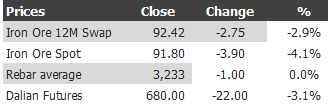

Here are the iron ore price charts for May 30, 2014:

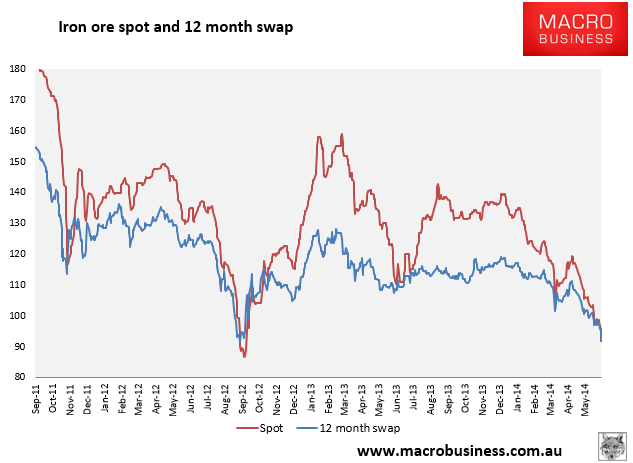

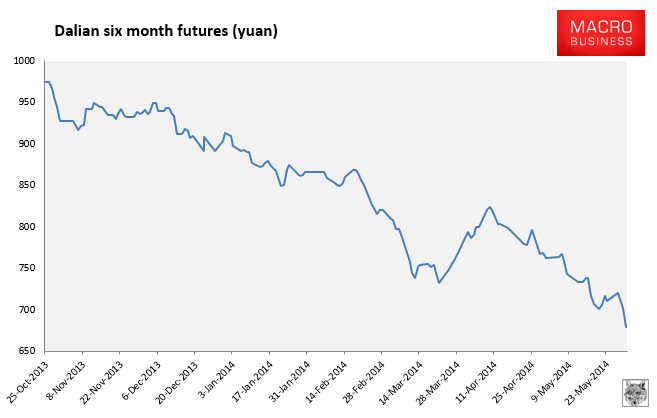

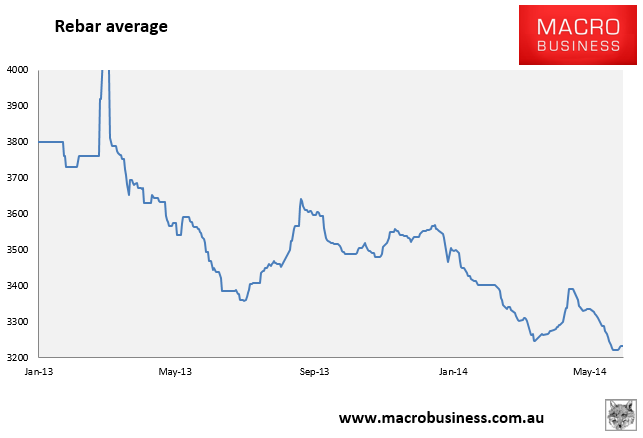

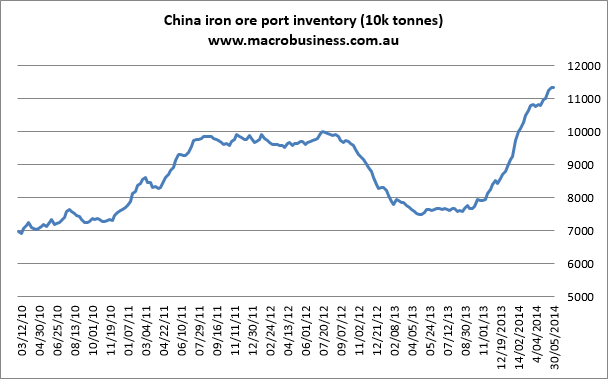

Don’t adjust your television set. Iron spot fell 4.1% even as port stocks added another 300k to 113.6 million tonnes. Dalian six month futures were smacked 3% to a record low. Rebar average stalled. Rebar futures fell to a record low. The Baltic Dry capesize component managed a 1% climb but is still languishing.

