Credit Suisse offers a good global PMI roundup today that I agree with:

The April Global manufacturing PMI edged down to 52.0 from 52.1. After three consecutive monthly declines, the index is now at its lowest level since August last year. It nonetheless remains slightly above its long-term average of 51.6, suggesting that the overall pace of industrial activity is relatively satisfactory.

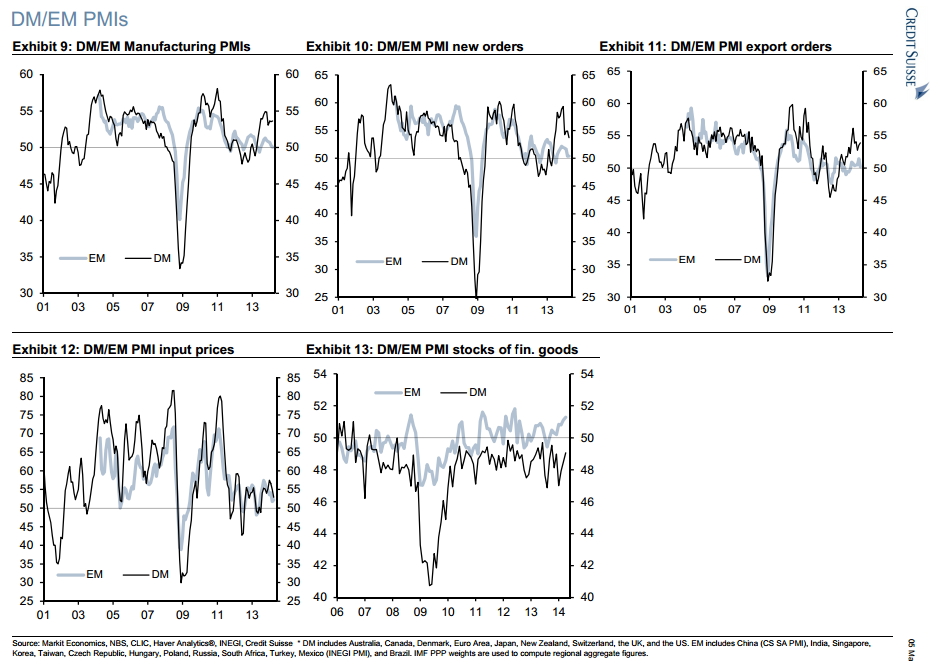

The geographical breakdown reveals a growing divide between Asia and the West. In particular, the Japanese PMI experienced heavy losses as a result of the 3pp VAT hike. Inasmuch as Japan supported the global PMI ahead of the consumption tax hike, it is now dragging it down. At the same time, China’s PMIs are bottoming out – at mediocre levels – but the outlook of the second largest economy in the world is rather sluggish. Meanwhile, the euro area appears to be entering a second phase of the recovery which should see an acceleration in growth rates and job gains. In the US, recent demand indicators have clearly picked up after the setback experienced at the turn of the year.

Overall, we believe the cyclical improvement in the West should outweigh the softness in the East. Therefore, global industrial production momentum should improve in the next couple of months after having been on a downward trend since the end of last year.

In the details, the new orders component fell to 52.2 from 52.9 and thus remains for the second consecutive month below its long-term average of 53.1.

Interestingly, the new export orders component – a good proxy for the pace of global trade – is holding up relatively better. Nevertheless, the stocks of finished goods increased to its highest level since June last year. Consequently, the new orders-to-inventory ratio, a forward looking indicator, has further decelerated.

This suggests that downward pressure on global industrial activity in the very near term remains present.

In the US, ISM Manufacturing increased for a third consecutive month and rose 1.2 points to 54.9 in April, reaching a four-month high. New orders were flat compared to March, holding up at a respectable 55.1 level. Much of the upward momentum in the ISM headline came from the employment Index, up 3.6 points to 54.7, and the inventories index was higher on the month – both lagging indicators. One particular positive factor worth noting is the new export orders index, which was up 1.5 points to 57.0 in April, the highest level since last October. Exports were a big sore spot in Q1 GDP (-7.6%) and net exports were a 0.8 ppt drag. These ISM data tend to be decent leading indicators and suggest the Q1 weakness will not last.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.