Westpac has produced a more detailed take on today’s TD Securities monthly inflation number:

The Gauge rose 0.4% in Apr following a 0.2% rise in Mar and Feb and a 0.1% rise in Jan. The annual pace is now 2.8%yr from the 2.7%yr pace in Feb and Mar and builds is building on the reported 2.5%yr pace in Jan. The Gauge is now in the the upper half of the RBA’s inflation target band.

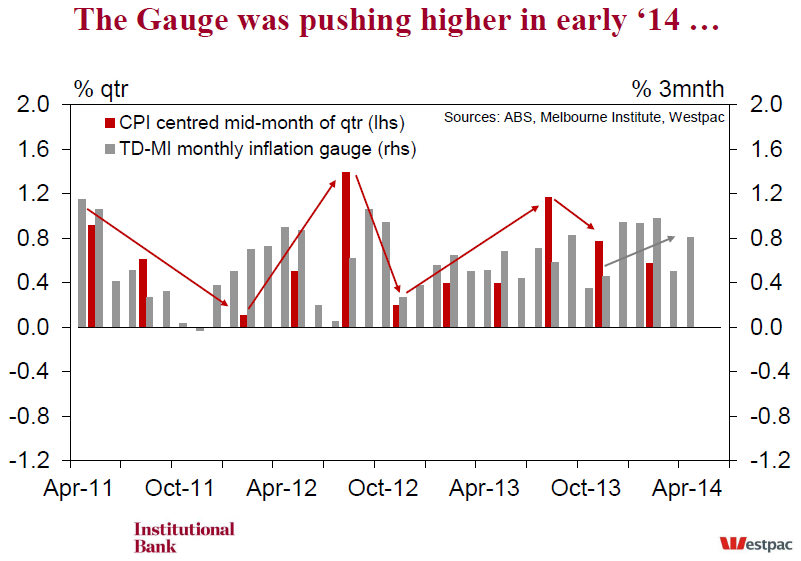

•The Gauge had been suggesting that inflation was easing in 2014 as the annualised three monthly pace dropped to 2.0% in Mar, from 4.0% in Feb and 3.8% in Jan. But in Apr, the pace lifted again to 3.2% suggesting this easing may have been very short lived.

•For Apr, Westpac estimates that there is a seasonal boost worth 0.1ppt for the month meaning that our seasonally adjusted Gauge rose just 0.3%.

•TD-MI reports that contributing to the overall change in Apr were price rises for communication (+2.6%), tobacco (+2.4%), and holiday travel & accommodation (+6.4%). These were offset by falls in fruit & vegetables (–6.7%), clothing & footwear (–2.1%), and automotive fuel (-2.1%). Of note, the price of postal services jumped by 12% in the month.

The trimmed mean of the Gauge jumped by 0.5% in Apr following a modest 0.1% rise in Mar lifting the annual pace to 3.1% from 2.7%yr.

