Another day, another spurious defence of negative gearing has arisen, this time by RP Data’s Cameron Kusher (via its weekly Property Pulse):

“Negative gearing continues to be a contentious issue and feature of the tax system which is unique to Australia.

“Another point worth noting is that the data in the 2011 Census shows that the Government only owns and rents out around 4.1 per cent of total housing stock; conversely dwelling approvals data shows that a very small proportion of new housing approvals are granted to the public sector.

“Looking at these two individual results, it would suggest that the Government has little interest in building or managing rental accommodation. This suggests that negative gearing is in place to encourage developers to build new rental accommodation and private individuals to act as landlord for those who aren’t in a position to own their own home.

“While it would make sense to apply negative gearing only to newly constructed properties, politically it would likely be unpopular. Furthermore, if negative gearing was to be removed the Government would likely have to play more of a role in constructing new homes and managing a portfolio of properties. On balance, they probably see that foregoing almost $8 billion in taxation revenue is more cost effective than developing and managing a greater proportion of new housing stock,” Mr Kusher said.

Needless to say, I find Kusher’s logic odd.

Advertisement

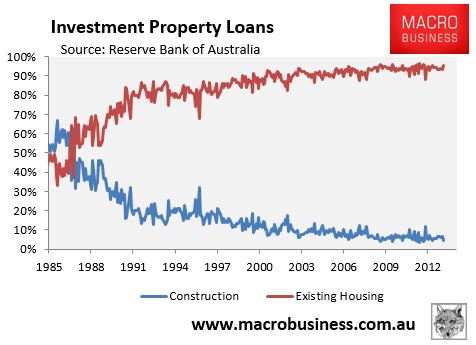

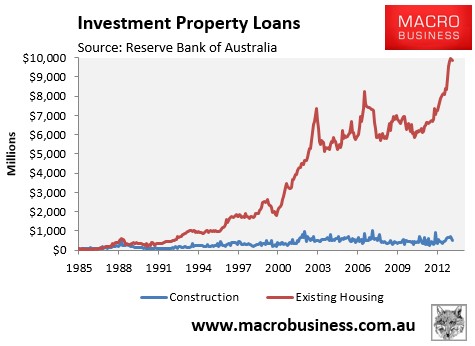

As noted repeatedly, the overwhelming majority of investors purchase existing housing (see below charts).

Hence, negative gearing, in its current form, is not “adding” materially to actual housing supply or doing anything to increase rental availability. Further, investors “built” a much higher proportion of rental dwellings when negative gearing was quarantined between 1985 and 1987 than they do now.

Advertisement

Further, as noted by Saul Eslake in his 50 Years of Housing Policy Failure speech last year, there is absolutely no evidence to support the claim that negative gearing results in more rental housing being available than would otherwise be the case:

Most other ‘advanced’ economies don’t have ‘negative gearing’: yet most other countries have higher rental vacancy rates than Australia does.

In the United States, which hasn’t allow ‘negative gearing’ since the mid-1980s, the rental vacancy rate has in the last 50 years only once been below 5% (and that was in the March quarter of 1979); in the ten years prior to the onset of the most recent recession, it has averaged 9.1% (see Chart 8 above).

Yet here in Australia, which does allow ‘negative gearing’, the rental vacancy rate has never (at least in the last 30 years) been above 5%, and in the period since ‘negative gearing’ became more attractive (as a result of the halving of the capital gains tax rate) has fallen from over 3% to less than 2%.

During that same period, rents rose at rate 0.8 percentage points per annum faster than the CPI as a whole; whereas over the preceding decade, rents rose at exactly the same rate as the CPI.

Similarly, countries which have never had ‘negative gearing’ – such as Germany, France, the Netherlands, the Nordic countries and (low-tax) Switzerland – have much larger private rental markets than Australia.

I have one question for Cameron Kusher, or anyone else supporting the retention of negative gearing on rental supply grounds: in the event that negative gearing was wound-back and a proportion of investment properties were sold, who do you think these homes would be sold to?

Advertisement

I have argued repeatedly, supported by the data above, that a large scale sell-off by investors would be met by purchases from renters (i.e. first home buyers). In turn, those renters would be turned into owner-occupiers, reducing the demand for rental properties and leaving the rental supply-demand balance unchanged.

Saul Eslake has argued similarly:

…suppose that a large number of landlords were to respond to the abolition of ‘negative gearing’ by selling their properties. That would push down the prices of investment properties, making them more affordable to would-be home buyers, allowing more of them to become home-owners, and thereby reducing the demand for rental properties in almost exactly the same proportion as the reduction in the supply of them. It’s actually quite difficult to think of anything that would do more to improve affordability conditions for would-be homebuyers than the abolition of ‘negative gearing’.

Finally, the billions of dollars of foregone funds used to subsidise property investors could instead be used to fund any number of worthwhile initiatives, providing far greater benefits to society at large. This could include boosting public housing investment, in turn increasing the overall availability of rental accommodation relative to demand, and improving rental outcomes.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.