Since the last downturn, Australia has managed the excesses and subsequentconsequences of a housing boom, China’s urban and industrial expansion, record-high commodity prices, and, recently, an unprecedented addition of capacity in mining.

Nimble policymakers can take much credit for this, particularly RBA Board members, who have been quick toadjust policy, most notably during the most recent global downturn. The RBA was the first central bank to slash official interest rates 100bp after Lehman Brothers collapsed in September 2008; others quickly followed. Fiscal policy’s automatic stabilizers played a role, too, both here and in China, in particular, which now takes one-third of Australia’s exports. AUD’s flexibility and the prevailing variable mortgage rate structure, which means the RBA gets a lot of bang for its policy rate buck, also have been helpful.

RBA: recession here has 100% probability

But this golden era can’t last for ever; Australia will suffer recession at some point. RBA governor Glenn Stevens told the Wall Street Journal last year that recession in Australia has a “more or less” 100% probability; only the timing is uncertain. Indeed, Australia’s economic history since federation in 1901 shows recessions occurring regularly, every seven years or so, on average. Deep economic downturns, in particular, have followed terms of trade bonanzas much like the one just experienced, albeit not since the abrupt end of the 1950s’ wool price boom. Indeed, Australia generally has not handled booms well; all previous commodity price-driven growth surges ended in busts.

We are, however, not forecasting recession this time around, nor are any of our competitors. Even the most pessimistic of forecasters expects only a period of sub-trend growth in Australia, as do we and forecasters at the Reserve Bank and Treasury. A crucial difference now is that AUD floats freely, and should fall to ease the economy’s transition as the terms of trade decline. AUD was pegged or managed until late 1983, meaning there was no timely pressure valve when trouble struck. Also, the base of the commodity price boom this time was broader—previously, it was all about wool.

Cause of next recession unpredictable

We do not pretend to predict the timing and cause of the next downturn. Will it be fueled by over-investment, as before the 1990-91 recession, or be triggered by a spike in interest rates, a policy error, or some other unexpected event here or offshore? We do not know, and nor should anyone guess. Policymakers don’t know either; if they did, they would adjust policy to help prevent recession, rather than merely jawbone and “lean into” emerging risks, as they are now. Instead, we have examined the economy’s apparent vulnerabilities and possible excesses, to gauge where the fallout from Australia’s inevitable recession most likely will be largest. These apparent pressure points will change over time, particularly if Australia manages to beat the growth record of the Dutch. For now, we find the household sectormost exposed, with leverage high, debt servicing costs elevated (despite record low interest rates), and house prices among the world’s most highest. This contrasts with the experience before the 1990-91 recession, which had its epicenter in the corporate world. The corporate sector this time around has performed better, although, until recently,

productivity growth was lame.

The oft-ignored benefits of recession

The apparent exposure of households, which we examine in more detail below, is the most obvious downside of Australia having avoided recession for so long. The absence of an economic trigger for change means many households will carry into the next downturn excesses that have built up over more than two decades. These will make the fallout from the downturn worse. We are not pro-recession; they are painful and destructive, usually causing unemployment to spike and wealth and potential output to be destroyed. Recessions do, however, have the benefit, often recognized only in hindsight, of triggering the necessary adjustment, a “clean out” that sets the sails for subsequent expansion. With the last recession receding into the deep past, many Australians have not experienced such catharsis first hand.

The likely prominent role for households in any downturn probably argues against the onset of catastrophe when recession arrives; bank failures, for example, as nearly happened in 1990-91, probably are less likely. It could, though, extend the duration of the downturn by constraining household discretionary spending over an extended period.

Indeed, unlike corporates, households de-lever only slowly.

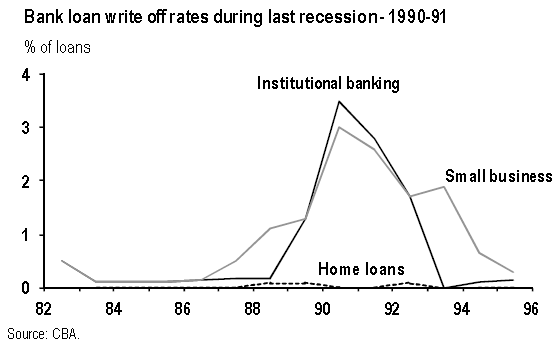

Corporate entities can raise capital from external sources more easily and/or pay down debt; also, bankruptcy protection can be a superficially attractive alternative. Households have fewer options. Most battle through toughtimes, continuing to make mortgage payments while cutting back on discretionary purchases. Household capitulation happens rarely. Even in the last recession in 1990-91, commercial bank loss rates (i.e., write offs) for home loans hardly budged at close to zero percent of outstanding borrowing (chart), but large corporate loan losses amounted to nearly 4% of all loans, and spiked to 3% for smaller businesses.

