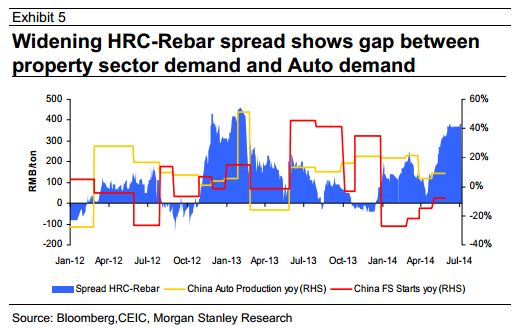

Morgan Stanley has some nice charts today summarising where we are in the Chinese steel cycle. The changing composition of Chinese growth, that many miners see as a positive, is obvious in steel prices with consumption related steel up and construction related steel down:

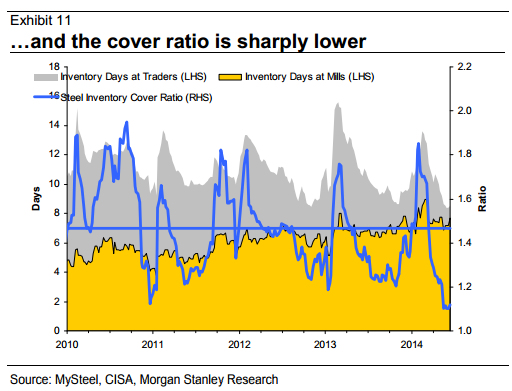

Because construction related steel is a much larger consumer of tonnages (its decline will therefore be bad for miners) the overall slack in the market is combining with tight credit to push down steel trader inventories:

This potentially sets us up for a decent Q4 iron ore restock as the new year may again trigger a steel trader and mill inventory rebuild. I think it likely to be lower levels than this year given it will coincide with renewed weakening in the Chinese economy. But it will likely still require extra iron ore even if inventories are currently comfortable:

The most likely outcome remains a weakening iron ore price for the next few months and then firm rebound into year end.