by Chris Becker

Following the discussion yesterday on “Are Shares Crazy?” here’s an excellent example of what I was trying to say, via Cullen Roche at Pragmatic Capitalism:

Before we begin, we are all “active” investors to some degree. No one, not a single one of us, can implement a truly passive index strategy in the same way that is so often cited by many studies against “active investment management”. We buy and sell periodically, we rebalance, we change allocations, etc. So, let’s all get on the same page and agree that we are all active investors to SOME degree.

We confuse real investing with allocation of savings. We are told on a daily basis that we are “investors” on secondary markets who can strike it rich if we just buy the right stocks and bonds.

But the reality is that when you buy stocks or bonds on a secondary market you are allocating your savings into what was really someone else’s “investment” and it’s very likely that the easy money has already been made and these real “investors” are cashing out.

Real investors build future production, make great products, provide superior services and only sell their majority interest in that production at a much later date (often on a stock exchange via an IPO – CB: this is a primary market).

The idea of getting rich in the stock market puts the cart before the horse. You shouldn’t look to “get rich” in the stock market. You should look to get rich making investments in yourself and on primary markets where real investment is done. (See here for more).

As I was saying – the stock market is a secondary market, where non-primary assets are exchanged on the speculation of price appreciation. I’ve long contended that the definition of “Assets” need to be divided into 3 classes before even considering asset allocation questions (e.g. stocks/bonds/cash percentage composition)

“Security assets” that have some or all of the following attributes:

- Non-yielding (or non-reliance on any yield)

- Non-speculative

- Un-leveraged (The exception is a low LVR mortgage on your primary place of residence)

- Secure property right (physical or legal)

- Intangible insurance (e.g health or life)

- Have zero or very little volatility in pricing

Typical examples include your home, a few weeks or months supply of liquid cash, an equivalent or greater amount in physical gold, if possible, agricultural land with secure water supply and definitely some form of life/disability and other types of insurance (I would even go so far as including education here before allocating surplus funds to other types of assets).

“Investment assets” must have all of the following attributes:

- High or complete certainty of original capital return

- Known and calculated payoff in yield/earnings

- Zero or very low leverage preferably max. 25% LVR (i.e must be positively geared)

- Provide at minimum same return as government bond

- Zero or known risk that can be adequately insured or hedged

The critical makeup of these assets is that they have known payoffs and a known certainty about the return of your original capital – that is, they have zero risk or completely insurable risks. They are definable risk assets that provide the investor with psychological security, knowing they will get two types of returns: a continuing annual yield and a return of the original capital at maturity/exercise/sale.

Examples would include annuities, most government and corporate bonds, term deposits, certain property investments (whilst avoiding concentration and high leverage) and a very small population of listed stocks. Stocks are the exception, not the rule.

Assets that do not have all of these factors are speculative in nature and do not belong in this category.

“Speculative assets and activities” have any of the following attributes:

- Uncertainty of return of capital

- Unknown but possibly very high payoff

- Unmeasurable risk (none, low or high)

- A known/estimated but uninsurable risk

- Any leverage exceeding 50% LVR (i.e more than half is borrowed)

- Depends upon underlying price volatility for positive returns (i.e is negatively geared or has negligible yield)

- Uninsurable/cannot be completely hedged

There is no moral judgement of what is what in these categories, rather its how you manage the risk thereof. My point is to suggest that your allocation into shares as an “investment” with no worries or concerns about an unknown payoff or return, drawdowns or the underlying need for a secular bull market (in almost all cases) is a falsehood that will lull you into complacency about your actual speculation and how you ultimately make a return on your savings.

Cullen also gives a one-two punch to the notion of why the so-called “equity risk premium” doesn’t really exist (i.e. the excess return over “risk-free” bonds that shares give each year, in exchange for higher risk (actually volatility, which is different):

We don’t account for real, real returns properly. In other words, we tend to hear about the nominal return of the stock market or something like that and fail to account for taxes, fees, inflation and other frictions. And in doing so we fail to account for how much a high fee or other frictions can really diminish our returns. (See here for more).

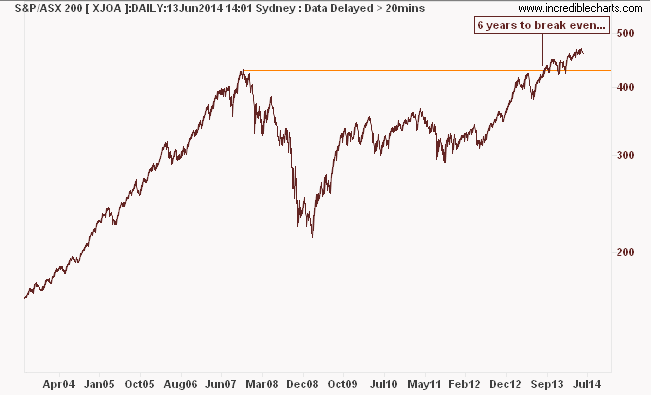

According to APRA who have made these calculations, in superannuation – where active and passively managed funds proliferate – your average five year rate of return is 3.1% p.a. and extends out to 5.7% for 10 years, but this relies almost entirely upon one of the biggest bubbles in Australian stock market history, from 2004-2007 (this is the ASX200 Accumulation chart, which includes dividends):