Below is a guest post from MacroBusiness member, Phil Best:

Paul Egan and Philip Soos last week released an epic 800-page report entitled “Bubble Economics”.

Notwithstanding that parts of this report are excellent, I do hold deep reservations about their findings on urban growth containment policies and their distortionary effects. This paper contains a section 3.8 entitled “Examining the Urban Containment Hypothesis”, starting on page 657.

Below are my comments on their findings.

Egan and Soos claim that price volatility in urban land markets was a historical norm long before growth containment urban planning was invented. This is true; but they actually provide the reason why, and then “rebut” it:

“….an inability to build homes outside the immediate city centre given limited transport options; travelling by foot, horse, or carriage….”

Their “rebuttal” consists of the evidence of very high build rates for housing in the 1880’s cycle. But very high build rates on the limited amounts of land accessible by primitive transport systems would be a reason for price volatility, not a reason to expect it to be absent.

What Egan and Soos have missed, as have the important authors Harrison, Gaffney and Anderson who they cite, is the paradigm shift in land markets that occurred with automobile based development, which for the first time brought sufficient land within transport system reach, in the process diminishing economic land rent. Ed Glaeser gets it right in “Nation of Gamblers” (2013):

“…..The post-World War II era demonstrated exactly what textbook economics predicts should happen when robust demand meets relatively elastic supply. Quantities rose and prices stayed relatively flat. The relatively elastic supply owed much to the rise of automobile-based living on the urban fringe, which can be seen as either a shift in housing supply or a change in supply elasticity. For example, in an open-city formulation of the Alonso-Muth-Mills model, with supply costs that increase with density, lower transportation costs will increase supply but not change supply elasticity. Yet it is possible that the automobile made supply more elastic as well. On the urban fringe, lower cost, low density housing can be built in massive quantities, essentially using a constant returns-to-scale technology……

“……..The missing post-war price boom is not a problem for conventional economics, but it does present a challenge to those who seek to explain bubbles as the outcomes of a stable process where readily observable exogenous variables translate into the presence of a bubble. The 1950s had easier credit for homeowners than the 1920s and economic conditions were at least as good. Any model that suggests that there is a stable relationship between either of those variables and price bubbles has difficulties with this epoch……”

There was no lack of early authoritative literature theorising the coming fall of urban land rent from increased transport system flexibility. Robert Murray Haig (1926) “Towards an Understanding of the Metropolis” contained a sound and influential theoretical discussion. Michael Goldberg (1970) “Transportation, Urban Land Values, and Rents: A Synthesis” discusses Haig’s work and further refinements from Richard Ratcliffe, William Alonso, Lowden Wingo and other luminaries of urban economics.

Paradigmic changes to the system of transport, due to roads and automobility, interrupted the historical norm to that time, of urban land market cyclical volatility and systemic economic rent of an “extractive” nature. A new norm of cyclical stability in prices, the democratisation of home ownership and its amenities, and consumer surplus in housing rather than extractive economic rent, commenced and lasted for several decades in many first world countries. It was this “new norm” that was interrupted by centrally imposed planning to constrain the consumption of land in urban growth, eliminating the beneficial effect of competitive automobile-based land supply for urban economies.

