The Kouk has been the harbinger of this cycle to date. He called house prices higher early than the rest of us and is now calling rate rises up earlier than everyone else too. It behooves us to explore the reasons he may be right.

I see three arguments in favour of the Kouk’s position:

- house prices rises are out of control

- inflation is bubbling

- Glenn Stevens is an inflation hawk

The Kouk himself has made the first two points. House prices are an obvious rising financial and macroeconomic risk and there’s no need to repeat that argument again.

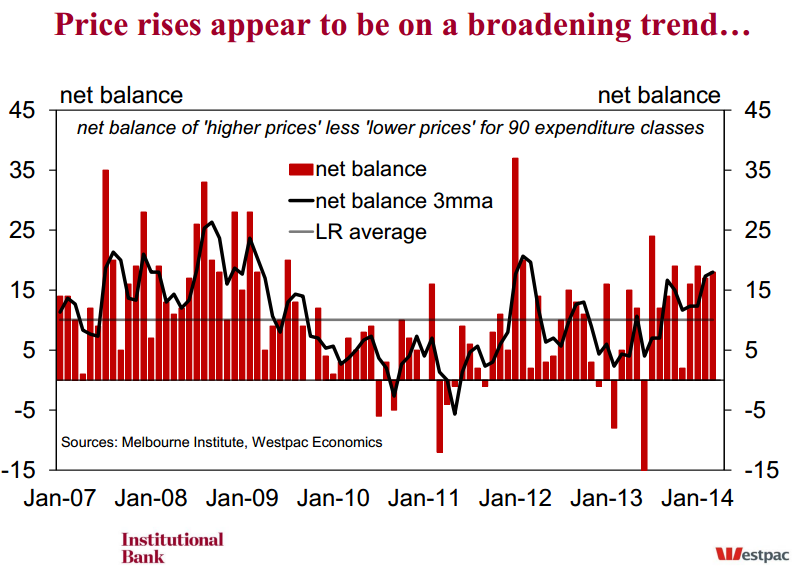

Inflation is also bubbling up. Yesterday’s TD Securities monthly inflation gauge (which the Kouk invented) shows an undeniable broadening of pressures in raw terms:

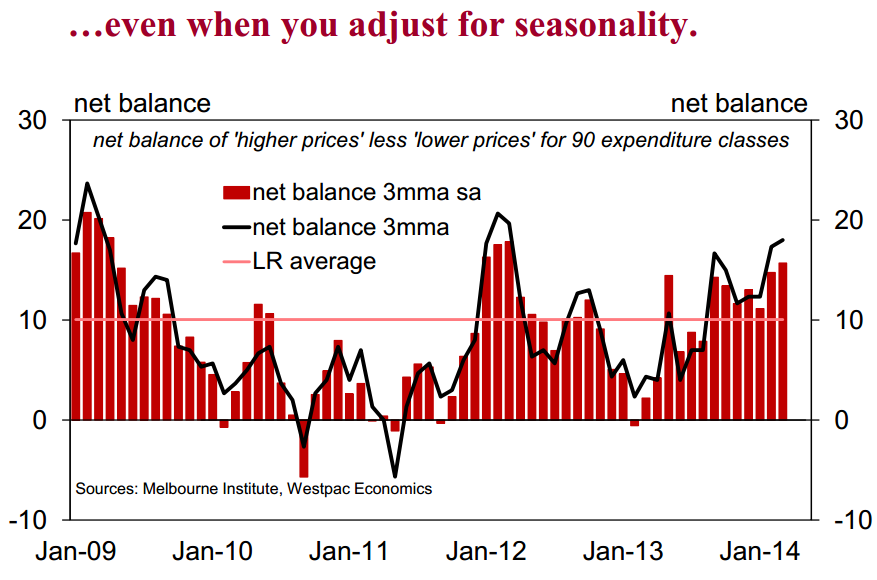

And seasonally adjusted looks bad too:

