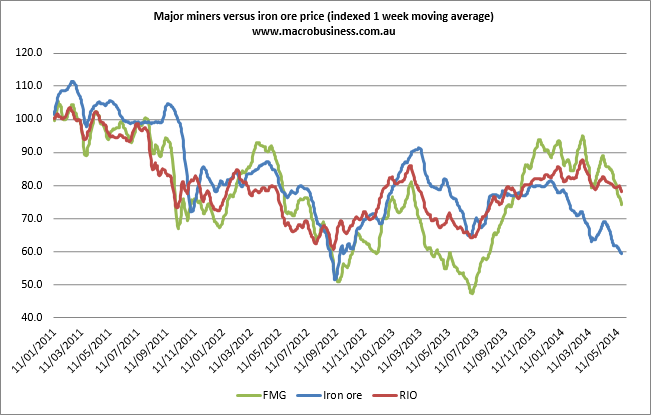

China’s Dalian futures are down another half a percent so far today but miners are catching a break since 11.30 when the dollar was hit. FMG is up 2%. Here’s the latest relative performance chart:

Carrying on the positive theme, there is also this from Fairfax:

A 25 per cent fall in iron ore prices will be felt by the miners, but there are a few reasons why this breach below $US100 per tonne is not as bad as the last venture into double figures in 2012.

…1) Currency: …the cost of doing business is now about 7 per cent cheaper for Australian iron ore miners, whose costs are generally in Australian currency, but whose products are sold into US currency.

2) Expansion: Operating on slim margins is much easier if you are selling more products, and that’s exactly what Australia’s iron ore miners are doing.

3) Cost structure: An unfortunate aspect of the mining industry in recent years has been the number of jobs that have been lost. All the miners, from BHP and Rio down to Gindalbie have cut jobs, while others like Fortescue have aggressively targeted their debt during the past couple of years reprieve.

Crikey. What pills are they feeding them over there? A lot of the miner’s costs are in US dollars but the impact of a lower currency is still firmly positive. Swapping volume for price squashes margins. Costs are down but the price falls will be more enduring.

And that’s the main reason it’s worse this time, not better, because it’s based upon the leading edge of structural oversupply that’s going to get much worse. Last time around it was a cyclical blip.

If the dollar is going to weaken and iron ore to settle near my target of 95 cents (in the short term) then we might see some positive action in iron ore equities for a while.