Not much data out overnight but that’s no impediment to the US bond rally, which exploded, presumably on Queenslander’s rushing for a safe haven after the NSW win in the State of Origin.

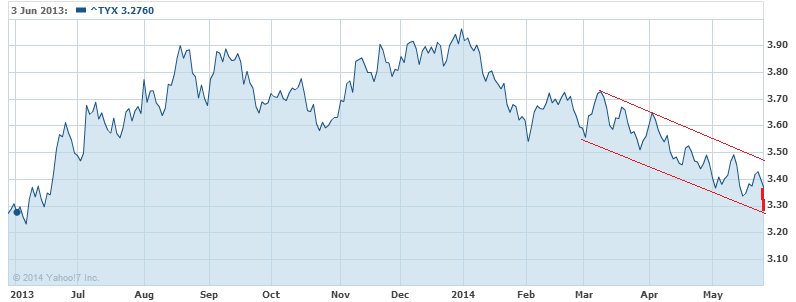

The 30 year powered and yields fell 2.5% to 3.28%:

The 10 year was even more bullish with yields tanking well north of 3% to 2.44%:

It’s taken out crucial technical support and is targeting 2.2%.

The only thing missing is a clear reason for why. Normally, I can make some sense of markets but today I’m guessing.

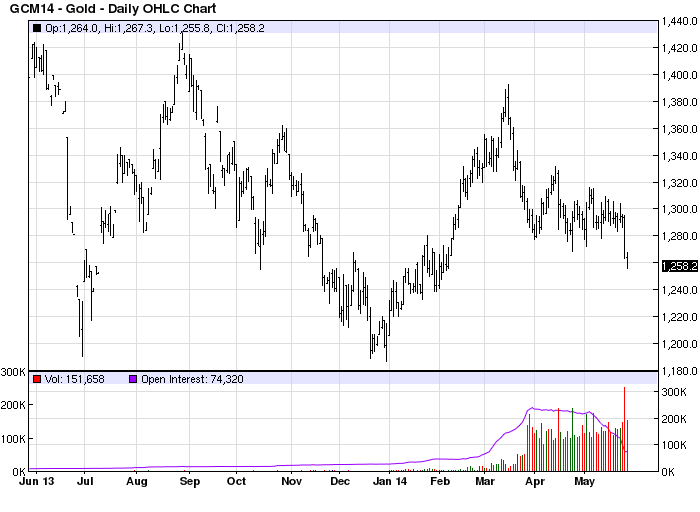

There is no corroboration that the move may be pricing a return to more US QE. On the contrary, gold has broken down and looks like it might test its lows:

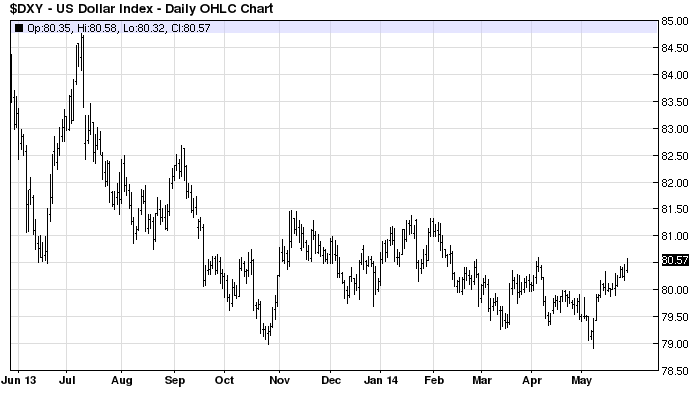

Likewise, the US dollar is firming and looks like it wants to test the upper limit of its 2014 channel:

Some of this is no doubt burgeoning weakness in the euro on the expectation of more QE there.

