Two prominent bank economists have issued warnings today that consumer spending will remain subdued and is poorly positioned to drive the economy as the mining investment boom fades.

From Bank of America-Merill Lynch chief economist, Saul Eslake:

”It is difficult to envisage a scenario in which consumer spending growth would recover strongly to an above average growth rate,” Mr Eslake said.

”The federal budget has taken away from household incomes and sapped sentiment and this has exacerbated an already challenging environment.”

Mr Eslake said he expected consumer spending to slow to be ”significantly below average” this year with ”only a modest improvement in 2015…

”In an environment of elevated household leverage, a preference for debt management and savings will … persist with consumers remaining prudent.”

And from Warren Hogan, chief economist at ANZ Bank:

Over the last 25 years, consumer confidence has only been lower than these levels during the financial crisis and the 1991 recession, Mr Hogan told the Committee for the Economic Development of Australia’s State of the Nation conference.

“My feeling reading this is just how sensitive the consumer is to bad news and this is a major issue for our economy”…

“[The consumer] won’t do what it did after the Asia crisis in the late 1990s and leverage up, build and buy houses and buy lots of products and cause economic activity to lift,” he said.

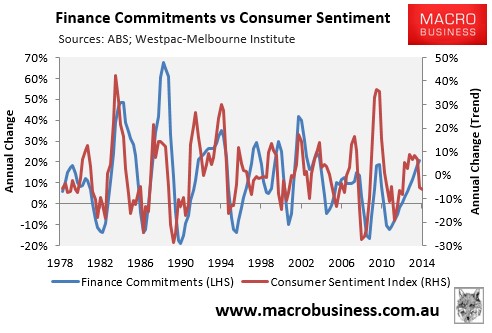

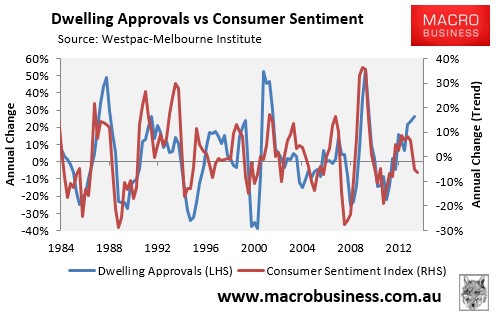

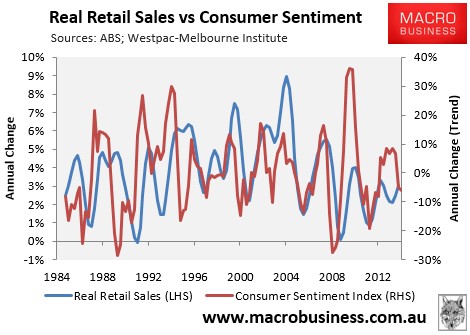

As illustrated a few weeks back, the recent slump in consumer sentiment is a bad omen for the economy, with consumer sentiment displaying a sharp correlation with house prices:

Housing finance commitments:

Dwelling approvals:

And retail sales:

Clearly, as long as consumer sentiment remains subdued, consumption spending is likely to remain well below trend, stifling rebalancing towards the non-mining economy.

Then the are the longer-term structural headwinds that will weigh on the consumer and broader economy.

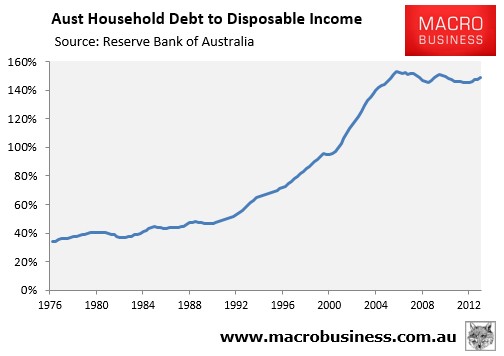

First, there is Australia’s near record high level of household debt, which limits household’s ability to leverage up like they did in the 1990s and early-to-mid 2000s (see next chart).

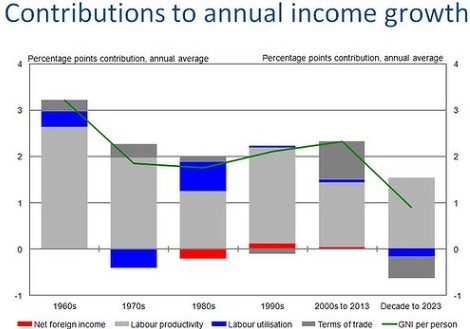

Second, there is Australia’s falling per capita income growth: a trend that is likely to continue as the terms-of-trade trends lower and workforce participation declines (see next chart).

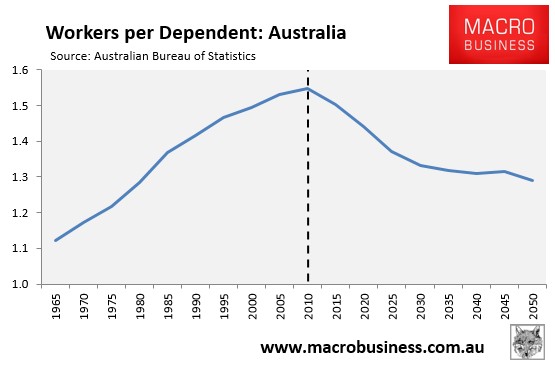

Finally, and related to the above, there is Australia’s ageing population and declining worker share, which will weigh on both income and consumption spending across the economy (see next chart).

While a cyclical pick-up in consumer spending is possible if sentiment recovers, chances are that it would only be modest and short-lived, given the structural headwinds facing the consumer. Hence, the “new normal” is for much lower consumption growth than was the norm over the past 20 years.