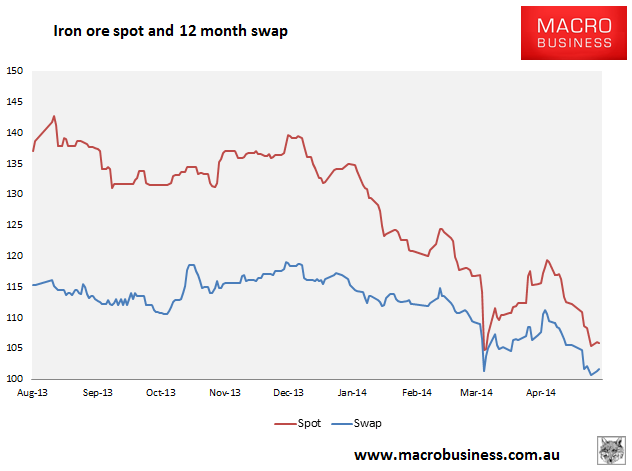

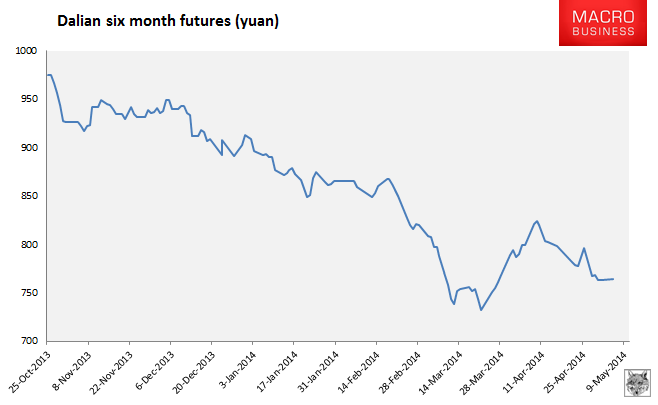

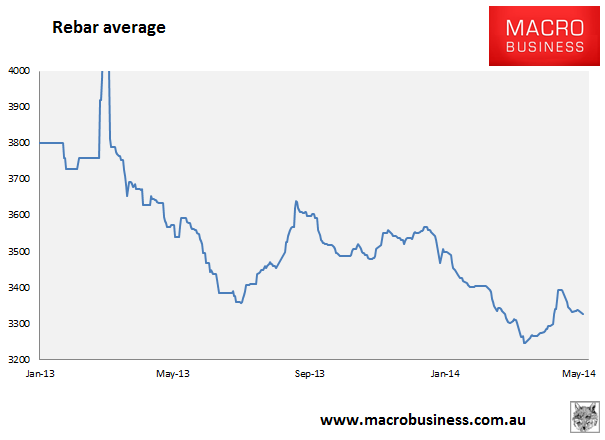

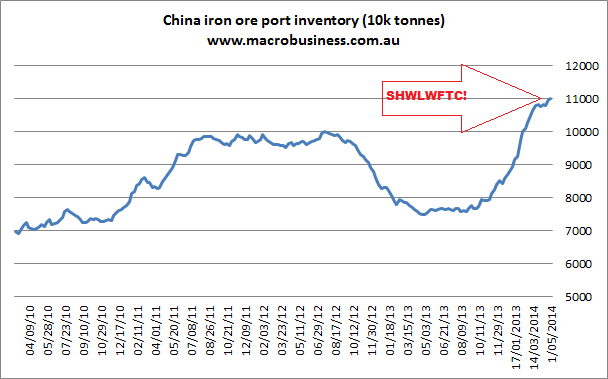

Here are the iron ore charts for 5th May, 2014:

Not much to say for either paper or physical markets on sideways movement. Rebar futures were the same . No update on the BDI today. In news, the China steel PMI leaped into positive territory yesterday up 8.4 percentage points from March to 52.6% in April. Also, there’s more feel good commentary on the Baosteel purchase of Aquila.

From Rowan Callick:

This is China Inc no more insisting on minimising risk by buying full ownership of a project but seeking to work with strategic partners — a path successfully pursued by the Japanese resource-based conglomerates over the decades.

The largely positive reception so far of the news of the deal indicates also a maturing of understanding in Australia of the value of our giant trading partners locking in their commitment by investing here.

The move amounts to a vote of confidence in iron ore as a core driver of China’s continued growth, despite the slowing of the overall economy, as overdue steps are taken to rebalance the economy from its reliance on manufactured exports and on infrastructure inputs to domestic consumption and services.

Meh, that’s over the top. Matthew Stevens is more incisive:

Given Chinese product costs more than anything imported, the likelihood is that its Pilbara output would replace Chinese rather than Australian supply. As the highest-cost Chinese material is bounced out of the system, the replacement cost that has driven iron ore pricing since China opened its doors to imports will drift lower for longer, which might have some wondering if it is a good idea that a major customer for Australian iron ore like China Inc should be a major producer.

That makes much more sense but $7 billion to develop is still a huge price for only $30 million tonnes of iron ore, even with cheap Chinese capital.

P.S. Yesterday’s acronym guessing competition produced no winner:

It was tough one: Screaming With Laughter Waiting For The Crash!