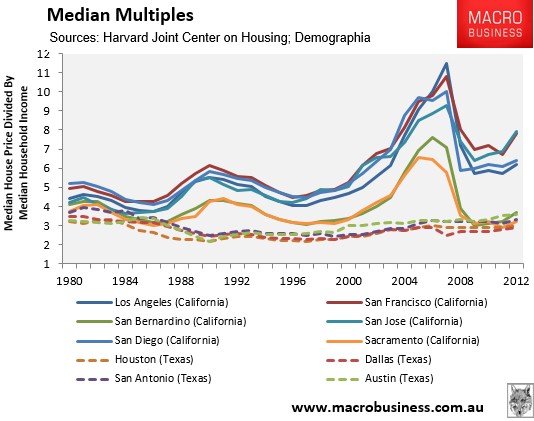

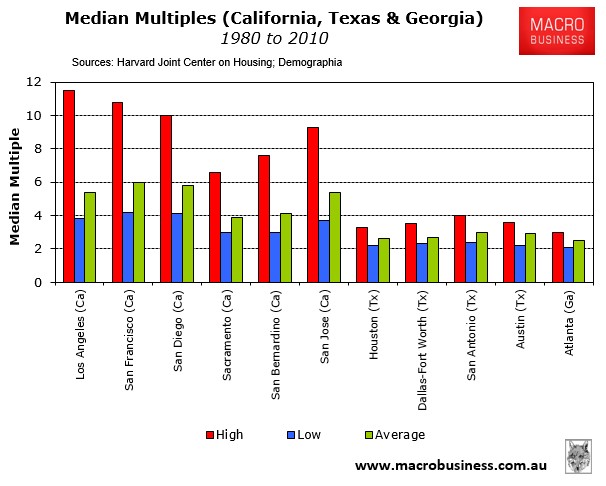

Egan and Soos use the example of Texas in the 1980s to demonstrate the presence of price volatility in the presence of freedom to convert land between uses. But as with other author’s discussion of this example (eg Phillip J. Anderson), nominal dollar percentage price rises and falls are used to make the volatility look a lot more impressive than if real prices were used. There was strong income growth in TX at the time. It is also worth noting that California, with more hindrances to conversion of land to urban uses, had a far greater price inflation at the same time.

The price falls in TX were significant due to overbuilding, which because it occurs without significant real price inflation, does not have to wreak the economic damage that happens when price volatility is high. And normality resumed within a few years as population growth caught back up to the quantity of housing. An occasional episode of overbuilding in conditions of explosive actual population and income growth is a small price to pay for urban land price stability.

In fact Phillip J. Anderson says of this episode:

“……In 1988 the comptroller of the currency, having surveyed all the recent banking and thrift failures, reported that less than 10 per cent of the failures had been caused solely by economic factors. Most were attributable to faulty lending practices or outright fraud…….” (Anderson, “The Secret History of Real Estate and Banking”, p284).

This contrasts with the highly destructive fallout from recent bubbles in which price movements have been far more volatile and even non-fraudulent loans to large numbers of borrowers have ended up in tragic negative equity situations – and with loan sizes that very much greater than a historically realistic assessment of the actual value of the property concerned.

Another crucial difference between this episode in Texas and the systemic changes in the markets in anti-sprawl regulated regions, is that in the latter, the volatility repeats and tends to worsen with each cycle, rather than disappear altogether (as it has in Texas); and furthermore the space per home in new development shrinks even as the median multiple trend entrenches at higher and higher levels.

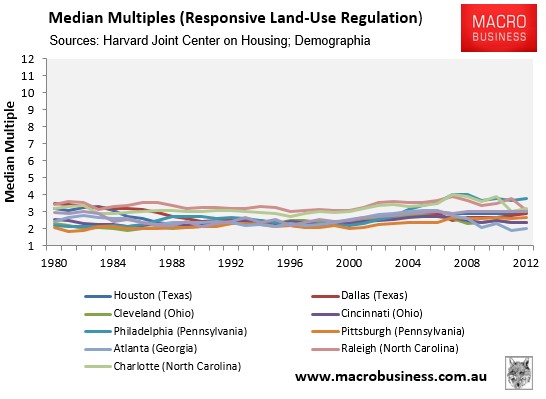

Bear in mind, too, that there are plenty of cities outside of Texas with growth rates that leave the growth-phobic parts of the world for dead, that do have price stability. Charlotte, Raleigh, Nashville and Indianapolis, for example (compare charts below).

There are analyses of housing supply elasticity by city in the USA that clearly show a major difference between the cities with freedom to sprawl and those without. (e.g. Green, Malpezzi and Mayo 2005; Albert Saiz 2010). The measured elasticity of supply in Texas’ cities are in fact not remarkable in the context of the elasticity that is the norm in the great majority of US cities. In Saiz’ study, none of the most elastic-supply cities are in Texas at all. Houston has a supply elasticity of 2.01; San Antonio is 2.26, Dallas 1.88, and Austin 2.41.

But Little Rock is 2.73, Kansas City 2.82, Omaha 2.83, Dayton-Springfield 2.91, Tulsa 3.02, Indianapolis 3.36, Fort Wayne 5.13, and Wichita 5.16……!

None of these cities have had the slightest tremor of real house price inflation in the automobile era.

