I’ve been waiting for some bullhawkian budget replies but so far have been more impressed by the silence. Yesterday The Kouk posted an argument on how large a government Tony Abbott intends run:

Mr Hockey’s first budget allows me to update my ‘size of government’ comparison, which I first published on 1 May 2014. It is reproduced in full, below.

For the sake of simplicity, the size of government is calculated by adding revenue and spending as a share of GDP, to see what sort of footprint any particular government has in the economy.

It is early days for the Abbott government, to be sure, but the budget shows that the size of his government will be 49.1 per cent of GDP, calculated on the period from 2014-15 to 2017-18.

This is a smidge below the Howard government (49.2 per cent) and the Hawke / Keating government (49.6 per cent), but is significantly larger than the Rudd/Gillard government (47.4 per cent).

In other words, the Abbott government looks like reverting a high spending / high tax government and unwinding the smaller footprint left by the previous government. The revenue from Medicare copayments, the petrol excise rise, the income tax hike, the levy on big business add to the tax take, but the fact they are recycled to at least part fund the paid parental leave scheme, roads, a medical research centre all add to government spending.

Unless something changes in the years ahead, the Abbott government looks like being a big government.

I’ll leave it to readers to judge whether it is a good or a bad thing.

It’s a good thing given the capex cliff and falling terms of trade though the purpose of the comparison is clearly to conclude the opposite. So the Kouk implies that the Government should be shrinking faster than it is, as well as, as we know, agitating for four rate rises this year. Perhaps he’s thinking of New Zealand.

Meanwhile, Paul Bloxham’s Budget reply was very sound but only made oblique mention of interest rates:

For the RBA, the budget bottom line is unlikely to have been a surprise. In their recent official statement the RBA indicated that they expected to growth in public demand to be ‘very weak’ as the government was expected to plan to consolidate its fiscal position.

That rather implies he sticking to his rate rise forecast by year end forecast.

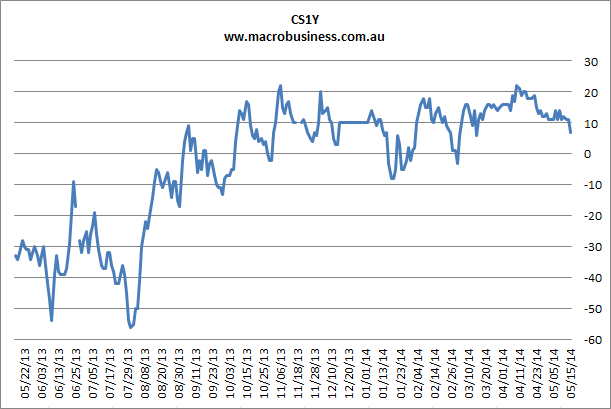

Market reactions, on the other hand, have been more dovish. We know the dollar flew yesterday but that was more about Europe than Australia. The CS1Y interest rate market has almost dropped back to neutral for the next twelve months of rates:

The Budget build-up and actual has knocked about 10bps off rate rises and at this point the market is forecasting 7bps of rises by May 2015. Hardly bullhawkian!

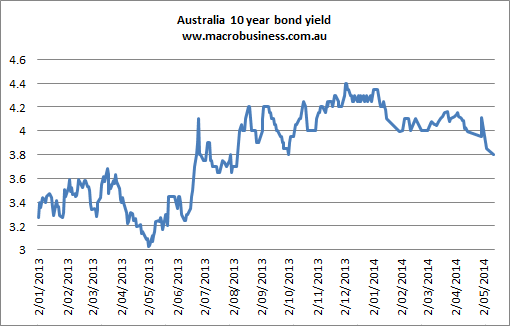

The 10 year bond yield has been more decisive and is down 60bps this year as global bonds yields have comes in and much of that recently:

That’s about the equivalent of pricing one rate cut. I’m with it.