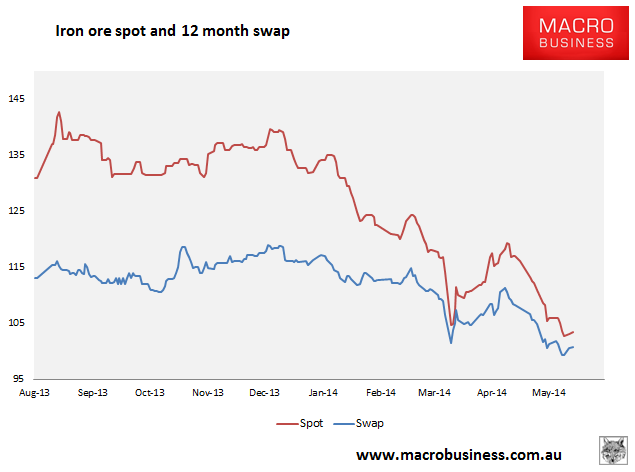

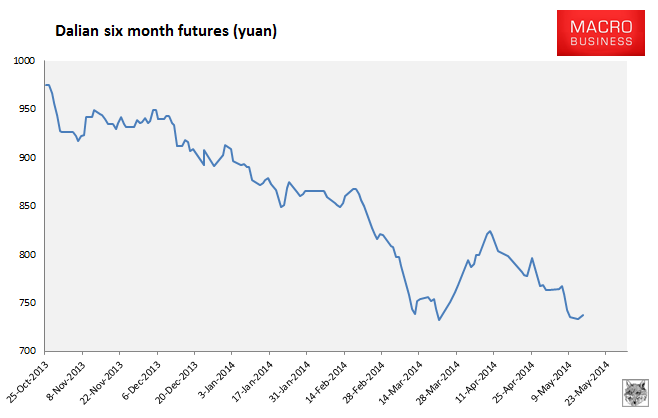

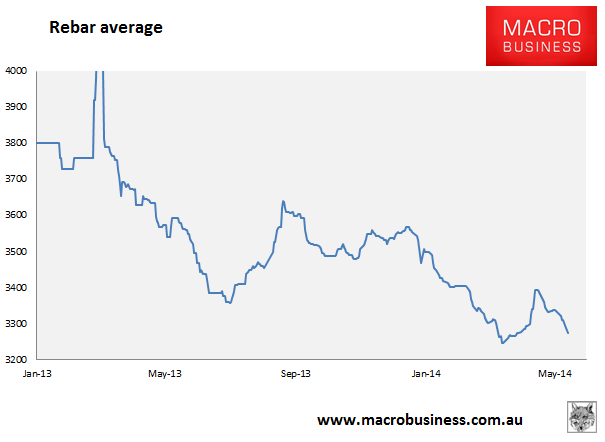

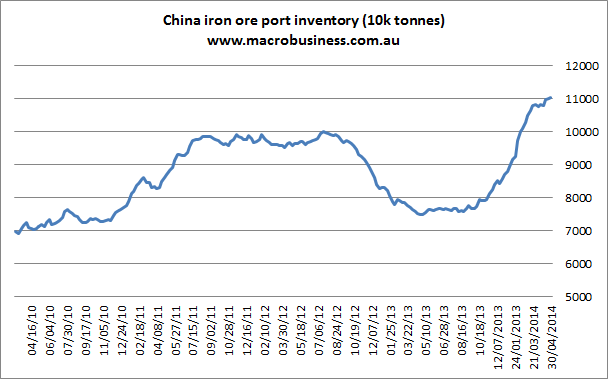

Here are the iron ore charts for May 14, 2014. Note that this is two days of data:

So, paper markets mixed with rebar futures bounces along the bottom. Some stability in physical and the Baltic Dry capesize rose 3.5%. However, port stocks rose again last week to another record and rebar average is collapsing once more. All of this despite the average daily output for steel in April reaching a record high of 2.29 million tonnes per day. The markets is swimming in steel and pricing power evaporating. Reuters has more:

A potential workers’ strike at Australia’s Port Hedland, which could halt a fourth of global iron ore shipments, has not deterred bearish investors from bidding down prices, arguing a shortage in supply may take weeks to be felt given towering stockpiles at ports in China.

…A flagging housing market in China is hurting sentiment towards the iron ore and steel sectors. China’s central bank has asked commercial lenders to hasten approval of housing loans amid tighter liquidity that has helped cool the property market this year.

“The physical market for steel is not that good and people are pessimistic because of what’s happening in the real estate market. They are very reluctant to buy,” said an iron ore trader in China’s eastern Shandong province.

PBOC stimulus and supply threats and we still can’t get a bid. The market is weak and the reason why is simple:

The trading firm is looking at buying a cargo from Fortescue which is offering an 8.5 percent discount to the Platts 62-percent iron ore index price for June cargoes for its lower grade material with iron content of 56 to 57 percent, he said.

That was a deeper discount to the 7.5 percent that Fortescue offered for May cargoes and the 6.5 percent cut in April, the trader said.

“They give very attractive discounts. I don’t think the other big miners are doing that,” he said.

Too much steel, too much ore.