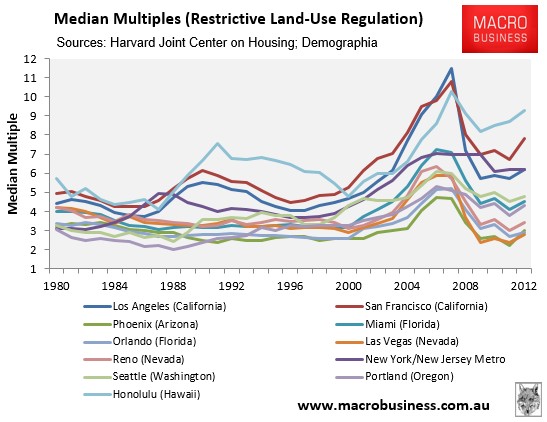

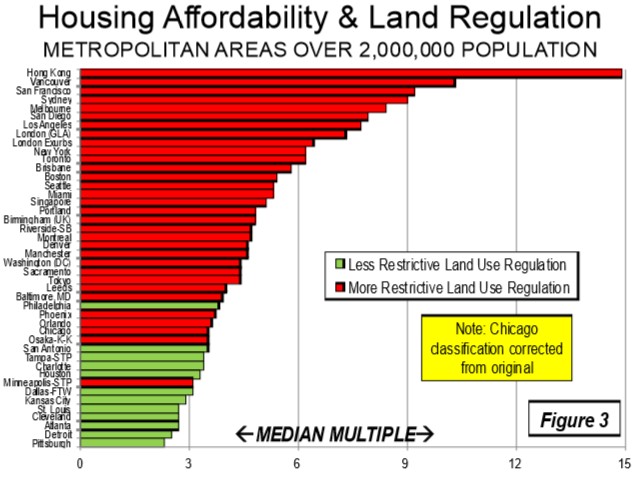

Egan and Soos use the classification of Chicago as a “less restrictive” land supply regulation city in a chart in a referenced Demographia Report. Unfortunately, this was an error in that particular chart; other references to Chicago in that report and all other Demographia ones are to it being “more restrictive”. Wendell Cox regrets the error, which has been corrected in the online edition of that report (see below).

Egan and Soos claim that prices and rents have an intrinsic relationship that should see them rise and fall in tandem if restrictions on housing supply play a role. But in real life, if amateur investors are cautioned about rental returns relative to the prices they are paying for houses, they will tell you that it is capital gains that they are chasing, not rental returns. Prices rising faster than rents is in fact one commonly acceptable piece of evidence that there is a bubble. The commonly understood price/earnings ratio on sharemarkets is a similar means of identifying bubble conditions.

A relative absence of institutional investors in the rental property market has been explained by the due diligence procedures of institutions, constraining them from taking risks. Amateur investors merely act on their own assumptions and wishes.

Egan and Soos point out, correctly, that leverage cannot be used to pay rents, but can be used to pay higher purchase prices. This is an argument against the necessity for rents and prices to move in tandem. They hypothesise that increased prices should be caused by increased rents, “capitalising into higher prices”, if supply constraints are the cause. As prices always rise ahead of rents when there are price inflation episodes, this, by their thesis, should mean that supply constraints are never responsible for the price inflation. This is an extraordinary position to take, given the range of severity of supply constraints in different housing markets around the world and the closely associated range of severity of economic land rent per unit of measurement of land.

If one takes the extreme example of London, UK, where the inflation of the value of a site gaining planning permission is fully 700-fold over rural values, (in contrast to a mere 20-fold in many cities with less strict rationing of land supply) and price inflation in every cycle has preceded eventual rent increases, how can one argue with a straight face that the supply constraints cannot be responsible for the price inflation? Yes, they will be and are responsible for inflation in real estate rents too, but these always lag the house price inflation.

In fact the only markets where rents and prices do remain in a stable long term relationship are the markets where significant price inflation and increases in economic rent per unit of land are absent. Both prices and rents tend to remain stable.

