Capital Economics has more today on the brewing global steel trade war:

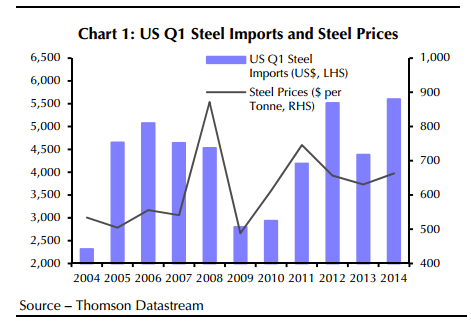

A sharp increase in US steel imports from Asia in the first quarter serves to highlight the overcapacity and overproduction of Asia’s steel industries. Surplus Asian output is undermining the global steel price. Without output cuts, particularly in China, steel prices will continue to fall.

…the above suggest that steel prices will fall further. This would particularly be the case if the US were to impose any sort of restrictions on Asian steel imports, perhaps based on anti-dumping legislation. Indeed, it may be that falling prices will be the eventual catalyst to force consolidation and rationalisation of the Chinese steel sector. We continue to expect US steel prices to fall to $600 per tonne by end-2014, from $660 currently. This compares with a consensus forecast of $660 at end-year.

The US steel lobby is strong and they have a decent case given that excess Chinese steel production is the result of subsidies and public ownership. The deteriorating strategic environment around Ukraine and Vietnam probably doesn’t aid a presumption of generous policy-making, either.

China exporting the problems arising from its dying steel ponzi scheme is not a lasting solution.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.