Westpac expects the underlying budget deficit for 2014/15 to be announced by the government as $26.0bn on Budget night on May 13. That is about $8bn lower than the estimate from the government’s Mid Year review of $33.9bn.

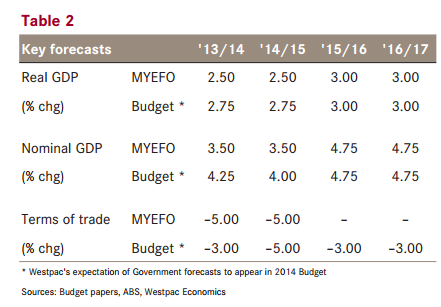

• The improvement will come from a modest increase in the government’s nominal GDP growth forecasts, 3.5% to 4.25% for 2013/14 and 3.5% to 4.0% for 2014/15. That will improve the 2014/15 starting point by $4bn. There will also be a number of policy initiatives on both the revenue and spending sides (a further $5bn). Partly offsetting the reduced spending initiatives will be a $1bn increase in infrastructure investment.

• On the revenue side it looks likely the government will announce a temporary deficit levy raising $1bn a year and a lift in the fuel excise, also raising $1bn a year.

• On the expenditure side there are likely to be net spending cuts of $3bn including a tightening of eligibility conditions for family tax benefits.

• The government will be able to announce this near term budget outcome as a considerable success by reducing the underlying deficit from 3.0% of GDP in 2013/14 to 1.6% of GDP in 2014/15.

• Given the strong rhetoric from the government in the lead up to the Budget these “savings” appear to be quite modest. However, they will be in line with the principles set out in the Committee of Audit which focuses on the medium term and returning the budget to a respectable surplus (1% of GDP) by 2023/24. Note that the near term spending savings envisaged by the Committee are modest: $2bn in 2014/15; $3bn in 2015/16; and $5bn in 2016/17.

• To identify the magnitude of that challenge we can look to the Committee’s sources of long term savings to reduce outlays by $60-$70bn per annum by 2023/24. The key sources of those savings are: pensions, $10bn; health, $20bn; family assistance, $7bn; foreign aid, $5bn; and $20bn from other programs including defence; schools; universities; industry assistance and government departments.

• The government will not adopt all of the initiatives suggested by the Committee, so the likely projected surplus is likely to be reached a little later than the Committee’s target of 2019/20. However, we expect the broad mix of savings to be quite similar.

• Westpac is in broad agreement with the government’s near term growth forecasts. Further, we do not believe that the new policies , including the levy, will make a meaningful impact on consumer spending.

• We also point out that the expected near term stance of the Budget will be significantly less contractionary than the first Howard/Costello budget in 1996. That budget included net savings over the 3 years of 3.1% of GDP compared with our estimate for this budget of 1% of GDP.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.