A comment from one Chad Padowitz of Wingate Asset Management has caught my eye. From the SMH blog:

Offshore investors are likely to question whether it was necessary for Treasurer Joe Hockey to deliver such a harsh budget, given the economy is just picking up and confidence remains fragile, say investment experts.

“Foreign observers may well be scratching their heads as to why a relatively low debt economy needing to transform away from a waning China needs to adopt such tough budget,” says Wingate Asset Management chief investment officer Chad Padowitz.

Padowitz adds that from a global investor viewpoint, the budget measures should please bond holders as it strengthens an already strong balance sheet, while equity market prospects are less positive from a demand perspective.

Low debt economy? Sheesh. Offshore equity market investors are important but beyond resources and bank yield-chasers we don’t really have anything much that they want. Debt matters much more because that’s how we fund most of the current account deficit:

On that front bond investors will indeed be pleased by the Budget. I know I’m the only one in the country that argues the truth of this, bizarrely, but that is what this Budget is all about.

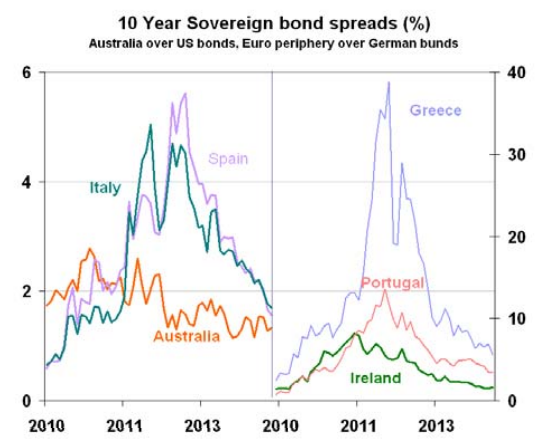

The Australian current account deficit can only be funded at affordable rates if the Budget remains in good shape for its own borrowing rates and, more importantly, for its guarantee of the major bank’s offshore borrowings, which sustain our huge household sector leverage. It is the key stone in the arch of the Australian economy. Take a look at the 10 year bond spreads between Australia and Europe:

The spreads have been coming in as normalcy returns to European bond markets but not here. While some will argue that this is because growth prospects are higher, it’s also because that growth hangs on access to external debt and as a lonesome South Pacific sardine the only insurance for sovereign and bank bond holders is a clean Federal balance sheet. I do not believe quantitative easing and bond monetisation is viable for Australia, lest the currency collapse completely.

If the Budget does not aim for surplus across the cycle then the AAA rating is toast. Here’s S&P in 2012:

“If there’s a sustained delay in returning the balance to surplus, as the economy gathers momentum and as people start spending again, as the import demand picks up and current account blows out, we might not see the government’s fiscal position as being strong enough to offset weaknesses on the external side and that’s what worries us…Australia’s already, as we see it, got some credit metrics that are right off the scale when it comes to assessing Australia’s external position…It’s got high levels of external liabilities, it’s got very weak external liquidity and that basically means the banks are very highly indebted compared to their peers…For us, we look to Spain, which was Australia’s closest peer four or five years ago in terms of having a very strong fiscal position, very similar to what Australia has at the moment, its external position was weaker, like Australia’s, and it got routed very quickly…The government needed to provide support to the banks, it had to shore up growth in the economy and its debt levels more than doubled…We can see that happening in Australia’s case.”

And again today:

Overall, this budget, along with the nature of the current political debate, is consistent with our view of strong political commitment to prudent budget finances. The government flagged its intention to make politically-sensitive spending cuts of this nature well in advance. It strongly signaled its intentions to address spending pressures since before the September 2013 general election, continuing most recently with the release of the Commission of Audit report. Indeed, ongoing willingness to make difficult budgetary choices may well be needed in coming years. We consider there to be potential for further revenue write-downs, given the current importance of Australia’s terms of trade to the government’s revenue base and the inherent difficulty in forecasting its trajectory.

If equity investors are displeased or bemused by a tight Budget then they really don’t understand what they’re invested in.