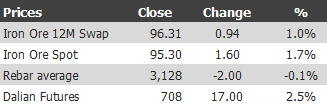

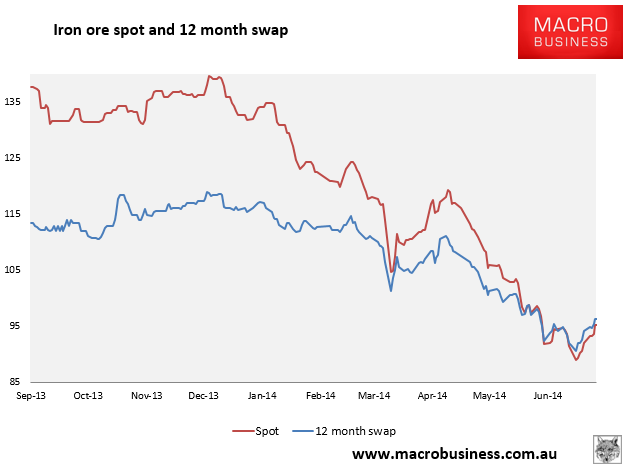

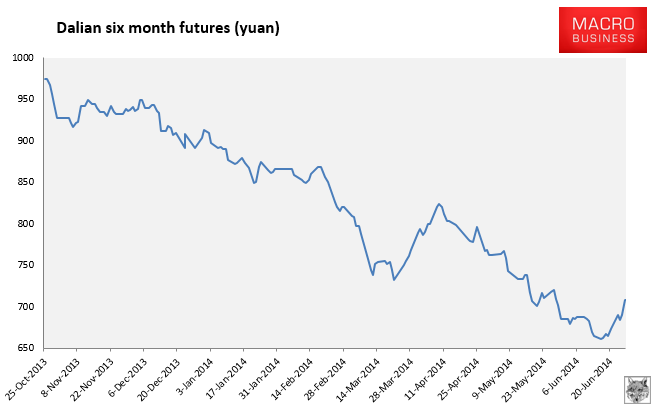

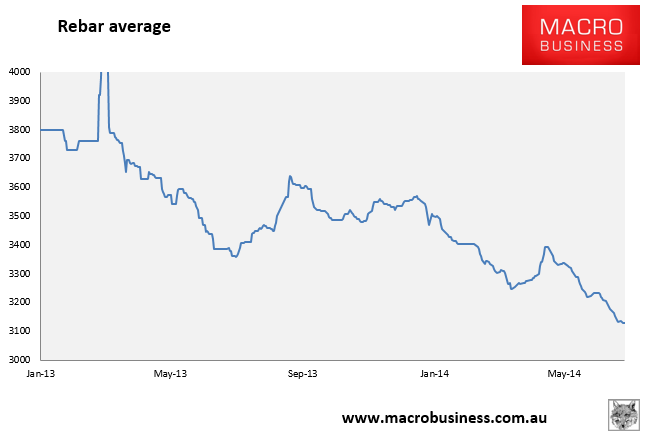

Here are the iron ore price charts for July 26, 2014:

So! The paper market short squeeze tightens. The Dalian 6 month was especially impressive, limit up at one point, and rebar futures were up 1% too. However, physical remains mixed. Spot is up firmly, although nothing like the 5-7% daily jumps we saw in the 2012 recovery, but rebar average is still falling indicating weak underlying demand and the Baltic Dry capesize lost another 3% and has pretty much retraced its entire recent gain. Reuters offers texture:

“Some local governments have started to implement some small stimulus measures to boost activity and I think the better economic outlook is behind the surge in prices,” said a trader in Shanghai.

…Some traders were buying spot iron ore cargoes at higher prices, optimistic that a stronger recovery in the market is taking hold, traders said.

…”There’s a view that the market has reached a bottom, and some traders are buying up cargoes,” said an iron ore trader in Tianjin who was hoping to sell a shipment of low-grade iron ore from Honduras as prices recover.

For now it looks like India’s needs have been satisfied:

Tata SteelBSE -0.95 % has no more plans to import iron ore to feed its steelmaking factories, and will rely on domestic production from its own captive mines or National Mineral Development Corporation ( NMDCBSE 0.00 %), its managing director TV Narendran told ET. Tata Steel imported about 0.5 million tonne of iron ore from Australia to tide over the temporary closure of its mines in Odisha in May. All of Tata Steel mines have reopened thereafter, providing necessary supply of the commodity.

…Other steelmakers in the country are looking at the option of importing iron ore seriously if production from mines in Odisha comes down. Even though mines allotted to Tata Steel and SAILBSE -1.27 % have been cleared by the state government , other mines under the illegal deemed extension clause are waiting for approvals.

Brazil’s Vale, the world’s biggest iron ore miner, is starting to offer discounts on shipments of the steelmaking raw material to top consumer China, joining Australian rivals in cutting prices following a global surge in production.

The move follows deeper price cuts by Rio Tinto and Australia’s Fortescue Metals Group for lower-grade iron ore, and indicates China is winning more say over pricing after years of complaining that costs were too high.

Vale is offering some Chinese customers a discount of $2.50 a tonne, including cost and freight, for 62-63 percent grade standard sinter feed Guaiba (SSFG) for third-quarter contracts, three mill sources with direct knowledge of the matter said.

“We’ve been told by Vale that we would get a price cut of $2.50 a tonne for SSFG for third-quarter contracts. The market is now changing quickly to a buyer’s market and competition among miners is intensifying,” said an iron ore buying official with a state-owned steel mill.

…An official with another large state-owned steel mill, which also sells iron ore to other mills, said the company was still in talks with the Brazilian miner but some of its customers had been offered the same discount.

It’s interesting to note that Vale is discounting above benchmark ore, suggesting endemic market weakness.

The NDRC also released data on the January to May period of steel production. Output was 342 million tonnes (mt), 2.7% year on year. That’s 5.3% lower growth than the same period last year. Iron ore and coke outputs were up 10.9% and down 1.6% year on year respectively. Exports of steel are flying at 34mt, up 34%year on year. But profitability at mills still fell 16.4% year on year.

In other words, if you subtract the growth in exports, Chinese steel production has fallen year on year by somewhere around 1%.

So, does this add up to a renewed restocking push and what’s the price target? No and who knows!

This still looks to me like a paper short squeeze getting some traders excited about offloading their loss-making cargoes at better prices. The rhetoric around better Chinese growth is fair enough but until property at least slows its descent then the changing composition of investment is going to weigh on demand and mills do not need to raise inventories. Indeed, they still face the seasonal slowdown ahead in Q3. On the other hand, we’ll likely see more stimulus announcements.

My best guess is that the move will flame out around $100 but so far I’ve over-estimated every bounce in this great slide.