by Chris Becker

Let’s look at what is shaking up in macro markets around the world.

Starting in Asia yesterday morning, Japanese GDP surprised on the upside, particularly capital/business spending. This didn’t send Yen moving as much as hoped, with mainly algo trading last night correlated to moves in the S&P500 keeping the exuberance to a low level: (Chart from Zero Hedge)

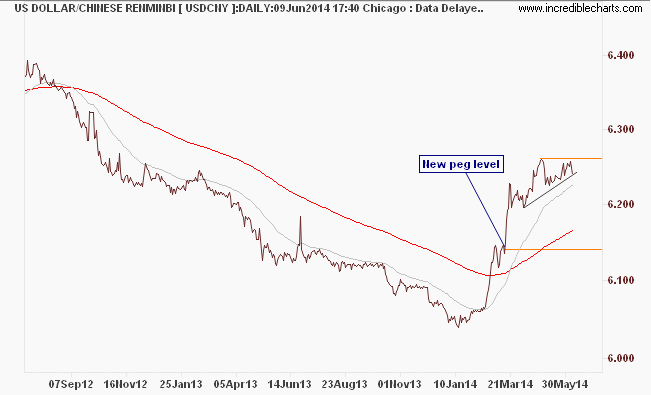

In other currency news, the Chinese government raised its dollar-yuan (Renminbi) peg yesterday, strengthening what many see as the world’s next reserve currency:

China’s central bank set its dollar-yuan central parity at 6.1485 per USD, down from the 6.1623 parity level Friday and much lower than Friday’s 6.2502 market close

Here’s the daily chart going back showing the breakout early in the year that it looks like the Chinese authorities want to contain:

In stocks, not much to mention apart from exuberance everywhere! All major markets up including historic closes for the German DAX and US S&P500 (plus the small cap Russell 2000) this should put a rocket under the lazy SPI futures and ASX200 this morning.

An interesting call coming from Deutsche Bank, which seems to be like shouting in the wind at the moment. From ZH:

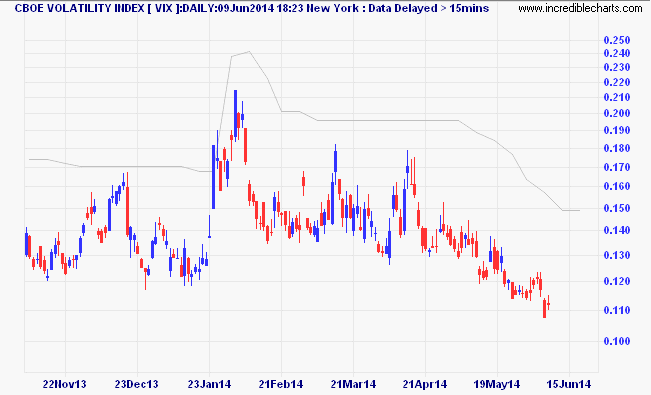

With a closing P/E ratio over 17 and a VIX under 11, Deutsche Bank’s David Bianco is sticking with his cautious call for the summer. Their preferred measure of equity market emotions is the price-to-earnings ratio divided by the VIX. As of Friday’s close, this sentiment measure has never been higher and is in extreme “Mania” phase. Deutsche’s advice to all the summertime-‘chasers’ – “wait for a better entry.”

Here is the CBOE Volatility Index or VIX, which had some big moves intraday, up nearly 4% from Friday (I’ll discuss that little grey line in a separate post on trading volatility):

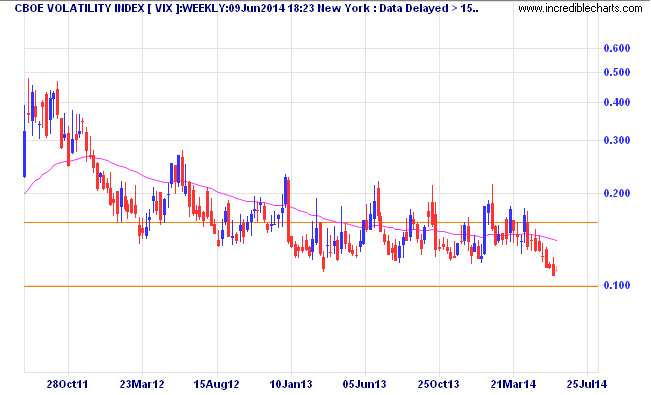

But lets put this into perspective using weekly charts and why some are worried about this “calm” – the VIX is testing its early 2007 lows (guess what the spikes are?)

Is this the calm before the storm? Astute watchers of markets (and macro economics) know that sustained periods of low volatility BEGET short, sharp and painful periods of high volalility. Calls before the GFC that “the business cycle has been tamed” or nonsensical arguments that the 2003-2007 Aussie stock market bubble was a “new paradigm” (i.e. double digit year-on-year gains with low volatility) are being repeated ad nauseam across market circles and media.

Of course, they are right so far – don’t fight the trend, but for heaven’s sake, have a risk management plan in place.

More later today, especially on commodities where I’ll have a closer look at crude oil (ICE and WTI), amongst others – check out my Trading Week post from yesterday giving a broader overview.