Soos and Egan’s central assumption, which is a common error, is that “there actually is an adequate supply of homes getting built, therefore the price inflation can’t be the result of inelastic supply”. The question I always ask such people is that if the supply of land for growing staple grains was strictly controlled in a lesser developed country, and “enough” bread was getting produced yet the price was so high that many people starved, and yet surpluses of it were going mouldy and getting dumped at sea; would the argument “but supply IS adequate” be regarded as a valid excuse that the controls on the land use were not responsible for a classic oligopoly price gouging ploy? The point here is that potential supply is not adequate – there is an absence of freedom for new entrants into the market other than by out-bidding existing actors, when in truly free markets it is possible to enter simply by “supplying” at a lower price, drawing on superabundant latent potential supply.

The glaring deficiency in mainstream economic analysis on this point concerns the market distortions caused by “quota” systems for the supply of anything. There is an added layer introduced into the market, or rather, an additional market introduced, between the factors of production and the consumer. This market is the market for share of quota. If government was auctioning the quota, government would capture the economic rent involved, as was the case for a short period with NZ’s car import license system in the early 1980s. But quotas can be created that give the private sector owners of the resource the power to extract zero-sum economic rent. This is the inherent problem with constraints on the conversion of land from one use to another.

In China, government actually is capturing the extractive economic rent created by strict control of the supply of land for urban development; in fact government is the “owner” of the land in the first place. They are deliberately maximising the “planning gain” (and ignoring housing affordability for now) because the revenue involved allows them to keep taxation of all kinds lower. The situation in the western world is similar only private sector rentiers are capturing all the gains, which are not helping the general interest by being a means of keeping taxes lower.

Egan and Soos complain about the shortcomings of classic urban land rent models in the literature from earlier eras (Alonso-Muth-Mills); yet all their criticisms of where the models are most inadequate are caused by distortions to markets that the classic authors were not attempting to incorporate in their models and possibly did not even foresee. The assumptions made by the classic modellers were largely true of an urban economy with no urban growth boundary (UGB) or proxy for one and minimal zoning, but are completely violated by the distortions introduced by an UGB. The principal effect of the UGB is the elimination of consumer surplus in housing, the creation of extractive economic rent, and the creation of expectations of capital gains. The owners of sites, therefore, do cease to act like rational actors who allocate their sites to productive uses, and behave more like speculators in gold and bullion.

Houston is an interesting case of a free-to-sprawl city that does not lack tall buildings in its CBD, which is logical given that more Fortune 500 Company Head Offices are located there than any other city. Yet Houston’s land rent curve is far flatter, and far lower at the CBD itself, than any typical UGB-contained city. In the latter, upzoning always increases site rents, often regardless of whether the site is actually redeveloped or not. However, in a city like Houston, building “up” tends to decrease floor rents, leading to decisions to build “up” being made on purely functional grounds, and prices and rents in the CBD being determined by fundamentals like agglomeration/productivity-derived income levels, not zero-sum economic rent extraction.

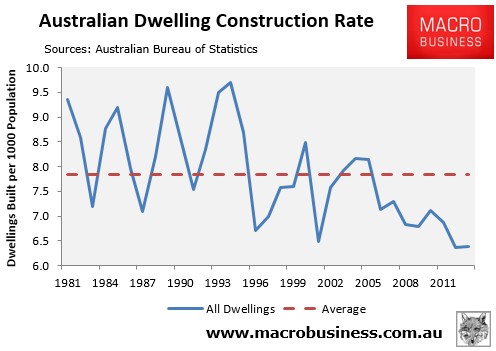

Egan and Soos claim that greater regulatory burdens on developers have not stunted housing construction rates. Whatever data they are relying on, it is not the dwelling construction data presented by the ABS:

In a normal functioning market, the massive rise in Australian house prices from the mid-1990s would have elicited a strong construction response. And yet, dwelling construction rates in Australia have fallen over that time, suggesting housing supply has become less elastic (responsive) to price.

Indeed, this recent study re elasticity of housing supply in Sydney, finds it to be below “unity”. Above unity means supply is elastic enough to stabilise prices. Most US cities elasticity in the above referenced Saiz study score around “2”. Studies for the UK find it to be indistinguishable from zero in many of their cities……!

