Earlier this week, I posted an article, The Texas housing miracle, which once again argued that housing markets with responsive land/housing supply are both more affordable and less prone to bubbles/busts than markets where land supply is constrained by physical and/or regulatory barriers.

The article, whilst acknowledging other US states with similarly relaxed land-use regimes, singled-out Texas as possibly the best example of the benefits achieved from a highly responsive land/housing supply system, since its home prices have managed to remain both affordable and stable in the face of very high population growth (Dallas and Houston each added a whopping 1.2 million people each over the past decade!).

An alternative view put forward by fellow blogger, Cameron Murray and others, is that Texas’ stable and seemingly affordable housing has instead been achieved because of it’s high property taxes. According to Cameron:

…why do prices in Houston still appear so dramatically affordable?

One major reason is the relatively high property tax rate…

One would expect areas with higher property taxes to have structurally lower prices, reduced price volatility, and much lower price to income ratios…

…at lower interest rates a fixed percentage property tax leads to greater price differences. Therefore, over time, we would expect Houston home prices to be a smaller fraction of comparable homes elsewhere as the property tax differential has a greater price impact at lower interest rates…

Of course, this does not mean that housing is lower cost. It just means that cost of housing is borne by annual tax obligations rather than capitalised in the price…

Perhaps once the property tax differential and other demand side factors are properly considered we will see Houston’s supply-side impact on housing prices diminish to zero…

Evidence of supply-side effects on home prices remains elusive.

The above quote is a short extract only. You can read Cameron’s full article here.

So let’s take a look at the data to see if Cameron’s claim that Texas’ stable and seemingly affordable housing has been caused by its “high property tax rate”.

Below is an interactive graphic showing median property taxes by state as a percentage of home prices and income. The graphic was last updated in July 2011 (Click here to use interactive graphic).

- Median property taxes as a percentage of home value;

- Median property taxes as a percentage of income; and

- Median property taxes paid per home.

{kind=link}

{kind=link}

")

{kind=link}

{kind=link}

")

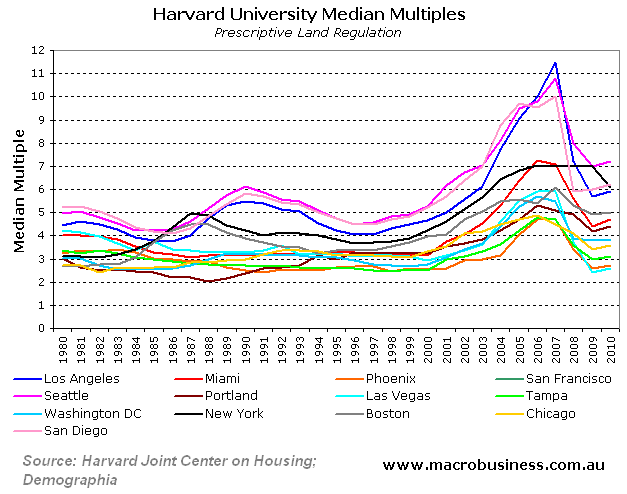

Okay, so Texas is the stand-out amongst the supply-responsive states.

Now let’s combine the supply-restricted and supply-responsive states together to determine whether there is a strong correlation between the level of property taxes and home price stability and affordability. Texas is shown in red, the supply-restricted states in blue, and the supply-responsive states in green.

First, consider median property taxes as a percentage of home values:

Now median property taxes as a percentage of incomes:

And median property taxes paid per home:

As you can see, Texas clearly does not have the highest property taxes – that honour goes to New Jersey. Moreover, Georgia, North Carolina and South Carolina – all supply-responsive states with relatively stable and low cost housing – have relatively low levels of property taxation.

