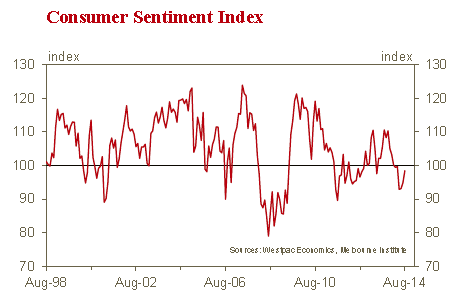

This is a pleasing result. The index is now only 1.2% below its level prior to the Federal Budget on May 13. Over the last three months the index has increased by a total of 5.9% indicating that much of the damage to confidence in the aftermath of the Budget has been repaired. However, the index has not reclaimed any of the ground lost between November 2013 and April 2014, when enthusiasm associated with a new government appeared to wane.

The Index is still around 10.8% below its post-election peak. There seems to be a number of politically-based factors that may be boosting confidence. Firstly, since the last survey it has been announced that the unpopular carbon tax has been repealed. Secondly, households have also probably been buoyed by resistance in the Senate to many of the unpopular Budget measures. It would seem that households are now assuming that some of these measures will eventually be moderated or abandoned. With the Senate set to reconvene on August 26, households will be anticipating a restructuring of the Budget that was released on May 13. If instead we see renewed disorder and indecision in the Senate, that runs the risk of dissipating this encouraging lift in confidence.

The rebound in confidence augurs well for a continuation of the lift in retail sales reported for June, which followed three consecutive soft months.

While the Reserve Bank did not cut interest rates over the month, some banks have been lowering rates for new loans, reflecting recent declines in market rates as the slowdown in activity has seen a reassessment of prospects for the official cash rate.

In August we saw the confidence of those households with a mortgage jump 12.8%. There were some significant moves in components of the Index.

The sub-index tracking assessments of ‘family finances vs a year ago’ increased by 11.9% to be only 4% below its pre-Budget level. The sub-index tracking expectations for ‘family finances over the next 12 months’ increased by 2.4% to be 7.3% below the pre-Budget level. However recall that immediately following the Budget announcement this component plummeted by 23% to record lows. More encouraging was the sub-index tracking expectations for ‘economic conditions over the next 12 months’ which improved by 8.3% to be only 0.5% below its pre-Budget level. The sub-index tracking expectations for ‘economic conditions over the next 5 years’ fell by 3.9% while the sub-index tracking assessments of ‘whether now is good time to buy a major household item’ increased by 1.9%.

Expectations for job prospects improved modestly. The Westpac- Melbourne Institute Index of Unemployment Expectations fell from 156.1 to 151.4 (down 3%). Recall that lower reads indicate reduced concern around the labour market. The index is now 7.9% below its recent peak back in March.

This gradual firming in the outlook the labour market has come despite news of a sharp increase in the unemployment rate from 6% to 6.4% in July. That information was released on August 7, mid-way through the August 4-9 survey period. We will probably have to await the next survey to get a clean read on the impact of this unexpectedly sharp rise in the unemployment rate. That said, households do appear to be gradually feeling more secure in their employment despite the negative reception to the Budget.

There was also good news for the housing market. The index tracking assessments of ‘time to buy a dwelling’ jumped by 9.7% to be 12.1% above its post-Budget read. Expectations for house prices have shown similarly gains with the Westpac-Melbourne Institute House Price Expectations Index rising 7.6% to be up 20.6% from its May read. This result is consistent with the boost in confidence we saw amongst respondents with a mortgage and may also be reflecting the lowering of some market interest rates.

The lift in confidence amongst respondents with a mortgage has come despite little change in outlook for interest rates. A clear majority of consumers still expecting rates to rise. The August survey found 63% of consumers expect mortgage rates to be higher in 12mths time, with 28% predicting ‘no change’ and just 9% expecting rates to decline. That mix is very similar to the last time we ran this question in February, which found 61% expected interest rates to move higher.

The Reserve Bank next meets on September 2. The Bank has made it clear in both the Governor’s recent statement and its August Statement on Monetary Policy that it expects the period of rate stability to continue. However it has lowered its growth forecast in 2015 from 3.25% (trend) to 3.0% (below trend). In theory that would imply its forecasts are pointing to lower rather than higher rates. We think the Bank is being overly cautious on the growth outlook. Specifically, the Bank’s forecasts do not indicate a lift in growth momentum through 2014. We expect the consumer to be running at a faster pace in the second half of 2014 than in the first with some spill-over to non-mining business investment and employment.

That prospect has certainly been boosted by this reported lift in confidence and the recently reported rise in business confidence. However, maintaining and lifting this confidence will be particularly dependent on a resolution to the current political discussions around the Budget that will resume on August 26.

It is our expectation that such a result can be expected and we remain confident that the next move in rates will be up, although not before the September quarter of 2015.

Bill Evans is getting ahead of himself in my view. Consumers have gotten over the Budget, yes, but the Government can’t just let it go. If it does not resume the campaign for cuts, by the time of the MYEFO later this year the outer years are going to be accumulating huge deficits, all the more so since the terms of trade are far lower than forecast already. As well, Q2 GDP is going to stink and housing is slowly slowing. The recent rebound in spending was just one month and was, to some extent, making up for earlier weakness when the winter arrived late. Smoothed out the year has been disappointing and will continue to be so. I expect employment gains will remain roughly where they are as the mining cliff offsets the services rebound.

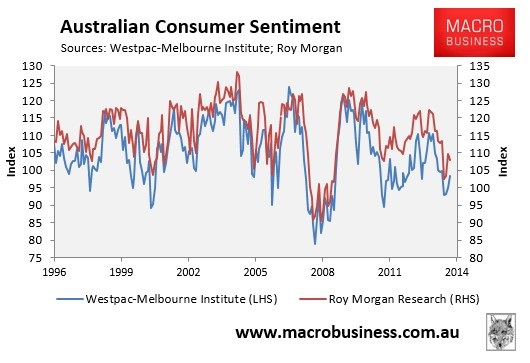

In sum, the second half will look more or less like the first and the RBA will be forced to cut in either October or November. Here the combined chart for RM and WBC measures:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.