The boys at Business Spectator are bearing-up something chronic on housing this morning. Callam Pickering sees the peak:

…dwelling price growth appears to have hit a hurdle, with nominal prices down 0.5 per cent in May to date. Prices in Melbourne are now 2.5 per cent off their March peak. Perth prices haven’t grown since November. Prices in Sydney have stumbled.

…A boom built on speculation is susceptible to changes in lending activity. By comparison, price rises that are driven by income growth or higher construction costs are likely to be more persistent or sustainable.

…Investor lending rose by 0.4 per cent in March but the pace of growth has slowed rapidly in recent months. The graph below, showing monthly trend growth, shows a distinct loss of momentum following a period of exceptionally strong growth.

…There is little reason to expect first home buyer activity to increase significantly in upcoming months. Even if it did, it would be insufficient to fill the gap left by investors and owner-occupiers.

… A slowdown in China would hit Australian property from all angles and has significant implications for both investment and prices.

Meanwhile Rob Burgess makes a more subtle point about rental yields:

What [the Budget] adds up to is billions of dollars in reduced spending power for tenants renting at the cheaper end of the property market.

While some would like to think ‘bludgers’ will just cut back on cigarettes, alcohol, illicit drugs or the like, the lobbyists in Canberra gave a very clear picture of tenants who will double up in rooms, sleep on each others’ couches, move back in with parents or as one said “become destitute”.

Of course none of that will happen if the Abbott government’s ‘learn or earn’ plans work — if, for instance, the government’s $50 billion infrastructure stimulus package, which leveraged with state money will fund $125 billion of projects, gives them all jobs.

…Many just won’t have as much to spend on rent. Property investors in the less glamorous suburbs of metropolitan or regional centres may feel the sting of welfare cuts as much as their tenants.

A hit to household formation in other words.

At the end of the day, what these pieces are both pointing to is trouble with income. That’s what the Budget was really all about, whether or not you agree with the particular re-distributions, it was forced to be harsh owing to the falling rate of growth in national income.

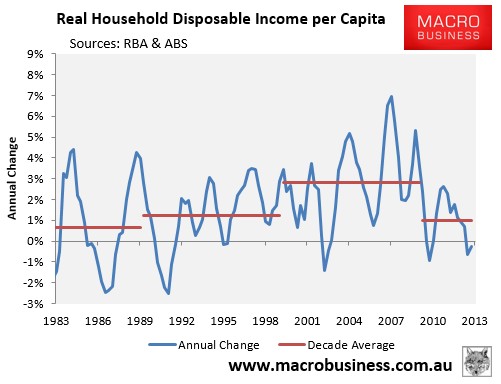

Australia has enjoyed a glorious period of income growth through the mining boom that supported the housing bubble that inflated before it:

Household income was boosted by the boom in three ways: share prices and dividends, real wage growth and, most importantly of all, massive tax cuts.

Now that that boom is draining away with the falling terms of trade, the tax cuts are reversing, real wages are declining and stock market gains have stalled.

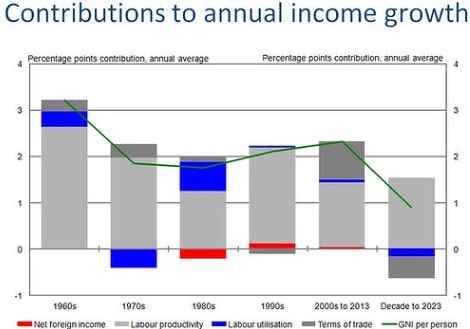

And there is no end in sight. As Treasury rightly forecasts, we’re in for a long period of bugger all income growth and none at all if we can’t get productivity up:

Nobody knows when housing will roll over. We think a steady erosion of growth rates this year into more rate cuts next is the best bet. But one thing we can say for certain is that the fundamentals that temporarily back-filled the millennial housing bubble are fast disappearing and, as we’ve been repeating in our special reports, “the unfolding structural adjustment makes gearing-up into property a risky proposition despite some favourable cyclical signals. The risk of correction sometime in the near future is arguably greater now than at any other time in living memory.”