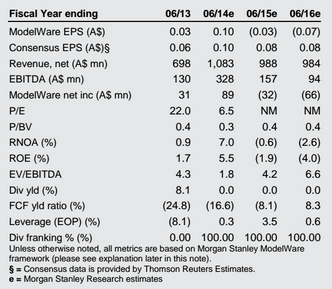

Morgan Stanley on Atlas’ production beat yesterday:

Atlas reported 4Q’FY14 production which beat company guidance and MSe. However, the beat was led by the early delivery of the 12Mtpa expansion and should only be viewed as a timing effect. The product splits between the Standard and Value Fines products were in line with MSe, which leaves our view on the equity unchanged. We maintain our Underweight view, primarily driven by our below consensus iron ore view, which in turn makes a Horizon.

That still doesn’t explain why the equity fell 5% on a volume beat, timing or not. What was the market hoping for, the unearthing of a unicorn?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.