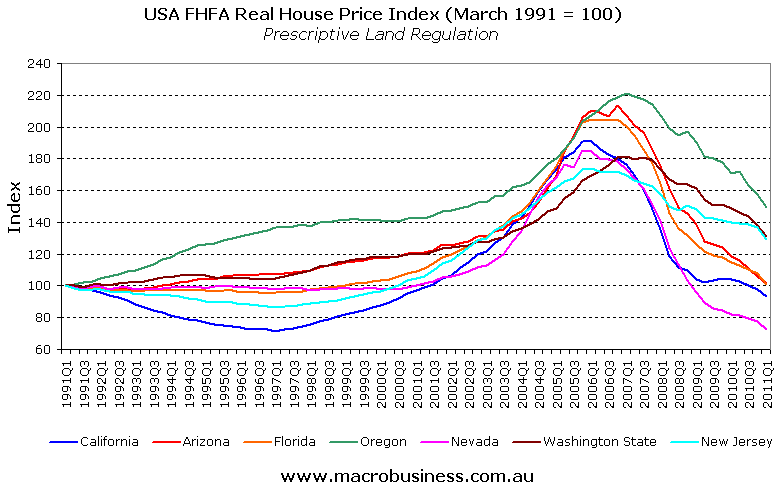

To put these findings into perspective, and to debunk Cameron’s claim that the level of property tax is a key determinant of whether home prices remain stable and low, I have charted New Jersey’s home prices and Median Multiple against the supply-responsive states.

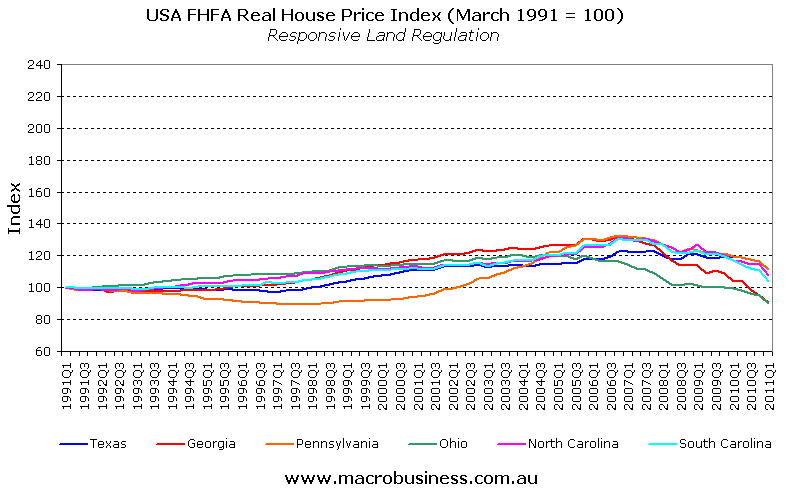

First, real house prices:

As you can see, New Jersey’s home prices have been far more volatile despite it having the highest property taxes.

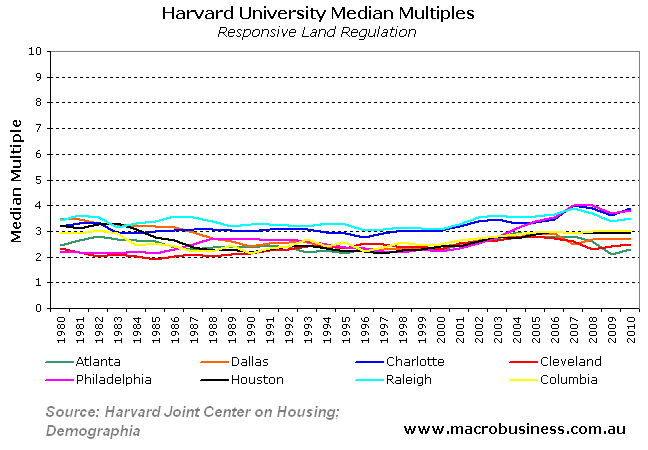

Second, consider the Harvard/Demographia Median Multiples (note: the New Jersey / New York metropolitan area is joined):

Once again, despite having high property taxes, New York / New Jersey metro has experienced lower levels of affordability and much higher volatility than the supply-responsive states.

While there are very strong reasons supporting the implementation of a broad-based land or property tax in place of less efficient forms of taxation, it is difficult to argue that such taxes have played a major role in promoting price stability and maintaining low property values in the US.

If property taxes were a major factor, New Jersey’s home prices would be low (relative to incomes) and it would have experienced minimal price volatility. In a similar vein, Georgia, North Carolina and South Carolina – all low taxing states – would have experienced relatively higher home prices (when measured against incomes) and high levels of price volatility.

Perhaps Cameron’s last sentence should instead have read: “Evidence of supply-side effects on home prices remains elusive conclusive”.