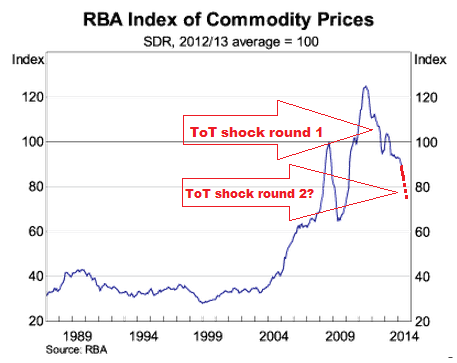

The RBA index of commodity prices for April was out last night. It is a good proxy for movements in the terms of trade and shows we’ve entered a second leg correction that has some way to run:

Preliminary estimates for April indicate that the index declined by 1.3 per cent (on a monthly average basis) in SDR terms, after declining by 2.3 per cent in March (revised). The largest contributors to the fall in April were declines in the prices of iron ore, coking coal and gold. The base metals and rural commodities subindices rose in the month. In Australian dollar terms, the index declined by 3.9 per cent in April.

Over the past year, the index has declined by around 12½ per cent in SDR terms. The prices of many commodities in the index have fallen over this period. The index has risen by 0.3 per cent in Australian dollar terms over the past year, reflecting the depreciation of the Australian dollar over this period.

As indicated in previous releases, preliminary estimates for iron ore, coking coal and thermal coal export prices are being used for the most recent months, based on market information. Using spot prices for these commodities, the index rose by 1.4 per cent in April in SDR terms, to be around 15 per cent lower over the past year.

The index compensates for spot and contract prices so you can expect it to keep falling in the months ahead as the bulk contract prices catch up with spot falls. I’ve marked in red roughly where the index is headed on price movements that have already happened and added dots for where it’s going when iron ore hits $80 average.

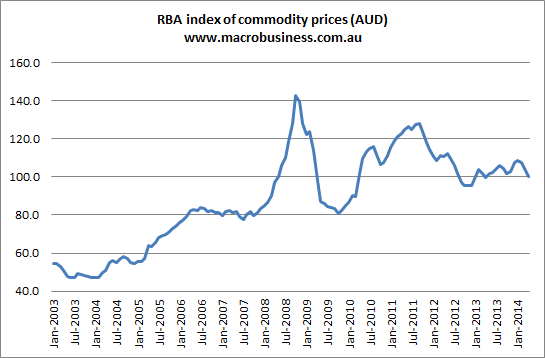

In Australian dollars the index had a very tough month but remains above its 2012 low:

Advertisement

With any luck, and a bit of leadership, it will stay that way. That would help support mining company profits and tax receipts but remember that real national income is still determined more by the top chart than it is the bottom.

I expect the index will drop through 8o by this time next year (perhaps a bit later) which will constitute a second round terms of trade shock. Remember that the first, which began in late 2011, smashed nominal growth, added 1% to unemployment, blew up the Budget, initiated a miner equity bear market, and triggered 2.25% in rate cuts even though the mining investment boom was powering.

Advertisement

The dollar should respond more quickly this time giving us some protection but what will the effects of a second income shock be as the capex cliff falls away and the government cuts spending, I wonder?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.