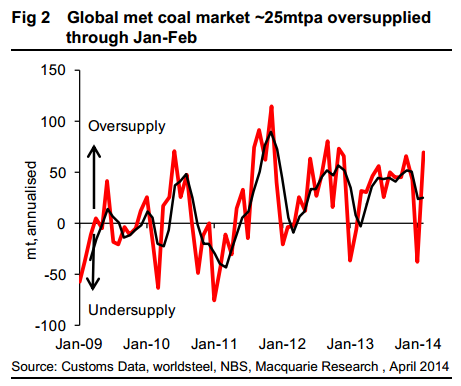

OAO Mechel is the latest miner to cut met coal production in North America, having announced on Tuesday that it is halting its Bluestone operations in West Virginia. In total, we estimate recently announced North American production curtailments amount to around 11mtpa. This is one reason we think spot price risk is starting to skew to the upside, but that further cuts are required to fully rebalance a global seaborne met coal market that was oversupplied by 25mtpa through January and February.

Making assumptions for global exports in March, we think that this oversupply fell to 10-15mtpa last month, but the reality is that this is a market that has not seen a sustained deficit for a couple of years, hence the steady broader deterioration in prices.

One of the common misconceptions when it comes to US coal exports is that a tighter domestic thermal market will result in weaker US thermal coal exports. In fact, marginal met coals are first to be redirected. Quite simply, almost all exported US east coast thermal tonnes are due to decisions made previously (hedging, contracts with EU utilities, take-or-pays), since spot market sales are uneconomic at delivered prices into Europe below $85-90/t (and current spot is ~$76/t). We would expect that further closures and/or re-directions are announced in due course.

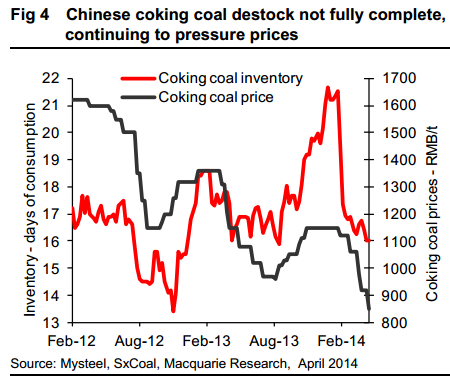

The other factor behind the extreme weakness in met coal has been the relative absence of China from the seaborne demand side, with its seaborne met coal imports down 22%YoY through 1Q14. Chinese steel mills entered a prolonged period of destocking at the end of January, a process which is yet to be fully completed.

However, here too, we see some light at the end of the tunnel. First, international coal prices remain at a substantial discount to domestic Chinese HCC, so any pick-up in demand should be reflected in stronger purchases of seaborne material. Indeed, the destocking as illustrated by the Mysteel data in Fig 4 has slowed substantially and our latest propriety steel survey indicates that mills are planning to increase purchases going forward.

Fair enough, the shakeout has been more mean than I expected, though I’d not be breaking out the champagne given Chinese demand is likely to get more flaky as the year rolls on and the property market weakens.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.