By Chris Becker

The self-managed super sector continues to outperform the so-called “pros”, according to NAB with average yearly returns (after fees) hovering near 7% compared to 4%

From SMSF Advisor Online:

A NAB analysis has demonstrated SMSFs outperformed APRA-regulated funds between 2005 and 2012.

A Rice Warner analysis of APRA and ATO statistics commissioned by NAB indicates that during the period from 2005 to 2012 SMSFs generated an average annual return of 7.7 per cent compared to the average 4.9 per cent return produced by the rest of the superannuation industry.

Taking fees into account SMSFs produced a return of 6.8 per cent over the eight years compared to 4.1 per cent for the rest of the superannuation industry.

NAB’s executive general manager banking and wealth solutions David Gell said the analysis shows that not only have a million Australians chosen to manage their own retirement savings, “they’re actually doing a particularly good job of it”.

“It is clear that SMSFs do rate very well in terms of performance against the other funds, contrary to some perceptions out there,” .

Who are those million Australians? Mainly Baby Boomers with average fund balances of $1 million and over 60% in retirement phase according to APRA.

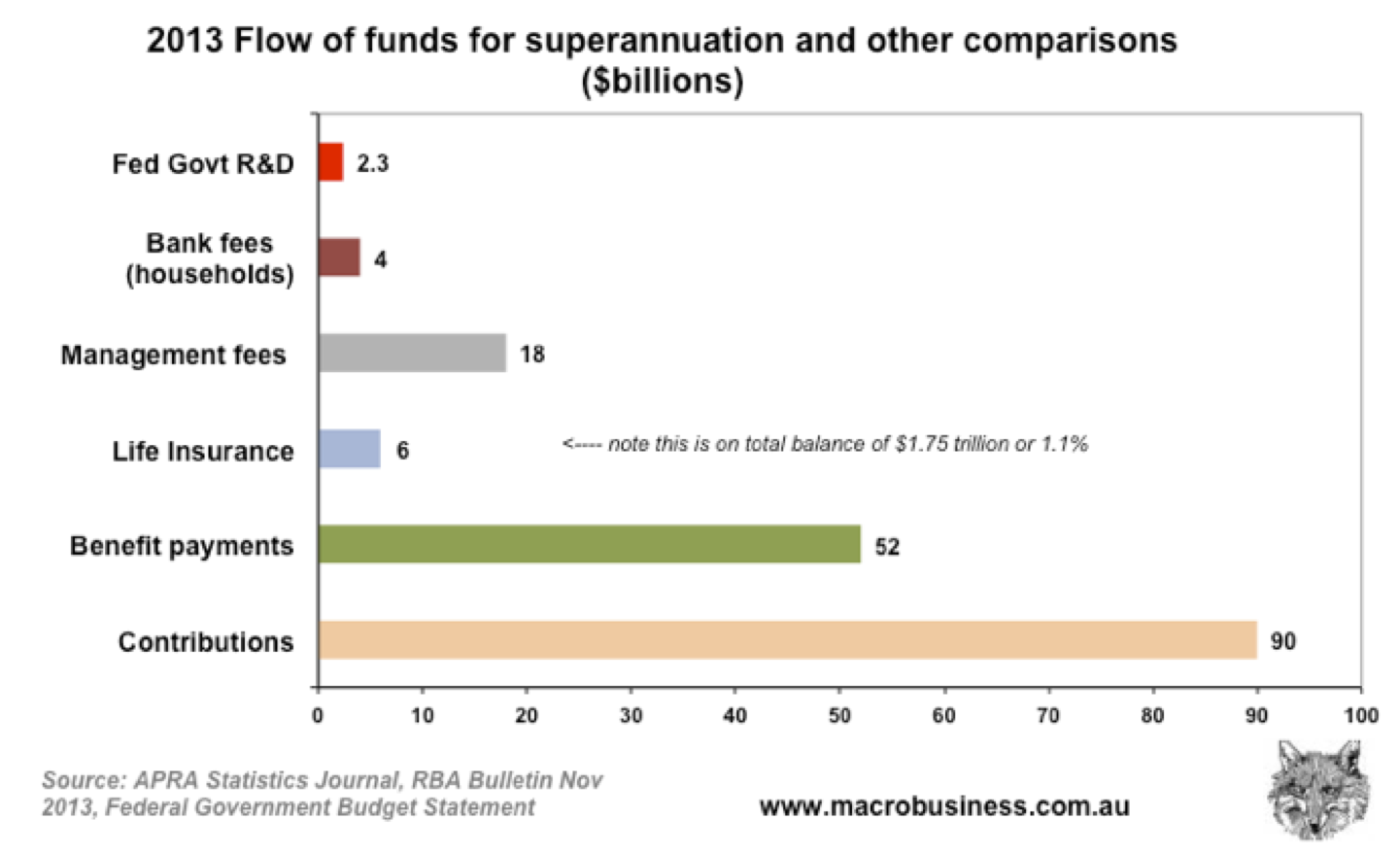

On the other hand, the average Gen X/Y is stuck in a “default” fund, with considerably smaller balances (between $42,000 and $70,000), and happen to be the main contributors to the ticket-clipping “pros” earning some $18 billion a year, who also rely upon a nice chunky stream of 9% (or more) of your income:

This is a story MB has talked about this previously where the evidence is quite clear: you are paying a huge premium in having your super managed for you, particularly if you’re in a retail fund (although industry funds are not that much better – only the fee difference, in aggregate, helping out here).

This result, which hasn’t changed since SMSF were created, also implies you are further paying a huge premium if you are not actively on top of your super balance.

Go do something about it – get self-managed and get involved. This out-performance, and the crowding out of the DIY crowd will ensure the super industry will lobby hard for heavier restrictions on anyone contemplating looking after their own money.