Today’s capex numbers showed a big mining capex cliff, an unfolding disaster in manufacturing investment and surprisingly strong lift in the “other” category that we can largely see as services.

I’ve unpacked the surprise and you’ll probably be less startled to discover that it’s all about a FIRE industry launch: Finance, Insurance, Real Estate and Retail.

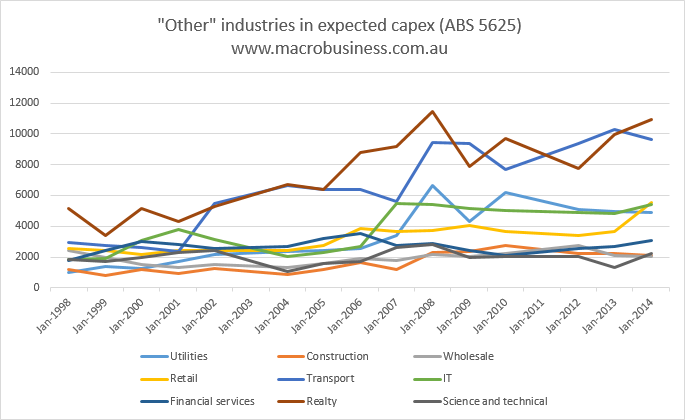

Here’s the chart (expectations for the year ahead):

Note that this does not include dwelling construction unless it were for a buy-to-let business. Red, dark blue and brown say it all!

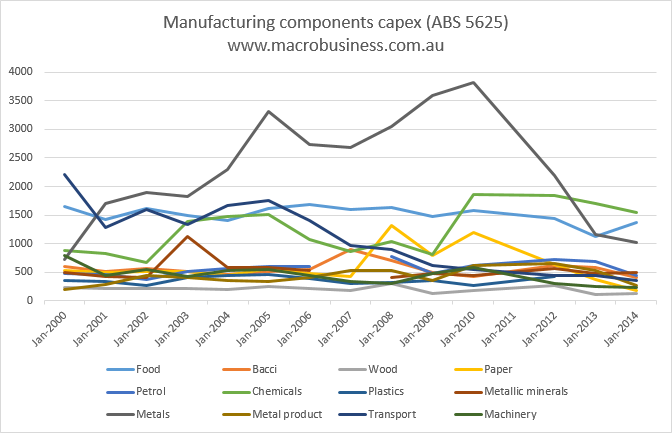

Meanwhile, in the tradable sectors of manufacturing it is universal carnage, most especially in metals processing:

Houses and holes forever!

Has this changed my view of the interest rates outlook? A little. It is strong enough to satisfy the RBA in some smallish measure that their rebalancing is on track so the risk of a pre-October rate cut has diminished unless iron ore just keeps on falling.

But I reckon the report is actually a bit backward looking because it will not fully capture the post Budget malaise. As such, I expect the strong lift in services investment intentions to wind back as the year goes on and be especially vulnerable to a consumer shock. There was also a lift in mining intentions which can’t be trusted.

My October rate cut call is unchanged.