How long is the memory of a nation? Six years it seems. From the AFR:

…the nation’s lenders have raised more than two-thirds of a combined $51 billion of funding in the offshore markets so far in 2014, according to Thomson Reuters. At the same point in 2013, the banks had raised just $35 billion, of which just over half was sourced internationally.

The faster pace of foreign borrowings comes as bank borrowing costs have declined to levels not seen since May 2008, before the onset of the crisis.

The boost in offshore funding could mark an early sign that the banks’ four-year long $400 billion deposit war is over, tipping the balance of pricing power in the local economy further away from savers and towards borrowers. With increasingly cheaper funding available in the international capital markets, banks are offering less generous interest rates to savers as the urgency of chasing deposits subsides. Borrowers, meanwhile, are expected to reap the benefits of cheaper wholesale funding costs as competition to write new loans forces banks to pass on savings. Australia’s banks borrow money from the wholesale capital markets to fill a “funding gap”, the difference between the new loans and deposits that finance the loans.

The funding gap is estimated to be $600 billion. In a speech on Friday, Westpac deputy chief executive Phil Coffey cited research from PwC which estimated the gap could grow to $1.325 trillion if there was a pick-up in credit growth.

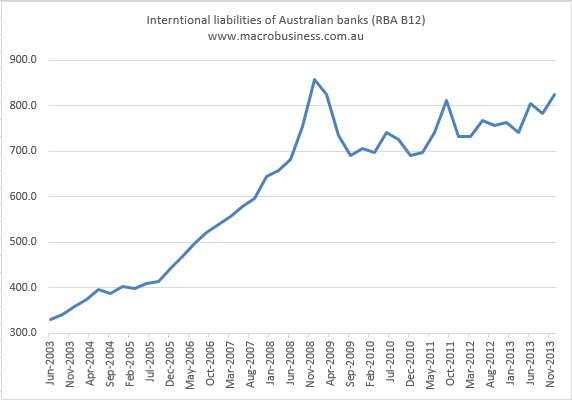

Here is the latest chart from the RBA showing the rising borrowing, it’s quarterly and likely lagging:

Notice how the article is focused entirely upon the “funding gap” as a tactical challenge in which the banks are innocent players. In reality there is no “funding gap”. Rather, our financial system is addicted to unproductive mortgage-lending and that crowds out the kind of business lending that would generate income growth and local savings. The “funding gap” is created by the banks not serviced by them.

For a long time I have expected slowly rising credit growth to manifest in a tightening of local deposit markets. Instead, the global chase for yield – a complete rerun of the pre-GFC period – is bringing in yield spreads and enabling the banks to ramp up external borrowing. This is another black mark for APRA, which has done a good job until now of preventing this kind of breakout.

One line of defence remains in the credit rating agencies, which have also warned the banks that any increased external funding risk will damage their rating outlooks. I would expect those warnings to turn more serious within a year.

Where it ends is predictable:

Mr Coffey said it was uncertain how the funding gap will be closed and warned about the risks of increased offshore borrowings. “Some predict that the shortfall in deposits would be offset by higher wholesale borrowing by banks – but prudent bank management will be wary of creating undue financial risks, through higher wholesale borrowings,” he said. “Just because investors are prepared to buy Australian bank bonds today, does not guarantee they will do so in the future.”

When the next global shock comes, it is the tax-payer that will wade into global markets with a renewed explicit guarantee to the bank’s liabilities to prevent disaster. You’re not paid for carrying this risk, even though the current widespread budget pain is a direct consequence of it.

Gosh, you are generous.