By Chris Becker

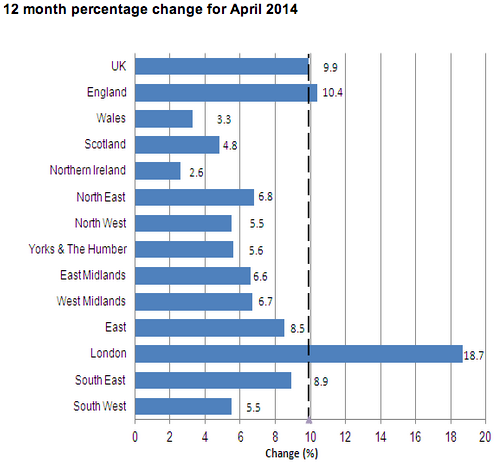

It seems you can’t go wrong speculating on property, as capital gains in London – 19% for the year or £71,000 – are almost double the average post-tax income for Londoners!

A shocking chart from FT Alphaville tells the tale:

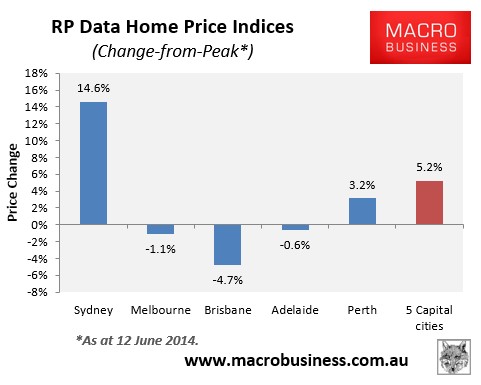

It’s even better in Sydney where house prices are up nearly 15% this year on a median around 680k:

That’s$100k per annum, much better than your average salary. Take the year off and let your dogbox earn the cash for you? What a plan!

Advertisement