Of all of the financial systems in the world, Australia’s is most similar to the UK. Of all of the restrictive housing planning systems in the world, Australia’s is most similar to the UK. Of all of the house price boom and bust cycles in the world, Australia’s is most similar to the UK. The Bank of England also practices inflation targeting (though its cap is 2%). The UK and Australia share a similar economic model reliant upon external borrowing to fund consumption and low export-to-GDP ratios but the main difference is that the UK economy is a more diverse mix of value-adding sectors with a much higher contribution from manufacturing.

But today there is one very new difference. The UK has announced it will henceforth practice macroprudential regulation to control its housing cycles and prevent them from hollowing out the economy.

From Coopercity:

When Julius Caesar took his army over the River Rubicon in Northern Italy, he changed the rules of ancient Rome forever. This morning we have seen a Rubicon moment for British banks and building societies.

The announcement that the Bank of England is to limit loan to income values for mortgages is a significant point in this country’s financial history. As Mark Carney stated, such restrictions occur elsewhere but not in the UK. It is a sign of the damage that the housing boom and bust did to the country’s financial system and economy that this step has been taken. It highlights the increasing regulatory control of the financial sector. And despite the crisis beginning almost seven years ago, the increase in regulation is still ongoing and not expected to ease anytime soon.

In Jan 2011 Bob Diamond, previous CEO of Barclays famously said to the Treasury Select Committee “There was a period of remorse and apology for banks – that period needs to be over.” Well he completely missed the mood of the country, its politicians and regulators. The regulatory pendulum is now swinging firmly in the opposite direction of the loose wild days that made Diamond (and also broke him).

At the moment, the new restrictions seen relatively painless for the banks. But the point is that the Bank of England now has this power. Restrictions can always be increased, once created.

Although I am against interventions in the free market as a general principle, I still think this is a good idea. Time after time all around the world, not just the UK, property boom and busts have occurred with alarming regularity. They do serious damage to the financial system and therefore the economy. We cannot rely on the banking industry to learn from the past and not over lend in the boom times. It has proved itself incapable of such responsible behaviour. Restrictions on mortgage lending are an alternative to using interest rates that also impact the rest of the economy. It is a sound plan.

At the moment the plan is to limit 15% of all new mortgage lending (per bank) to 4.5 times income. Carney admits this will have little impact currently, but may do so in a year’s time. He also wants banks to check affordability of mortgages by assuming a 3% point increase to the lending rate. The plan is in a consultation phase at the moment and the new rules to be implemented by October 1st.

“The recovery in the UK housing market has been associated with a marked rise in the share of mortgages extended at high loan to income multiples”:

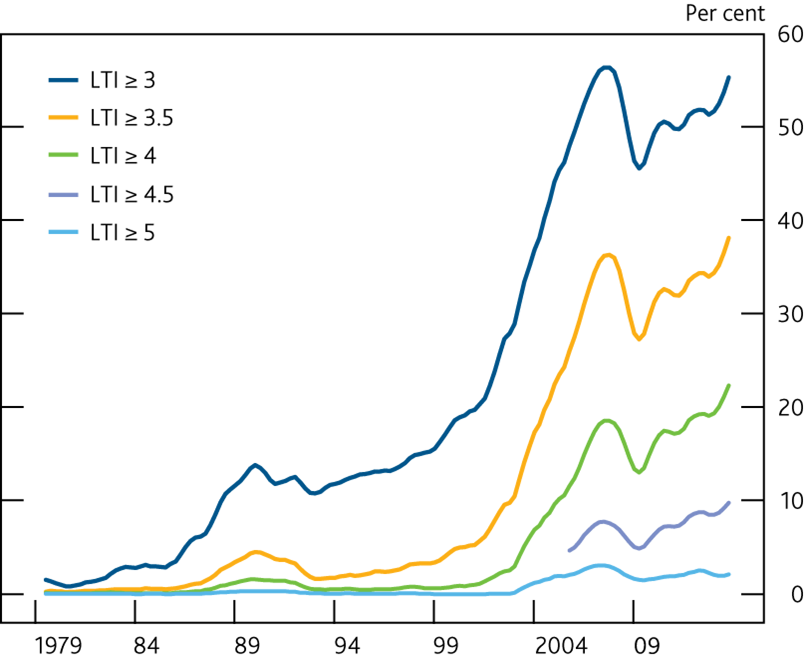

The Share of new mortgages with LTI multiples above 4.5 has risen to a new peak:

