Here are the iron ore charts for May 15, 2014:

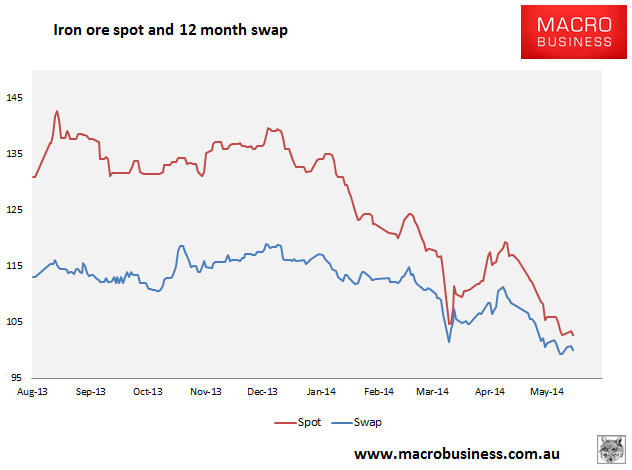

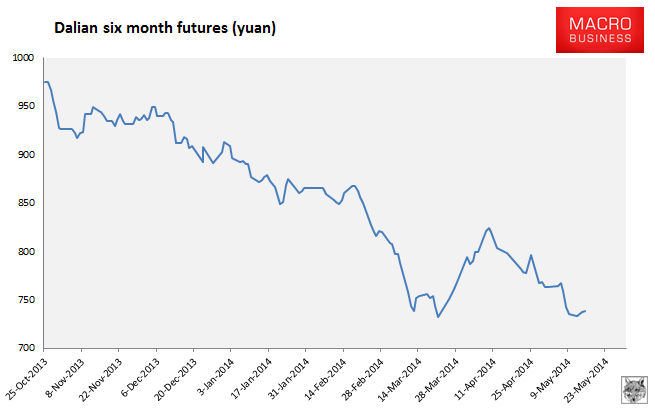

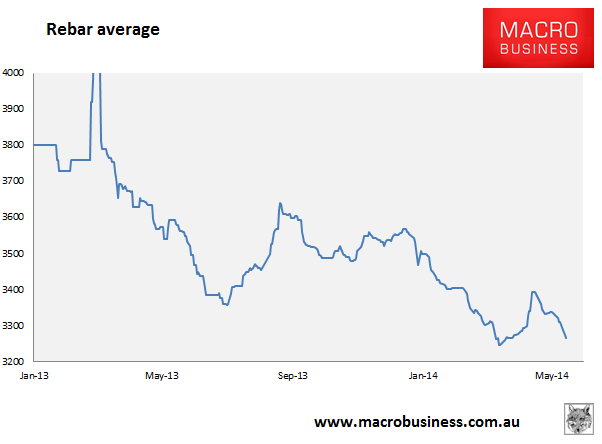

Paper markets are weak or weaker with 12 month swaps struggling to get above $100, Dalian 6 month hanging at record lows and, most importantly for the future, rebar futures plumbing record depths daily.

Physical is just as bad with iron ore spot still biased to test $100 and rebar average chasing futures into the abyss. The Baltic Dry capesize component was a little relief rising 3.5%.

The texture via Reuters is all gloom:

After a brief seasonal spike in steel consumption in April, Chinese demand weakened this month, forcing traders to destock, said Helen Lau, senior mining analyst at UOB-Kay Hian Securities in Hong Kong.

“Downstream demand has turned weak and the only way to sell to the market right now is to lower your prices,” said Lau.

Inventory of five major steel products held by Chinese traders, including rebar, fell to 15.98 million tonnes as of May 9 from from 16.47 million tonnes the previous week, according to industry consultancy Mysteel.

…”China is undertaking these mini-stimulus measures, but we’re not sure when it will happen or if it will happen at all,” said Lau.

“Now the Chinese market is very, very weak, stocks at the ports have been increasing, and I heard that some mills cannot get letters of credit because Chinese banks have limited lending so the iron ore price must go down,” said an iron ore trader in Rizhao in China’s eastern Shandong province.

And more from Platts:

A Hebei-based steelmaker said buying activity among the end-users was still sluggish, but he had not expected prices to slide so quickly. “Everyone is still very cautious and the volatility is not helping convince people to start buying again.”

“Mills, especially those in the north of China, are not actively trying to buy seaborne cargoes now,” a Zhejiang-based trader said. “They’d rather go to the ports to purchase cargoes because prices are still cheaper there and there are high volumes for the taking.”

…Additionally, some sources said there was no lack of spot supply of iron ore as major miners like Australia’s Rio Tinto and Brazil’s Vale were continually offering cargoes, a factor that was only going to put pressure on prices in the longer term.

“It is like our daily bread,” a Singapore-based trader said of the spot offers that were flowing into the market every day.

…”Most people thought that once prices went near $100/dmt [CFR China], a rebound was necessary, otherwise any improvement [in the iron ore and steel markets] would be impossible. Another point is that $100/dmt is the cost of domestic ore,” a Hong Kong-based trader said.

Wasn’t it supposed to be $120? It’ll end up being closer to $80.

So long as the port pile is there as a counter-weight to the mining oligopoly and downstream steel demand remains weak even as production pumps at record highs, the pressure to destock raw materials will remain.

We’re into the lamer for longer period.