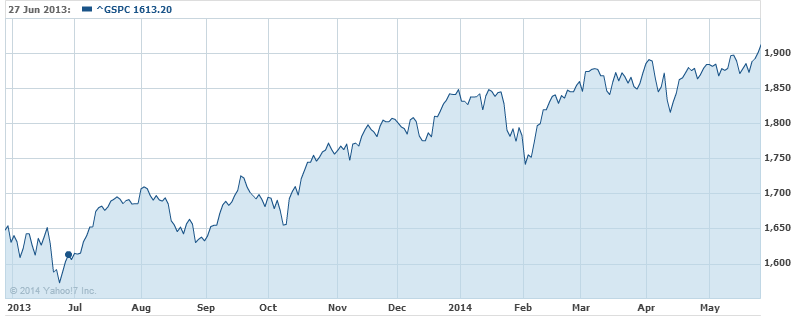

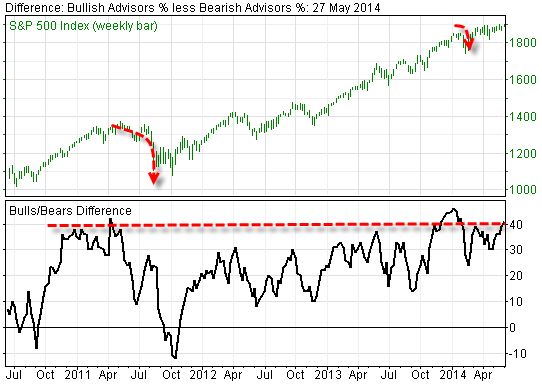

Stocks, too, were firm with the S&P500 hitting a new record on the night above 1900:

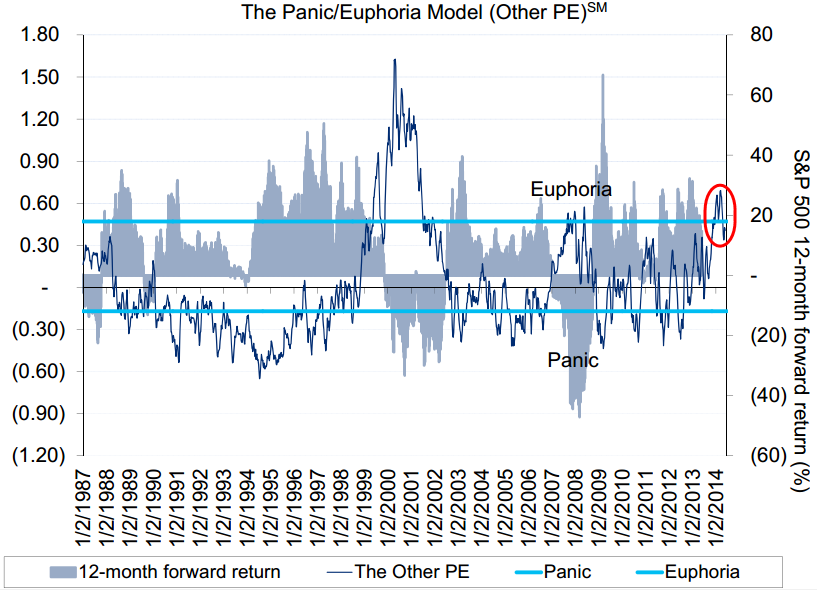

And that’s the nub of the issue. You can’t have this kind of disconnect for long. Zero Hedge points to the last divergence of this nature:

There are three possible outcomes I see for the gap:

- it’s sustainable because Europe isn’t going to launch QE and deflation concerns are driving down bond yields globally. Stocks can ride it out on the Yellen put as the “new neutral” thesis takes hold. Or, the EU does embark on further QE and that drives down global bond yields, supports growth, and stocks;

- it’s going to close as US growth accelerates this year and the labour market generates more inflation than expected and the US bond rally reverses, or

- it’s going to close as stocks correct sharply as the end of QE combines with the ongoing unwind in Chinese housing to spike volatility.

I’m always cautious using ZH material given its penchant for death and destruction but, it must said, version 3 looks the most persuasive to me at this juncture.