It is clear from the iron ore price gapping that appeared on Friday that panic seized traders. I see two possible scenarios. The first is that Friday’s dump was caused by the rumoured end of May deadline for traders to meet new, tightened prudential requirements on their loans. If this is the case then the selling should ease this week. In support of this case, the market has moved into a long-dated contango which has marked bottoms in the past, although it is still shallow at this stage.

Alternatively, a self-fulfilling cycle of falling collateral, margin squeezes, dumped stock, rinse and repeat has taken hold, al’a 2012.

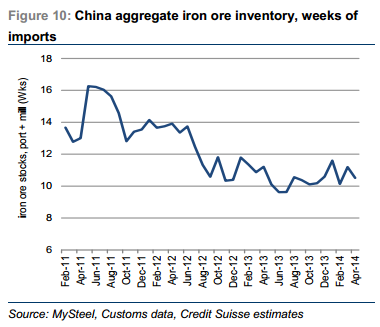

In such circumstances, we all know that the iron ore price can crash. It does so until aggregate port and mill iron ore inventories are sufficiently cleaned out. A Credit Suisse chart combining mill and port stocks last week showed that although inventories are lowish they can go lower:

Note that during each major price correction of the past few years total inventories (by days of supply) have dropped then stabilised in a lower band. Over time, mills and traders are adjusting to a new normal of no more stimulus and abundant supply. This is a structural shift and we could be on the verge of the next step down in the process.

All of this is only circumstantial evidence for further price weakness but that’s where we are. My Q3 destock thesis appears to be transpiring right now. Remember that my target forecast for that move was in the mid $70s range. Macquarie thinks so:

Macquarie Bank analysts noted Friday further iron ore stockpile reductions in China expected based on a disconnect with the current availability of iron ore.

Prices may fall to $80/dmt as destocking takes hold next month and then recover quickly, or stay in a $90-100/dmt range over the third quarter and recovering further in Q4, based on its scenarios, the bank said in a report.

“We believe the next step of iron ore’s transition process will be a clearing out of excess inventory — a process that will mean purchasing activity needs to drop below real demand and is likely to result in near-term downside risk to prices,” Macquarie warned.

Macquarie’s description is right on the money. But, given we’re so early in the year, unless we see a sudden rush of stimulus, third quarter steel demand is going to be seasonally weak exacerbated by the property slowdown. There’ll be no impulse to restock aggressively so a more muted rebound than 2012 is likely. A Q4 restock is still probable in preparation for the 2015 Q1 steel rebuild and Pilbara cyclone season. Also possible is a reversal of the quarters for these two outcomes with an earlier restock but disappointing Q4. A rebound to $110 or lower seems a fair outcome and then sinking back to $80 and lower in Q1 next year.

Of course, aggressive stimulus would drive a bigger rebound, which is where we find Andrew Forrest:

“The Chinese ability to manage poverty out of its country is unprecedented and their consumption of steel is still running at record rates,” Mr Forrest said.

He said betting against China’s growth story was the “only guarantee of a loss I have seen in a long time’’.

“I’m pretty comfortable with the iron ore price oscillating around the $US110 (a tonne) mark,” Mr Forrest told the conference.

“It could wander down to $US80, it could wander up to $US140.”

He said it was a case of “thank god we have China’’.

“You have a situation where they’re trying to urbanise an Australia every year,’’ he said.

I’ll never say never but the chances of iron ore rocketing back to $140 are remote. It doesn’t matter if China urbanises an Australia every year if that is not more than the year before. Once urbanisation is past halfway, and it already is, then it will detract from growth (but can be supported by wider demolition and rebuild rates). Even a high plateau in steel demand will not help the higher cost miners. They have invested on the assumption of a parabolic demand curve that in reality does not exist.