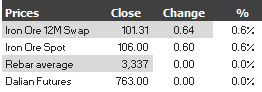

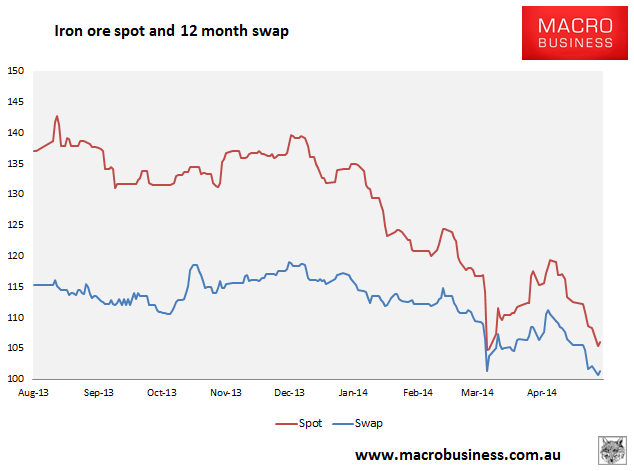

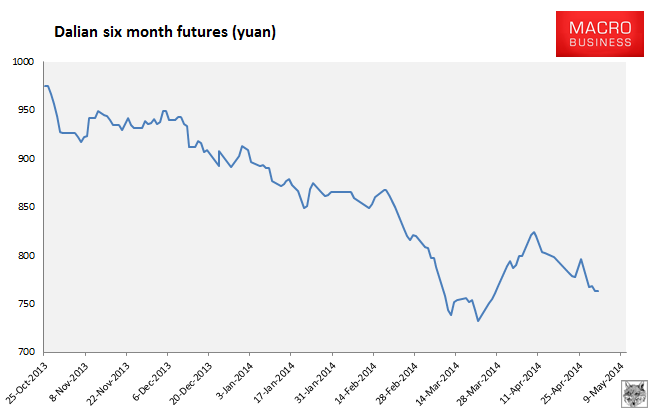

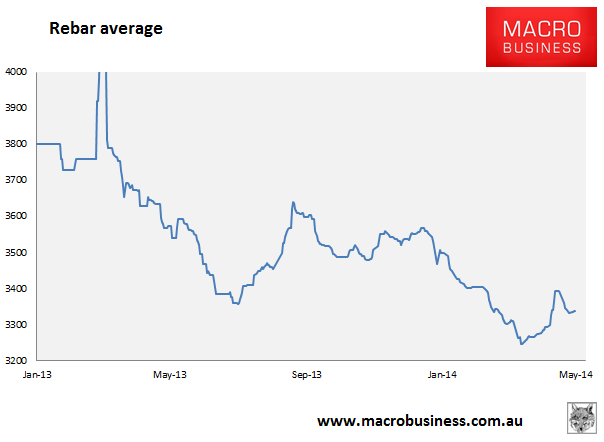

Here are the iron ore charts for May 1, 2014:

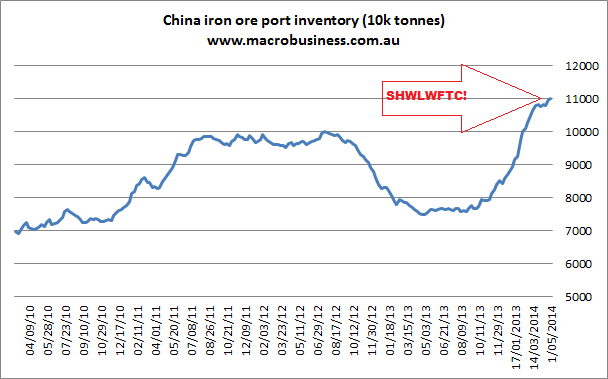

Chinese markets were still closed. 12 month swap managed a small gain, physical too. The Baltic Dry capesize component has surged 14% in two days suggesting current low prices are tempting mills. I’ve had to invent a new acronym to describe the port pile which is up again marginally on the week. Guess it if you can.

A range of macro Chinese indicators have stabilised in recent weeks and steel output has bounced with them. The Chinese infrastructure non-stimulus appears to be working for now. The property sector remains in a downdraft and the major risk to renewed weakness in steel output.

That has the press cogitating on “peak steel” in China:

There’s a disturbing new phrase being uttered by bears in the resources game – “peak steel”.

And it’s a very different phenomenon to the “peak oil” theory, where supply dries up and energy prices soar.

Peak steel is all about too much supply, not enough demand and tumbling prices.

While not conclusive proof, the recent fall in iron ore prices is showing there is a significant rebalancing of supply and demand going on.

Certainly the steely gaze of the all-powerful China Banking Regulatory Commission (CBRC) has unnerved the market and accelerated the price slump after a mini recovery early last month.

In March the CRBC signaled that it will strangle credit to steelmakers who pollute or overproduce.

A month later the CRBC broadened its attack, vowing to pursue the more speculative end of the market where iron ore inventories are used to secure lines of credit.

The Shanghai-based industry website Mysteel suggests that as much as 40 per cent of port inventories are used as collateral to finance other deals.

Adding to the regulator’s displeasure are reports of traders defaulting and fleeing the country.

Brokers at UBS suggest this rather unsettling behaviour could see “an unknown amount of inventories being liquidated to secure cash and avoid investigation”.

Clearly any rush to the exits by traders is not great news for anxious iron ore miners looking for a significant change in sentiment.

…In a recent report, the analyst team from brokers CLSA noted that “peak steel demand would be seen this decade rather than next.”

The CLSA research cited factors such as “the slowing pace of urbanisation and demographic trends which are going sharply into reverse.”

Increasingly Chinese developers are reducing their land banks and building smaller apartments, with floor-space construction falling 27 per cent in the first three months this year.

Overall, CLSA forecasts a 37 per cent decline in private property floor-space sales between 2013 and 2020.

CLSA says steel consumption in the property sector is likely to peak this year, and a similar scenario is developing in infrastructure.

“We also forecast infrastructure steel consumption to peak this year, with steel demand from road and rail construction to decline,” the analysts noted.

CLSA suggests that, rather than being an absolute cut in spending, projects will be become less steel intensive.

“Major infrastructure backbones such as the national highway network and high speed rail network have largely been built out,” the firm observed.

“The next round of spending will increasingly focus on more local level/linkage infrastructure which is less steel intensive as it involves fewer big bridges, tunnels and elevated sections.”

As I have observed many times, in economics it’s the rate of change that matters, not absolute levels. China can keep building huge amounts of everything for ever but if it’s not more than the year before then iron ore is going to sink. Peak steel is probably closer even that this article implies.