China was closed yesterday for the May Day holiday so there’s no price update. The Baltic Dry capesize component fell 1%. Today’s news is all about denial. From Rio‘s Andrew Harding:

“At the moment you see a lot of stories about iron ore prices down — is it the end of the world?” he asked.

“I don’t pay any attention to that.

“When the iron ore price goes up I feel good. When the iron ore price goes down I don’t feel good, but the reality is that I actually don’t care about it because the issue is the long term.”

From Vale’s Jose Carlos Martins:

”We expect that the price in the second half would be better than the first half,” he said. ”Nothing is for sure but the price will not fall below $US110 on a sustainable basis.”

From Roy Hill’s Barry Fitzgerald as Gina dug her first dirt:

…predictions that no more large resources projects would be built in Australia were premature.

But the prize for denial goes to Atlas Iron’s Ken Brinsden:

“There is constant and growing demand for steel production in China and that will lead to continued demand for seaborne trade,” he said.

“And the Chinese market is still overly reliant on high-cost domestic production, which needs to be balanced out [by imports].”

…Mr Brinsden is confident the iron ore price will recover to hold well above $US110 in the short term. “An average price between $US110 and $US130 a tonne is not an unreasonable place for market to be for at least the next couple of years,” he said. “And long-run pricing north of $US95 a tonne is absolutely conceivable.

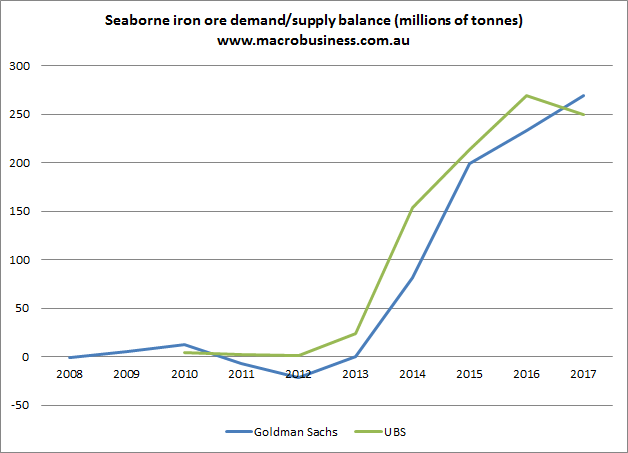

Carn, Ken. Current steel production in China is growing at a healthy 4% year on year and the oversupply situation is much better than it’s going to be:

As China slows some more and the supply ramp up goes on the intensity of denials will need to intensify.