This is a relatively scary chart, particularly the LTI >4 line in green. LTI of 3-3.5 is regarded as affordable but getting to 4 times and over, much less so. This chart shows that currently over 20% of new mortgages have a LTI ratio of over 4, up from close to zero pre the crisis. The >4.5 LTI line in purple shows why the new limit at 15% has no impact currently – only 10% of new mortgages are being written with a LTI of over 4.5 times. However the Council for Mortgage Lenders has noted that the “London market will be the main place that notices the 15% limit on 4.5x income. 19% of London loans were 4.5x or more in Q1”.

But you have to remember that the past five years has seen almost zero wage growth whilst property prices in some areas continued to head higher. That makes LTI ratios strained until wages pick up (which is expected to occur as unemployment falls and skills shortages emerge). The good news for financial stability is that loan to value ratios have only risen a little as larger deposits have been required by weak banks.

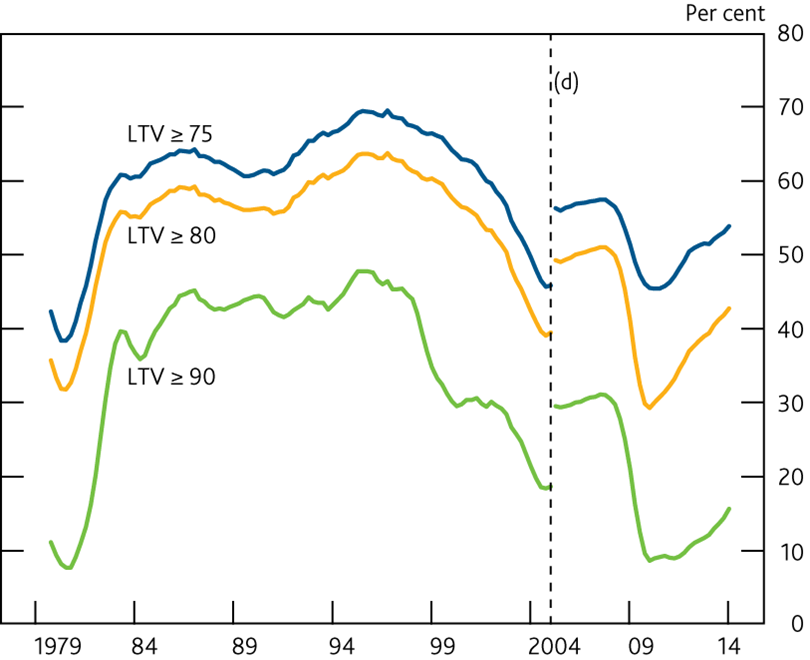

New Mortgage Lending at high LTV ratios has risen modestly:

Carney’s argument against over indebted Britons is that they can cause economic instability. By being more indebted, they cut spending far more when times are difficult. Hence making economic weakness worse. Hence his argument as to why these enw rules are good for macroeconomic stability.

There is criticism that Bank of England’s low interest rates and QE created the recent house price boom to start with. But that is slightly unfair. The real boom has been in London and that is partly a result of the safety and attractiveness for foreign buyers in uncertain times. To engineer a UK recovery, it was a good idea to help consumers to spend and feel more confident which is best done through a stronger housing market. The consumer recovery has given businesses the confidence to spend too and now the recovery is broadening out. It is now sensible for the BofE to gain these new powers and send a warning shot over the bows of the banks that restrictions may get tighter if needs be. Lets face it the banks have barely recovered from the last crisis, it is way too soon to be embarking on a new one!

So there you have it. The Poms now have the system to control house prices without raising interest rates that we need far more than they do. After all, the pound has been weak anyway on QE. It will curtail the London property price blowoff without ruining the wider economy and protect the UK economy from the accelerating cycle of currency wars.

Meanwhile, we will be protecting our financial system and productive economy with Luci Ellis’ ridiculous stick figures.