Egan and Soos attempt to explain “land banking” and the withholding of sites from redevelopment to more efficient uses, in terms of the power of owners of land vested in them purely by location. That is, allegedly, this behaviour would be no different whether a UGB was present or absent. This completely ignores the role of “option values” in land in an urban economy. Travel cost can be traded off against location. Increasingly, travel cost has fallen in real terms, which is one of the factors that makes more sprawl inevitable (the other factor is that rural land has steadily fallen in price in real terms, enabling the conversion of more of it for the same amount of urban income). Communications have become an even cheaper substitute for travel, making location advantage less of a cause of premium pricing. Alan W. Evans (“Economics, Real Estate and the Supply of Land”, 2004) makes the distinction between economic “rent” that is due to location advantage, which he calls “differential rent”; and economic rent that is due to systemic scarcity, either real or induced by regulations. “Extractive” economic rent is the appropriate term for the latter.

It matters very much whether a site’s value embodies only differential economic rent or whether it has extractive economic rent in it as well. If the lowest cost land within functional driving distance of a site is rural land costing $30,000 per acre (entirely typical) then a site should not cost significantly more than the capitalised savings on travel on top of the $30,000 per acre. The fact that land just inside a UGB always sells for many times the rural value, while land in a comparable location in a city without a UGB always sells for a moderate percentage higher than rural value, should be conclusive for rational observers. The “option value” effect means that the value of all sites between the rural exurban land and the very city centre, are derived from capitalised travel cost savings relative to the rural land cost. There will be some price input from local agglomeration effects but these are still part of “differential” rent and can be quantified as an “add-on” to the lowest-cost land available to the urban economy – which is why those tall-building apartments in Houston CBD are so cheap.

Egan and Soos attempt to define a “more appropriate” approach to analysing whether a UGB causes housing unaffordability, than the allegedly crude identification of higher land selling prices (often 10 to 20 times higher; mostly over 100 times higher in the UK, and 700 times higher in London). They say:

“……..A study of the difference in land prices across the UGB must have two elements: a plot of land’s zoned use must be controlled for by rental income per square metre and measurement of the movement in the nominal rent to inflation and rents to income ratios over a specified period of time…… returns to residential land will always be greater. Land that is zoned for alternate purposes has different values, determined by the stream of capitalised income from the land’s highest allowable use, minus lot preparation and construction costs……..”

This is just at attempt to baffle readers with bunkum. Oh, we need to “control for the value of the stream of income in the highest-value allowable zoned use of the land”, to disprove that the zoning has an effect…….??? I would suggest this very same approach to prove that it does have an effect. The UGB creates extractive rent of an amount that seems to attach to each dwelling permitted; the higher the permitted densities, the higher the “planning gain” in the land. New fringe McMansions in growth-contained Boston, on mandated 1-acre minimum lot sizes, tend to be about the same price as new fringe row-houses in Manchester UK each on 1/20 of an acre of land; however, both are around double the price of the new fringe McMansion on 1 acre of land in a non-growth-contained city. The greater the permitted densities that go along with a UGB, the greater the “planning gain” to the site owner. Logically, this is why the rentier class likes UGB’s with upzoning even more than they like UGB’s without upzoning. The reason that affordable cities are affordable regardless of how low density they are (average lot size of 2/3 of an acre in new developments is common for median multiple 3 cities) is that the land value is anchored in “rural value plus cost of development and a modest profit in a competitive market”. When this means the developed land cost is under $100,000 per acre, then it obviously is not a make-or-break matter for affordability, to cram as many houses per acre as possible.

Egan and Soos quote literature from the US (Quigley and Rosenthal and others) regarding the complexity of land use regulation and how it is difficult to tease out the effect of each contributing factor, taking not merely UGB’s, but large lot mandates, height restrictions, set-backs, parking mandates, and so on, as “anti-growth” restrictions. This confusion by mainstream economists is common. But it does not require much time eyeballing data to see that the decisive factor is the ease with which rural land can be converted to urban use. As long as there are no restraints on this, it is indeed virtually impossible to tease out of the data, any effect on affordability from all the other “anti-growth regulations”. Median multiples seem to hover stubbornly around 3 in cities with freedom to convert rural land to urban use regardless of how much large lot zoning occurs. There is of course a limit to this – at some point in the “minimum lot size” scale, the effect must become literally a constraint on the conversion of rural land to urban use: for example, some US cities said to have “no UGB” are surrounded by rural municipalities who “do not disallow building of houses” but whose “minimum lot size” is 20 acres plus. This can be referred to as a “proxy for a UGB” or a “de facto UGB”.