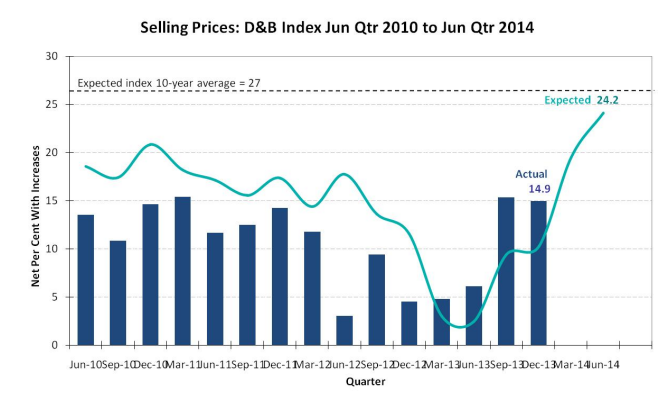

As well, The Kouk now works with the D&B people and helps produce its monthly business expectations survey. It released the following chart today:

In the services economy, the boom in expectations is for price increases above all else. This survey grossly under-represents mining so that is a large downwards price pressure that is missing. Still, it’s an impressive ramp and we all know of the intrinsic price pressures buried in our services economy via land, rents, government fiat etc.

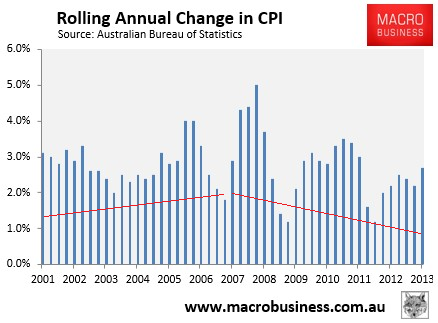

All things equal, this will deliver a 0.7% lift in Q1 CPI and an annual figure of 3.1%, above the RBA target band. The release is scheduled for April 24 and is clearly the basis for the Kouk’s May rate hike call.

The largest argument in favour of the Kouk’s view he hasn’t made himself. It is that the Stevens RBA is an inflation hawk, at least in Australian terms and much more so than its predecessor:

Glenn Stevens jacked rates during the 2007 election. He jacked rates right into the GFC when it was obvious a crash was coming. He jacked rates more quickly and further than anyone else after the GFC. Stevens is a hawk.

So, does that mean he’ll hike the moment the CPI breaches its limit?

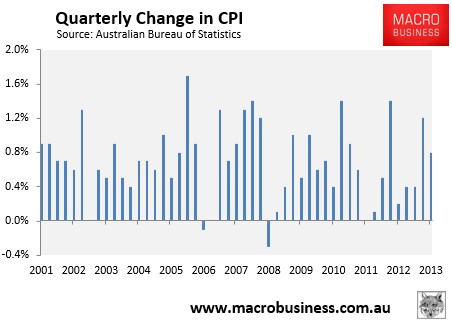

I still say “no” for a number of reasons. First, even if the RBA is spooked by the CPI, it will need a few months to prepare the ground for rate hikes so there’s very little chance of a May hike. The next Statement on Monetary Policy isn’t until May 9 and the RBA would need to shift its growth and inflation numbers first. It would then try a little jawboning for a meeting or two as well. The earliest rise I see if Kouk proves to be right is August, probably after the June quarter CPI. It’s possible it could come in strong as well given the quarterly numbers:

The June CPI number will see another 0.4 reading drop out and if it’s replaced with another 07% or 0.8% then the headline number will be running very firmly in the mid 3% range. The heat to hike will be awwwn.

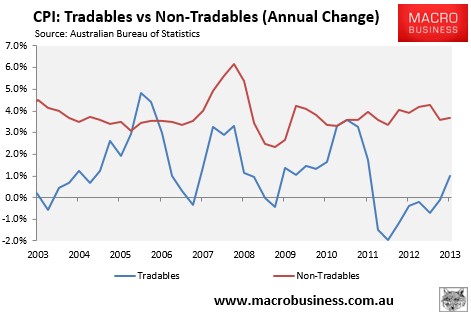

Because the RBA has failed to shift its post-mining boom adjustment frame of reference, sticking to the old script of house prices and services economy to the moon, it will have no basis upon which to argue that temporarily higher inflation is a transient part of engineering lower real income to improve competitiveness. Assuming this all comes to pass, tradable inflation should be peaking by then and ready to fall as the strong dollar has its way:

But, on the basis of its own rhetoric, the RBA may be hoisted on its own hawkish petard just as the capex cliff tears the heart out of investment. If so,all I can say is “duck”!

I still don’t think it’ll happen. In 2011, when inflation threatened, despite the hawkish tendencies of the RBA it went to brink before stepping back. But a similar scenario of rates brinkmanship is not altogether unlikely, maybe even deliberately, to jawbone inflation lower.