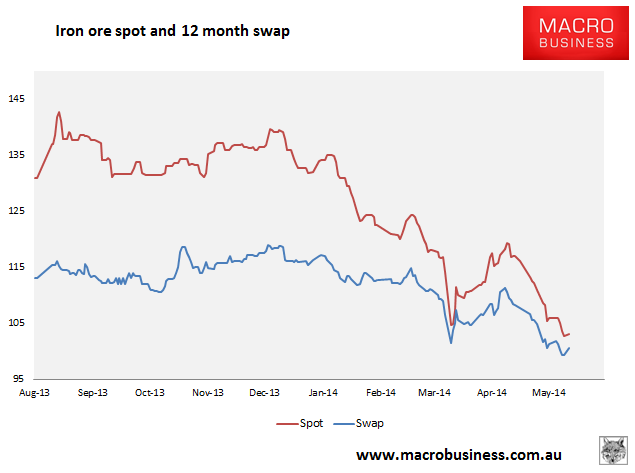

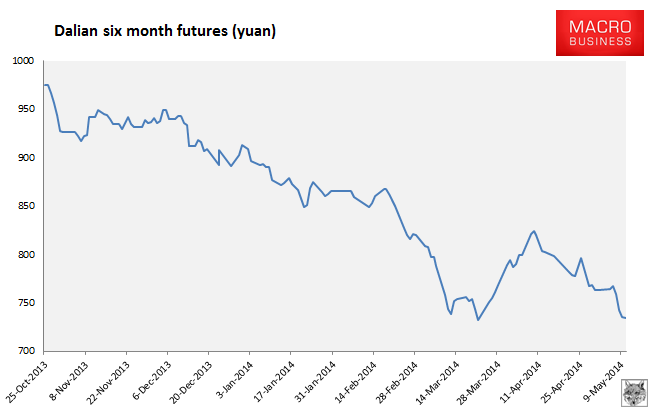

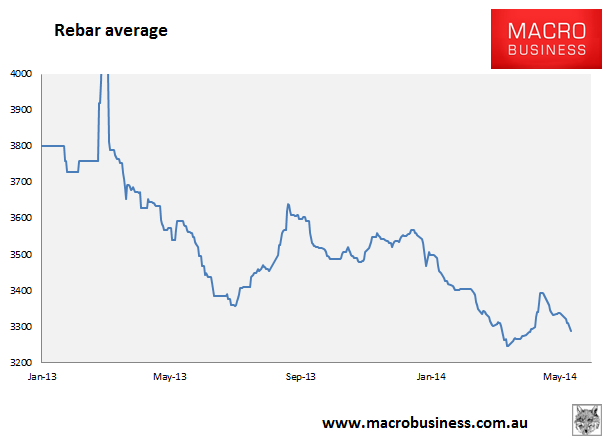

Here are the iron ore charts for May 12, 2014:

Iron ore paper markets rallied following the news of strike action in Port Hedland after trading much of the day down. Rebar futures also managed a little bounce.

Physical markets are still weak with the rebar average now in free fall and the Baltic Dry capesize index down another 4%. Spot obviously held up better. Reuters suggests some renewed buying interest on lower prices:

“I think a price lower than $100 is very possible right now. However, many buyers are asking for cargoes after the latest price drop so the market seems a little warmer,” said an iron ore trader in Rizhao city in China’s eastern Shandong province.

…Baoshan Iron & Steel Co Ltd (Baosteel), China’s biggest listed steelmaker, slashed prices for a second straight month in June. “We think Baosteel’s price cut will further dampen market sentiment towards steel sector. If steel prices cannot be held stable through June, then it will be less likely to see a rebound through the slow summer season in July and August, in our view,” Helen Lau, a senior mining analyst at UOB-Kay Hian Securities, said in a note.

Steel mills are not the only ones furiously discounting. From Platts:

Fortescue Metals Group, Australia’s third-largest iron ore miner, has offered deeper discounts to its contract customers for June-loading cargoes of its main iron ore products, compared with May-loading parcels, customers of the miner told Platts this past week.

FMG uses the Platts 62%-Fe Iron Ore Index assessment to price its iron ore, making a price adjustment for the iron content for each grade, and typically offers its contract customers a discount that depends on market conditions.

Several contract customers of the miner told Platts they received an 8.5% discount for FMG’s flagship 56.4%-Fe Super Special Fines product for June, compared with a 7.5% discount for May.

For its 58.3%-Fe Fortescue Blend fines, FMG has set its June discount at 5%, according to several customers, up from 4.5% for May.

A source at a steelmaker in central China said there was a supply overhang of 56-58%-Fe grade fines in the spot market, adding that the miner has to offer wider discounts to term customers so that they will keep to their contractual volumes.

Discounting contracts before they adjust on the usual formula of an average of the past three month’s spot price is indicative of serious price pressure. Better news for producers comes from India:

Optimism triggered by the lifting of a ban on iron-ore mining in the western Indian province of Goa last month, seems to be fast dissipating with the threat of such bans looming large once again in other parts of the country.

For one, a fresh ban on iron-ore mining looms over the eastern province of Odisha with the Supreme Court expected to deliver a verdict on illegal mining in the region.

…The Supreme Court, hearing cases of illegal mining across the country, has maintained that in the case of Odisha, automatic renewal of mining leases, after the first renewal period of 20 years, was illegal. Miners were currently awaiting further verdict.

With the possibility of the court slapping a ban on mining, the sword of Damocles hanging over miners was how many of the mines in Odisha would come under the threat of the ban, even if the court did not order a blanket prohibition on mining.

Though definitive figures were not available from the mining industry, several miners said that 22-million tonnes a year of iron-ore could be knocked off national production figures if mines operating under automatic renewal of lease were to be banned from operating by the court.

…Odisha was the largest iron-ore-producing province in the country, accounting for around 45% of the country’s total annual production.

I still expect Indian exports to climb this year as Goa resumes mining given it’s output is nearly all export oriented.

Meanwhile, hope springs eternal for Aquila shareholders:

SHARES in takeover target Aquila Resources continue to hover comfortably above China’s bid price as the market continues to bet on a sweetened offer.

Chinese state-owned entity Baosteel launched a $3.40-a-share bid for Aquila on Monday last week in a $1.4 billion move to secure ownership of significant iron ore and coal assets in Australia.

Shares in Aquila have traded above the bid price since it was launched and yesterday the stock closed up 1.75 per cent at $3.48.

Analysts have said that an increase in the original bid would be needed to gain the support of company founder and executive chairman Tony Poli, who controls about 30 per cent of the stock. But the Chinese, which have teamed up with Australia’s Aurizon in a joint bid, set a minimum acceptance level at 50 per cent, meaning they can take control of the company without Mr Poli’s support.

Now that’s just downright greedy! Given the outlook, the bid is bonkers to begin with.

The immediate outlook is complicated by the supply threat in the Pilbara. Given what’s at stake you would think that the unions will win before any actual strike action but that’s pure speculation. Beyond that, the outlook remains weak, weaker or weakest given tumbling steel prices and the pressure to destock raw material, and on China’s seeming willingness to drive its property slow down further.