On which note, an interesting development has emerged since banks started winding down their commodity divisions in 2013. According to David Bicchetti and Nicolas Maystre, who wrote a paper in 2012 highlighting increasing correlations between a number of major commodities and indices from 2008 onward, these correlations have now begun to dissipate.

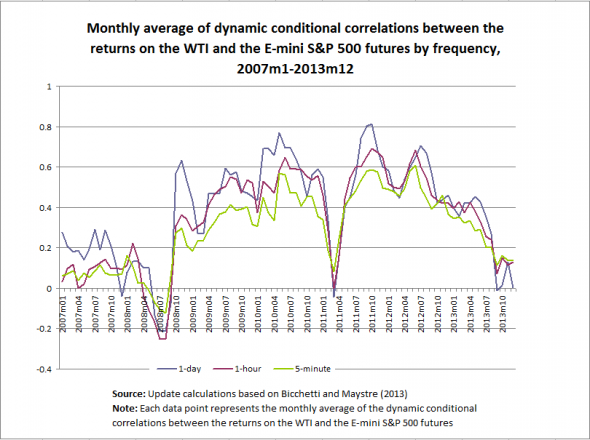

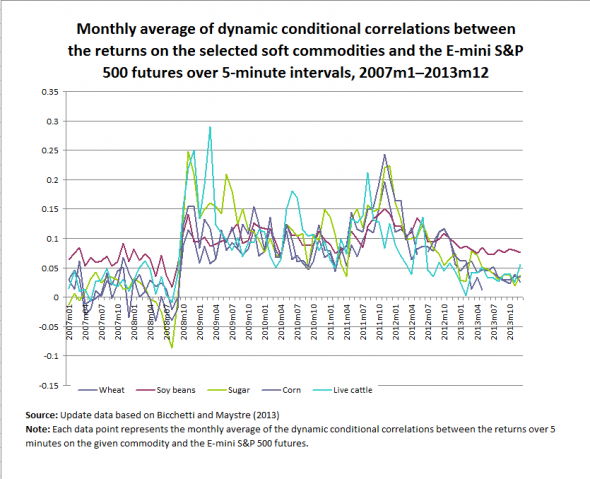

The findings come as a result of an update to their original data set, with the amended charts now looking like this:

FT Alphaville met with the authors last week, who explained that banks exiting commodities could be behind the correlation reversal, which in and of itself is statistically meaningful and therefore worth observing.

Such long-lasting low levels in correlation have not been seen since before the 2008 crisis struck. Back then they were swiftly followed by a spike in correlation, a pattern consistent with what might be expected from a crisis. What is surprising, in the authors’ opinion, is that correlations stayed elevated until at least 2013. The only exception was the breakdown in correlations which occurred in the oil market in the early part of 2011 due to the Libyan crisis.

The two authors argue that the falling correlation is unlikely to be the result of changing fundamentals or US tapering (because it’s still early) and that their research showed commodities are a poor diversification tool given the their propensity to “herd”.

This is chicken and egg stuff. Financialisation played a role, for sure. But so, too, did the 2011 La Nena, MENA crisis, and US QE. For me, though, the primary driver of both the 2008 and 2011 peaks is the correlation with China. Both periods were the very peaks of Chinese demand growth.

Advertisement

It’s classic model for a bubble. A kernel of truth leading to an overblown and ultimately destructive market response culminating in hysteria and crazy correlations.

As the great “super cycle” bubble unwinds on the reset in Chinese growth and the overblown supply response you can, ironically, expect correlations to fall much further.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.