Crude oil is only up $5 or so since the Iraq crisis escalated (though some movement prior is probably related) but the charts look very bullish. The daily chart is flying in free air:

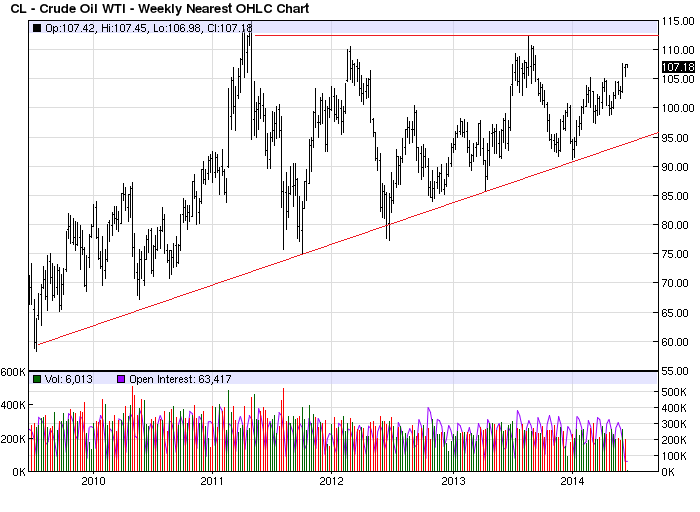

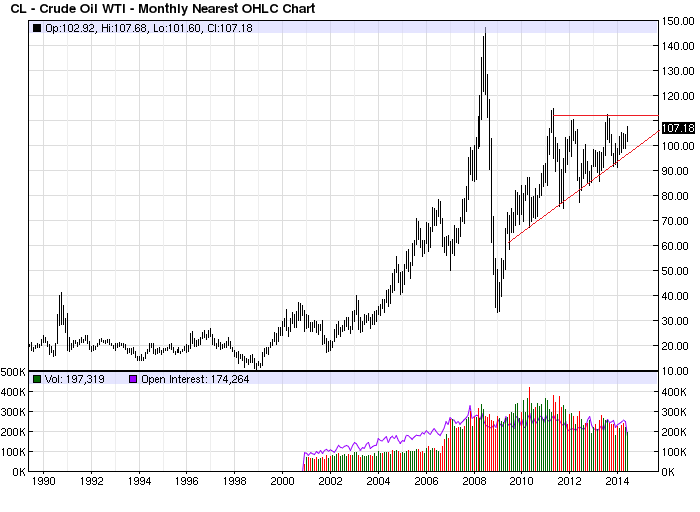

And the weekly and monthly charts both look ball-tearingly bullish on ascending triangle patterns:

Advertisement

It leads one to ask when will this become a problem? For the US economy, Morgan Stanley has an answer:

Whether price increases are temporary or sustained matters most when modeling the contemporaneous effects on the economy of a rise in oil prices. Simulations of a permanent, upward shift in the price of Brent crude of $10/barrel indicate that real GDP growth four quarters out would be reduced by roughly 0.4 percentage points (pp) and that CPI would be higher by about 0.9pp – compared with our baseline. Growth in real consumer spending would be reduced by 0.5pp.

If, however, we model a transitory $10/bbl rise in Brent crude prices (occurring in the current quarter and dropping back to previous levels in the subsequent quarter), the impact results in no net change in the growth rate of real GDP, nearly no net impact on CPI, and no net change in the growth rate of real consumer spending – one year out.

A stress test of our model indicates that a more extreme, sustained $50/barrel jump in oil prices would be enough to stall the US recovery, precipitating a single quarter of sub-1% growth and lowering real GDP growth by 1.7 percentage points one year out. A price surge of that severity would also raise CPI growth by about 3.6pp and lower real consumer spending growth by a full two percentage points.

Thankfully, the military scenario still seems most likely to result in a stalemate before Baghdad is attacked so a $50 spike remains a tail risk. But the proxy war scenario is playing out and that’s going to mean a chronic condition of higher prices as conflict drags on, meaning higher prices for longer and spikes on the news flow.

Advertisement

For Australia this has largely played out so far in support for the Australian dollar because of the line of reasoning that we’ll benefit from higher oil-linked LNG prices. There is some truth in that and it will hold so long as the price rises are not extreme, in which case I would expect a big “risk off” move in markets to more than compensate. A sustained moderate move up in the oil price, that slowed but not staled US growth, would likely end in more bond bullishness, also increasing the attractiveness of carry trades into higher interest rate markets.

In the longer term, however, higher oil prices are only going to increase the shift away from Australian LNG contract prices once oversupply begins in 2018. The comparable US gas flow that begins in 2018 is not oil-linked. The process is very likely, therefore, to accelerate the shift away from Australian volumes, towards other producers, an to ensure the steepest possible mining capex cliff.

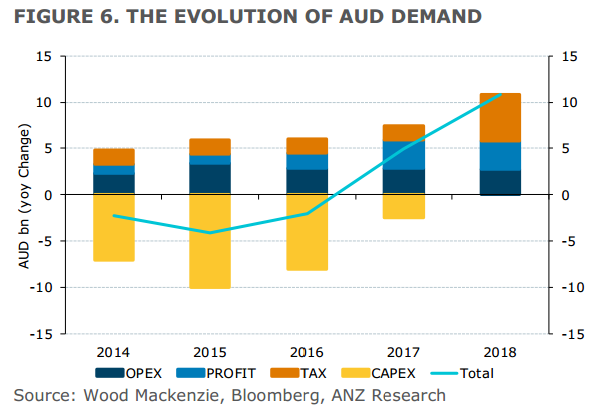

As well, ANZ makes the point today that LNG production is not going to effect the AUD materially until then either:

Advertisement

Phase III of the mining boom (the production phase) will not result in significant new net demand for the Australian dollar (AUD) until at least 2018.

New sources of demand will manifest as onshore operating costs rise alongside profits. However, ownership structures, cost dynamics, and the fact that the mining companies operate in USD makes this a far more nuanced story.

Overall, the impact from the rise in trade volumes will not be large enough to determine the broader direction of the AUD. The key domestic determinant will remain the terms of trade.

So, the answer to the question posed by this post is, yes, if oil remains high but not extreme, the biggest point of impact for Australia will be that the expected terms of trade falls associated with the coming gas glut will be slowed and so too dollar falls.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.