John Daley, CEO of the Grattan Institute, has given a fantastic critique of the generational warfare inherent in the May Budget, which left untouched the ridiculously generous entitlements provided to richer, older Australians. From News.com.au:

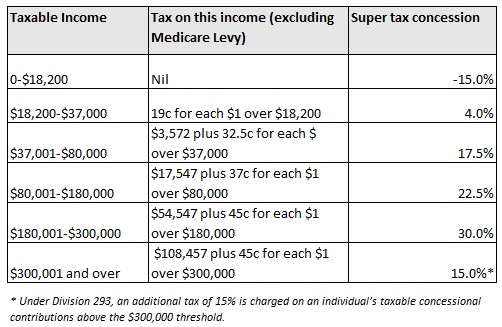

Mr Daley said people over 60 years old were essentially able to enjoy a tax-free threshold of almost $55,000 a year because of super tax concessions. This is because they are able to put up to $35,000 of their income (before tax) into super, it will not be taxed and because they are 60 years old they can withdraw this money at any time.

This is regardless of whether they were actually retired. They can still be working but they can benefit as long as they are registered as being in the “transition to retirement phase”. They can freely take money out of their super funds and potentially pay no tax on the super fund’s earnings for the rest of their lives. Everyone else pays 15 per cent on super earnings, as well as paying income tax on everything they earn over $18,200.

“If you think this is outrageous, then you’re right,” Mr Daley said. “Young Australians should be furious about this.”

Even the controversial Commission of Audit suggested this perk should be pulled back but “apparently super is sacred”.

Many older people are also enjoying a generous aged pension scheme.

“You have to ask, why did the inquiry into welfare in Australia look into disability and unemployment benefits, which are growing at about the same rate as GDP, but explicitly exclude the age pension, which costs much more and is growing at a faster rate?” Mr Daley said… the aged pension was not well targeted…

“You can have a house worth $5 million and other assets of about $1 million and still get a part pension, well someone with $6 million in assets is not doing it tough.”

Daley is 100% correct. While the Budget attacked younger people via higher university fees and tighter restrictions to accessing welfare, it has largely left wealthier older Australians alone.

That said, the Budget represents more than a case of generational warfare. Rather, it is class warfare, whereby the poor have been mostly targeted for cuts over the rich. It just happens to be that the poor tend to be younger, whereas richer Australians tend to be older.

This view is perfectly encapsulated by the Freedom of Information (FOI) request lodged by Fairfax Media, which revealed Treasury modelling showing the measures introduced in the May Budget would be highly inequitable and punish lower income workers:

The combined effect is that an average low income family loses $844 per year in disposable income (earnings after tax and government payments) due to the budget. Middle income earners forgo $492; while a high income family is down by $517.

As argued by Daley, instead of punishing lower income families and the young, the Budget should instead have targeted Australia’s world-beating and poorly targeted tax concessions, which tend to favour higher income earners and wealthy retirees.

Superannuation is obviously a large part of the tax expenditure problem. In addition to the issues inherent with over-60s effectively enjoying tax free income, the superannuation concession structure also provides the lion’s share of benefits to higher income earners, whilst ignoring (or punishing) lower income earners (see next table).

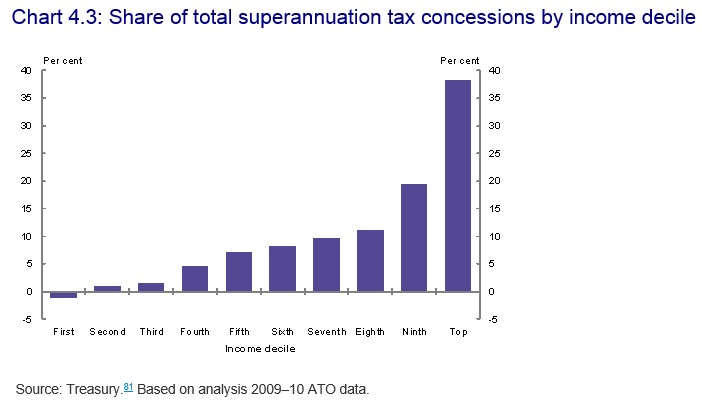

Hence, according to the Murray Inquiry into Australia’s financial system, “the majority of superannuation tax concessions accrue to the top 20 per cent of income earners (Chart 4.3). These individuals are likely to have saved sufficiently for their retirement, even in the absence of compulsory superannuation or tax concessions”.

The huge inequity of superannuation concessions, along with their massive (and growing) cost to the Budget, is the elephant in the room that the Abbott Government refuses to address. It is also a key reason why its Budget is widely viewed as being inequitable.

The means test for the Aged Pension is also way too lax. As noted by Treasurer Hockey on Budget night, “currently, an individual with a home and almost $800,000 in assets still qualifies for the age pension; a couple with a home and almost $1.1 million in assets also qualify for the age pension”. This level of taxpayer support is clearly more generous than necessary and allows precious tax dollars to flow to those that are not in genuine need.

All of which highlights why the Government must place superannuation and pension reform front-and-centre of its Budget repair job, with the principle aim of improving the equity and sustainability of the retirement system by ensuring that taxpayer assistance only goes to those in genuine need. Otherwise, richer older Australians will continue to receive a free taxpayer ride, while poorer segments of society (and the young, in particular) are required to shoulder the burden of Budget cuts.

A reform-minded government would also champion fundamental tax reform that broadens the base and shifts the tax burden away from labour and onto more efficient and equitable sources (e.g. land, resources and consumption), raising productivity in the process.

unconventionaleconomist@hotmail.com