Last downturn fueled by over-investment

Australia’s recession of 1990-91 had its genesis in the heady days of the late 1980s, when a rapid rise in corporate leverage, encouraged by steadily falling interest rates in the wake of the 1987 share market crash, helped fuel an unsustainable binge in non-residential property investment, in particular (first chart above). Excluding mining-related engineering spending, non-residential construction ballooned from just 1% of GDP in the mid-1980s to almost 4% of GDP in 1989. As a result, corporate debt rose to a then-record 65% of GDP (chart, previous page). Subsequent increases in official interest rates as inflation approached 9% eventually ended the boom, triggering widespread bankruptcies and deleveraging— corporate debt tumbled to 50% of GDP by 1993.

Unfortunately, the onset of recession in some of the world’s major economies exacerbated the extended economic downturn in Australia back then. This inconvenience constrained the subsequent boost to Australia’s exports as AUD fell sharply. The local unit, in fact, fell from near 90 US cents in the late 1980s to below 70 cents by 1993 and nearly 21% in real trade-weighted terms. Australia’s export share,however, rose only modestly, from 15% of GDP in 1990 to 18% by 1993. Much of the lift in the relative export share wasdue itself to the extended weakness in domestic demand.

Corporate sector prudent this time …

The corporate sector has been much better behaved during the recent expansion. Corporate debt is elevated at 69% of GDP,comparable to the peak heading into the last recession 23 years ago, but down significantly from the record 78% reached in 2008, ahead of the global slump. Indeed, despite the Australian economy dodging a deep downturn back then when others did not, corporate entities managed down theirdebt in the aftermath. Local managers perhaps felt chastened by what was happening elsewhere, and acted accordingly.

Unlike the boom in commercial office space in the late 1980s, the recent boom in mining-related engineering construction was funded largely by offshore investors, limiting growth in domestic debt. Engineering construction surged from 1% of GDP in 2002 to a record 7% in 2012 as foreign equity investment via Australia’s open capital account swung from a net outflow of A$40 billion per year (2.7% of GDP) in the mid-noughties to a net inflow of A$60 billion (4% of GDP) in 2012. Also, corporates now are sitting on large piles of cash, which have been funding extensive share buybacks and other capital management activities. These most liquid of reserves could be diverted to other purposes if need be.

… but households carry excesses

The fallout from the corporate recession of 1990-91 extended to the household sector via a sharp rise in the jobless rate as businesses cut costs or failed, falling equity and house prices, which led to negative wealth effects, and the rise in debt servicing costs that squeezed disposable income. Back then,

unlike many corporates, households had been well behaved; household debt was just 50% of annual income, but they were not immune to the effects of the recession. Moreover, the rapid rise in interest official rates to 17% took households’ debt servicing costs to a then-record high relative to disposable income. The moderate debt ratio, though, meant that house prices equated to just 2.5 times household income, comparable to the global average.

Now, the household metrics are more worrying. Two decades of falling interest rates, steadily declining unemployment, and easing bank lending standards, alongside rising national income, have allowed household gearing to explode; the household debt to income ratio now is 1.5 times, three times higher than before the 1990-91 recession (first chart next page), and among the world’s highest. As a result, average house prices in Australia are more than five times gross household income, also among the world’s highest.

The housing market, then, would be vulnerable when recession strikes, although the full-recourse lending provisions here should limit the damage. Indeed, “jingle mail,” as unwanted house keys are returned to financiers, is an unfamiliar phenomenon for local banks. In fact, we forecast further gains in house prices, as there still is a shortfall of supply. That said, house prices can fall, as Governor Stevens recently reminded investors. Prices nationally dropped 7% from peak to trough during the 2008-09 global recession, when the real-economy impact of the global downturn were modest. The price falls were largest in the biggest cities, as was the case in the last recession in the early 1990s (chart).

