This weekend saw the release of the Department of Finance’s monthly tracking of the government’s cash flow and it showed that for all of the bleating from certain quarters about the cyclical rebound the deficit is only marginally better than that projected in the supposedly uber-bearish MYEFO.

Craig James at COMMSEC has a note on the update:

In general, the economy is performing better than Federal Treasury assumed in December. It had expected unemployment to be at 6 per cent in the June quarter: it is currently lower at 5.8 per cent. And the economy was tipped to grow by 2.5 per cent in 2013/14. The Reserve Bank estimates 2.75 per cent growth in the year and current annual growth is 2.8 per cent. Importantly nominal GDP is up 4.8 per cent, ahead of the Mid-Year estimate of 3.5 per cent.

The improvement in the economy is reflected in GST receipts: up 6.6 per cent on a year ago to record highs and around $800 million above the assumed profile.

Tax revenues are up 4.9 per cent over the year with net personal tax up 5.2 per cent.

On the expenses side of the equation, interestingly health spending is largely unchanged and by far the largest component – social security and welfare – is up just 3.2 per cent. But notably public debt interest is up $1.2 billion or 10 per cent, economic services (includes Agriculture, Mining & Transport) is up $2.5 billion or 8.6 per cent while education spending is up $1.5 billion or 5.4 per cent.

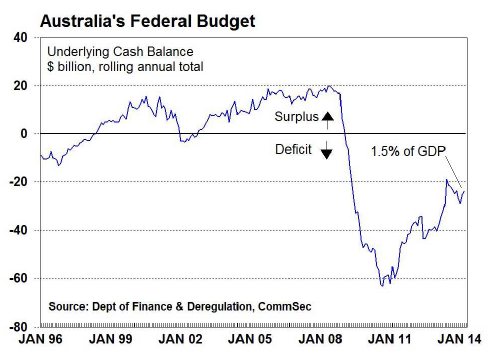

Better, yes, but only just:

Advertisement

The Government noted: “The underlying cash balance for the year to 31 March 2014 was a deficit of $34,783 million, compared to the Mid-Year Economic and Fiscal Outlook (MYEFO) profile deficit of $35,814 million. The difference of $1,031 million relates to lower than expected cash payments partially offset by lower than expected cash receipts, excluding net Future Fund earnings.”

A lousy 3% ahead of forecast after five months, with the best of the house price boom behind us, consumer confidence and the terms of trade under intense pressure, a higher dollar than projected and the capex cliff dead ahead.

The Government will set itself up for failure if it upgrades its growth forecasts in this week’s Budget, which seems to be the goal of certain Labor-biased commentary.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.