Egan and Soos claim that private debt and property taxes are a glaring omission from land use policy studies, but in fact there is very little examples of urban land markets operating in either strict constraints on credit, or with land taxes. Both these policies are massively problematic politically. We do, however, have an example, South Korea, of severely unaffordable housing simultaneous with restrictions on credit that would make westerners squeal, such as LVR’s of 50%. All that this did was stimulate savings among young people, delaying marriage and childbearing until, in their mid to late 30’s, they could put down the 50% deposit, often with the assistance of parents. There is no evidence at all that house prices were constrained at all by the LVR policy. (See: Bank of International Settlements (2013): “Can non-interest rate policies stabilise housing markets? Evidence from a panel of 57 economies”).

There does not seem to be any correlation with the severity of property taxes, which have a land component, in US cities, and urban land price stability.

Egan and Soos refer to exurban “splatter” and “leapfrog” development in a couple of contexts; firstly in criticising the inability of the classical Alonso-Mills-Muth model to represent this reality and latterly in suggesting that urban growth boundaries are justified because they prevent this from happening. Actually, the classical Alonso-Mills-Muth model does somewhat include this reality because of the gentle slope of its land rent curve out into the surrounding rural land, from the urban centre. Splatter development tends to fit this curve reasonably well. It is a prohibition on splatter development that produces a curve with a serious discontinuity at the urban fringe.

Regarding the efficiency or otherwise, of splatter development patterns with later infill, this writer is aware of several specialist analyses that find this to be more efficient, not less efficient, and is unaware of any analyses that find the opposite, or of any rebuttals of this seemingly well-established principle. This is simply because later development of the fragmented land can have more efficient decisions made regarding its uses because of the existence of free-market evolution in the use of land around it already; new agglomerations can form that would not have formed otherwise, dependent on their need for affordable land, and indeed any spare sites at all where a nascent agglomeration might be forming (see Silicon Valley as the classic example); and because infrastructure planning and securing of rights of way is easier to do before areas are fully built out and yet while they are evolving. Growth containment policies are based on the assumption (that should have died with the former USSR) that central planners can anticipate the future needs of society and the economy better than what they would do if they follow the free market and act as enablers rather than prescribers.

Egan and Soos allege that critics of urban growth containment are possibly attempting to divert attention from the malfeasances of the finance sector and neo-liberal policies on immigration, globalisation and financial market freedom. But this charge could be reversed: it could well be finance sector rentiers as well as significant property rentiers, who are behind-the-scenes “bootleggers” to the growth-containment “Baptists” of the environmental movement. The crowning irony is that Egan and Soos claim that it is the “neo-classical economists” who are turning to blaming growth containment regulations, allegedly from lack of specialist knowledge on land economics, including a lack of understanding of “the private capture of geo-rent”…….! It is the contortions of theory regarding land values that Egan and Soos have presented, and the authors they quote in support, who truly lack this understanding in particular.

Egan and Soos end up making a plethora of recommendations that would be unnecessary if they understood and recommended that the priority reform concerns supply of land for urban growth. Many of the policies we now regard as toxic, are only so in combination with distortions to process of this supply. The many US cities with elastic housing supply, due to an absence of a quota mechanism in the land supply, do not experience negative unintended consequences from basically well-meaning policies like stimulatory low interest rates, the subsidy of first home buyers, tax write-offs of rental property operating losses, the welcoming of good quality immigrants, and the absence of a CGT on housing.

When new house prices are anchored in market freedoms in the same way as the prices of cars and TV’s are, low interest rates actually do stimulate the real economy; first home buyer subsidies actually do benefit first home buyers and increase home ownership; tax write-offs of rental property operating losses actually do encourage the supply of rental housing and enhance rental affordability; the need of increased supply of homes and infrastructure for population growth merely feeds economies of scale; and property capital gains in the long term are unjust due to inflation being the main cause for the “gains” taxed, and in so far as they are due to productivity improvements, they act as a disincentive to productivity improvements.

One of Soos and Egan’s recommendations, is abolition of the ability to write off rental property losses against other income, and imposition of rent controls to ensure that this loss of write-off ability does not result in rents increasing. This is a classic example of “the king, the mice and the cheese” effect in regulations – a regulatory distortion requires another regulation to fix it, which introduces another distortion, which requires another regulation, and so on ad infinitum.