So now we know why iron ore miners surged yesterday as prices tanked. From Citi yesterday:

Iron Ore: Cyclical Bottom, but Bear only Hibernating

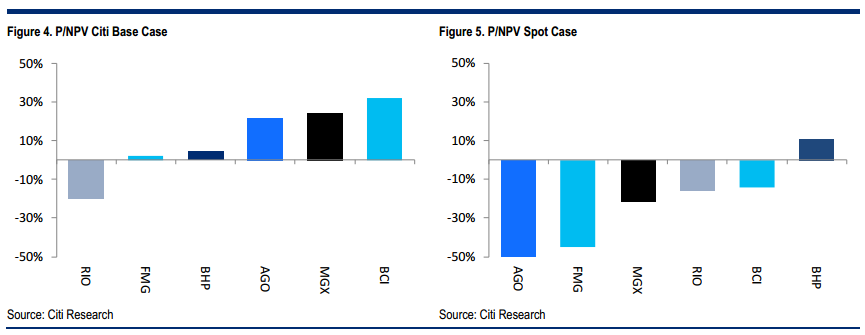

What’s Changed — In March we downgraded iron ore stocks on expectations that the wave of new supply and stickier than expected Chinese production would drive prices significantly lower – There’s a Bear in There. With iron ore now below our forecast of US$108/t, and stock prices significantly lower, we upgrade a number of recommendations and take a more positive cyclical view. However, we remain structural iron ore bears with price forecasts of US$90/t in 2015 and US$80/t in 2016.

Recommendation Changes — Key recommendation changes are upgrade of Rio Tinto (TP A$71/sh) and Fortescue (TP A$5.50/sh) to Buy, previously Neutral. Atlas (TP A90¢/sh) and Mt Gibson (TP A75¢/sh) upgraded to Neutral, previously Sell. BHP Billiton (TP A$38/sh) remains Neutral rated and BC Iron (TP A$3.60/sh) remains Sell rated. All target prices remain unchanged.

Year to Date — Despite Chinese mills being back in the black and steel production rates improving, iron ore has continued to drift lower as expansions and a mild Pilbara wet season have seen supply continue to increase, keeping Chinese port stocks at >100mt. Without the seasonal inventory draw there has been no “panic” buying that has characterised 1H iron ore price spikes in recent years.

Cyclical Bottom — We expect the supply growth rate to slow in 2H14 as RIO/FMG hit targeted 290/155mtpa rates by mid-year. Combined with continuing recovery inChinese steel production as liquidity conditions ease – Calling a Cyclical Bottom, we see near-term upside to iron ore price and stocks. Key risk is that improving liquidity does not flow through before summer slowdown, which with iron ore arriving unabated could drive price below the financially and psychologically important level of US$100/t.

Bear Hibernating — This cyclical call does not change our structurally bearish view on iron ore that increased seaborne supply, largely from Australia, and less price sensitive than expected Chinese domestic production remaining in the market.

This is wrong in my view, as I described this morning. The key is the fourth paragraph and the assumption of “improving liquidity”. On what one might ask? Chinese interbank markets have eased from last year but there has been no suggestion that the prudential measures that are hitting housing and steel have been relaxed. On the contrary. Thus, falling interbank rates and rising liquidity are more likely to be the result of slack demand for borrowing, not easing by the PBOC.

China may ease up on property and steel at any time, and if you think they’re about to do it then Citi is right. I don’t.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.