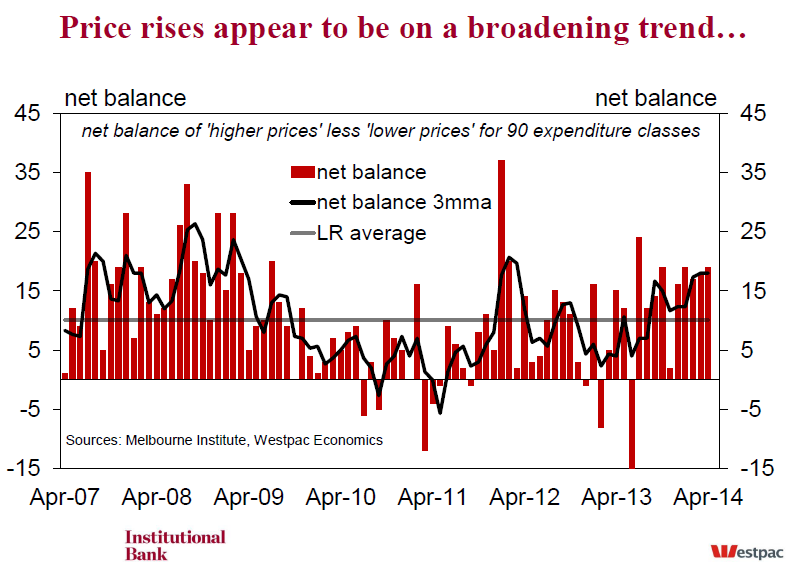

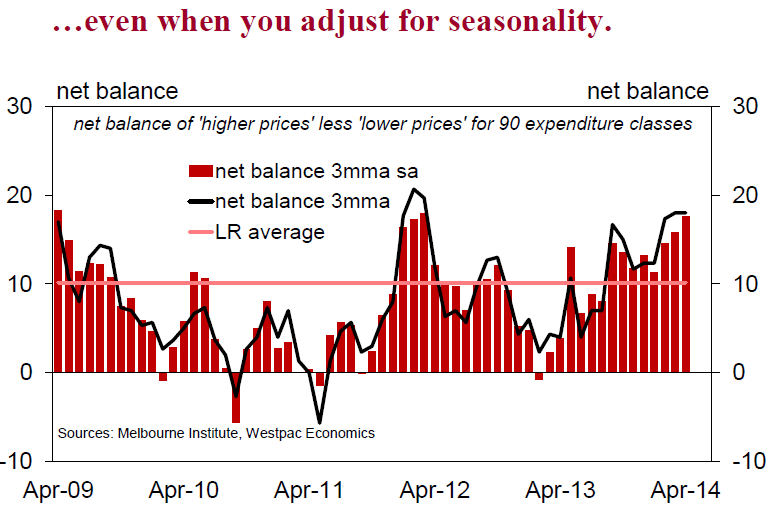

•More critically, the net balance (number of price rises less number of price falls) was 19 in Apr from 18 in Mar and 17 in Feb. As such, it is holding above the long run average of 10. Westpac estimates a positive seasonality in Apr, the adjusted net balance was 17 compared to 21 in Mar. The recent low was 3 last Nov.

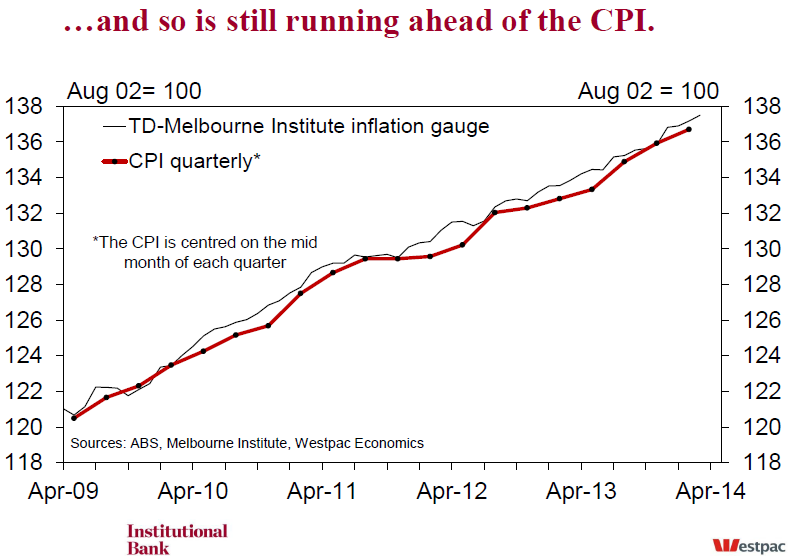

•In the Mar quarter, the CPI surprised with a modest 0.6%qtr and as such, left the Gauge tracking well ahead of it. The Apr report suggests the Gauge continues to run well ahead which, if history does repeat, suggest that at some point the CPI will catch up. So for now, the Gauge suggests some upside risk for the Q2 CPI.

•Westpac’s is currently reviewing our Q2 CPI forecast. As it stands, our forecast is for a 0.5%qtr rise but we have a lot of partial information to process before we lock in an estimate.

The building pressures are real but I remain of the view that the capex cliff and terms of trade falls will outpace the cyclical bounce in the second half.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.