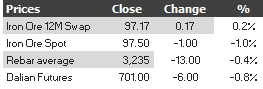

Here are the iron ore charts for May 20, 2014:

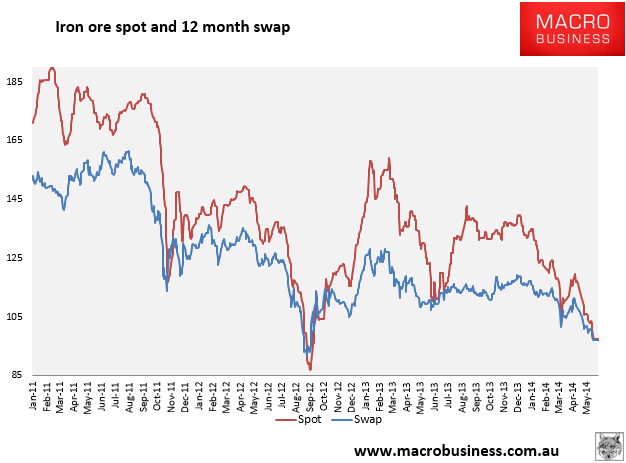

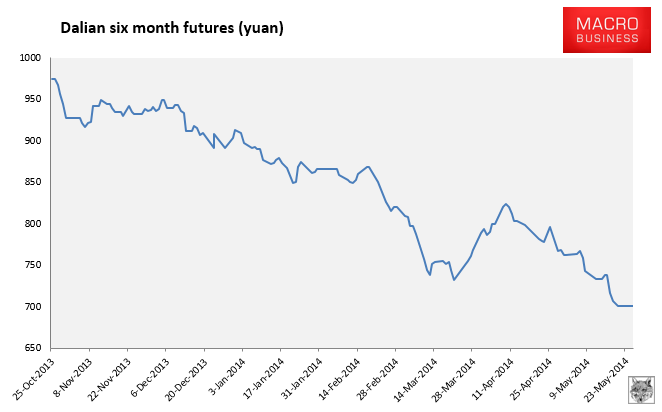

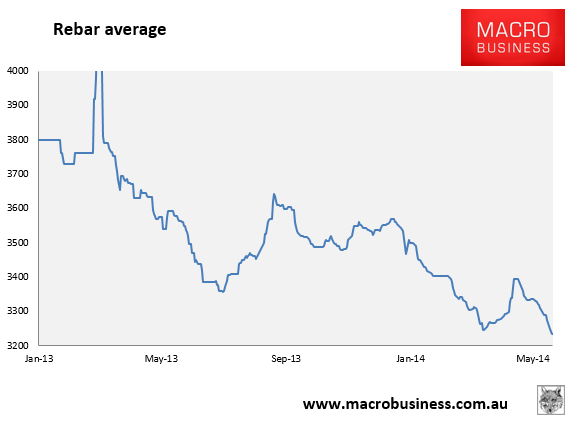

No let up. Paper markets were very weak with rebar futures at new lows. The 12 month managed a tiny bounce but, jeez, it’s unconvincing.

Physical markets are showing no panic but it’s a relentless grind lower and the Baltic Dry capesize component tanked 5%.

The AFR has one explanation:

Ji Minlei, a trader who operates from the port of Rizhao, said pressure from banks partly explained why the iron ore price had dipped below $US100 a tonne for the first time since September 2012.

“Some traders have been caught in the liquidity crunch and have been forced to sell,” he said via phone on Tuesday.

Mr Ji said banks had been increasingly tightening credit this year and were now demanding deposits of up to 30 per cent to finance cargoes, double the previous level.

“The biggest risk to the price now is that banks further tighten credit,” he said.

Fair enough but that is not the market’s biggest problem and is also contradicted by still rising port stocks. The real problem is the steel price. Rebar average just carved through the recent low like a hot knife through butter and until it stabilises then the pressure to destock raw materials will remain. Indeed, I don’t think that current record levels of steel output can persist either with prices tumbling like this.

That raises the prospect that my Q3 destock thesis is happening right now and we’re going lower.