Cross-border comparisons are untidy, as all markets are different, partly owing to differential tax treatment, but national house prices fell 33% peak to trough in the US after the great recession (second chart), 13% in the UK, 11% in New Zealand, 10% in Canada, and 35% in Spain, where they are still falling. Prices fell only 6% in the Netherlands.

Modest hikes will see debt servicing spike

High debt is a particular pressure point for households. The surge of borrowing over the last decade means it would take only modest mortgage rate rises to lift household debt servicing costs back to record highs seen in 2008. The forecast anticipates the RBA starting to normalize monetary policy from the current record-low cash rate of 2.5% in 3Q 2015. The first 150bp of official rate hikes, which we expect by the end of 2016, would take the household debt servicing ratio back above 10%, higher than before the early-1990s recession, assuming an unchanged household debt ratio. This also assumes the official rate hikes are passed through fully to bank mortgage rates, which seems likely.

A potential mitigating factor for the next recession, however, is that improved corporate fundamentals could limit the rise in the jobless rate. The forecast assumes only a modest rise in the jobless rate this year but that, of course, assumes no recession; the jobless rate reached almost 11% during the 1990-91 recession. Also, there is a large buffer of household mortgage pre-payments that the dominant variable interest rate structure allows; most households keep repayments thesame as variable interest rates fall. The mortgage buffer will be eroded quickly, however, as interest rates rise, and particularly so if unemployment later climbs rapidly.

Policy flexibility now more limited …

A complicating factor for when the next recession hits is that policymakers have less flexibility now than they did when recession last struck. The prevailing cash rate in 1990, for example, was 17%, providing policy makers (via the RBA, which was not formally made independent from government until 1996) with plenty of room to move when trouble struck.

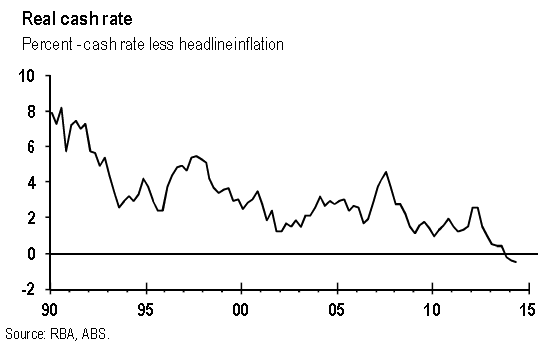

Now, the cash rate already is at a record low, although it probably will be higher by the time recession arrives, whenever that is. By then, the RBA will have started to normalize policy. Even after adjusting for inflation, the comparison stands. In 1990, the real cash rate was 8% (chart previous page); the real cash rate now is negative, for the first time in the inflation-targeting era.

Similarly, the government’s fiscal response to recession will be constrained. The Commonwealth budget deficit was less than 1% of GDP in the late 1980s, leaving room for the fiscal shortfall to blow out to nearly 5% of GDP as the automatic stabilizers kicked in. Now, due partly to extravagant (and largely wasteful, in our view) stimulus that played a small role in staving off recession five years ago, the deficit already sits above 3% of GDP. Rating agencies that bestow upon Australia the coveted AAA credit rating have called on the government to implement measures to return the Budget to surplus over time, further constraining any policy response. The agencies also have drawn a line in the sand on the public debt ratio at 30% of GDP, above which the credit rating could be under threat; it currently stands close to 20%.

… but AUD could fall sharply

Perhaps the pressure valve, then, would be lower AUD, which still sits proudly above 92 US cents, despite the plunge in previously soaring bulk commodity prices that helped drive the local unit above parity with USD two years ago. The incongruence between commodity prices and AUD reflects Australia’s now more prominent standing in the global AAAratedsovereign club, whose membership has been shrinking since 2009. The “curse” of the triple-A rating is that central banks and sovereign wealth funds now find AUDdenominated assets increasingly attractive, preventing AUD from falling, despite deteriorating fundamentals. The onset of recession, though, could see even these “sticky” investors head for relatively safer havens, triggering a fall in AUD that could boost exports, helping to cushion the damage done by recession to domestic demand.

Very good. Could have written that myself. The only point at which I disagree is the timing. I do think it will come this time around, following the next external shock, which is much closer ahead than the GFC is behind.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.