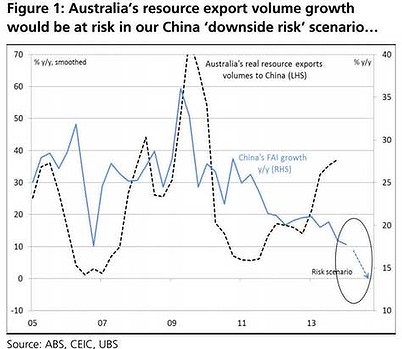

The SMH blog is carrying an excerpt from a UBS study of the impact of a hard landing in China upon Australia:

Australia would suffer a loss of income – While the AUD’s willingness to swing around 20-30 cents in prior cycles has been key to Australia’s 22 years of uninterrupted growth, at the current juncture, Australia’s yield carry & relative AAA fiscal strength would likely see the AUD fall less than is needed to fully offset an expected fall in commodity demand and prices from a sharp slowdown in China.For key sectors of the economy – It’s likely the investment outlook would weaken further.

While non-mining capex may lift on a lower AUD, an even sharper drop in mining is likely to dominate. For the consumer, the unfolding pick-up through 2014 could reverse course in 2015 as confidence weakened on the back of negative offshore news flow and negative wealth effects as risk markets (particularly Aussie equities) would likely be weaker. Sub-trend growth would also limit any further fall in unemployment. For housing, the current upcycle may be more elongated, but it remains a relatively small sector, unable to offset the combined weaker capex, exports & consumer sectors.

Overall, growth in China closer to 5% in 2015 would likely see us lower Australia’s forecast for 2015 growth from 3.25% (after 3% in 2014) back closer to 2%. Below trend growth would lift unemployment and lower inflation. Reflecting this, we’d likely remove our modest rate hikes (+75bp) from 2015, and look for the AUD to move lower toward USD0.80 or below (rather than USD0.85 currently for end 2014). Such a China scenario certainly increases Australia’s recession risk, but this would still likely be avoided, subject to a move lower in the AUD.

With respect, that doesn’t pass the laugh test. In the case of a Chinese downturn driven especially by big falls in construction, Australia would face an intense external shock. Here is what would actually happen:

the income shock would be very large as iron ore fell to $50 and coking coal fell to $80;

FMG would go out of business and be bought by the Chinese. RIO would face a potential debt restructuring;

the blow to equity prices would be substantial as the S&P500 also fell heavily;

Australian consumer confidence would collapse under the shock and house prices immediately begin to fall;

the capex cliff would accelerate downwards on non-housing, manufacturing and mining investment. Housing investment would last a little longer on its existing pipeline but developers would begin to go belly up quickly as sales evaporated;

unemployment would jump 1-2% in a matter of months

the RBA would cut interest rates to 1.75% but rising debt funding costs mean the major banks only passed on 50pbs

house prices would not respond until the dollar fell through 70 cents and the fiscal stimulus kicked in, a package of roughly $30 billion over eighteen months, and probably including a new first home buyers grant

Net exports would rise as several gas projects came on stream and the dollar fell heavily.

Advertisement

We would be fortunate to avoid a recession in the popular definition of two negative quarters of growth (depending upon how aggressive the fiscal stimulus is) but on any other more useful definition, such as GDP per capita or unemployment, we would almost certainly succumb.

There’s probably no need to go further but I will. Within a year we’d have ourselves a nice little stimulus-led rebound but the real problems would just be beginning. After a brief rebound China would be settling into a permanent lower growth profile from 4-5%. Australia’s terms of trade would resume falling on increasing LNG supply. The national budget would now have a gross debt to GDP ratio closer to that of Canada and be stripped of its AAA rating as it became obvious that surpluses were a thing of the distant past. Fiscal tightening and persistently high national funding costs would renew deflationary pressure on housing and unemployment would begin to creep higher once more.

We would exist in a state of zombie economics for a number years as households finally embarked on deleveraging proper, supported by substantial gas exports. Slowly and painfully, Australian competitiveness would improve and tradables investment rise again.

Advertisement

That’s assuming, of course, that we avoid an outright current account crisis, which seems a fair supposition if Chinese growth doesn’t fall further.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.