Albert Edwards is Society Generale’s uber-bear, the coiner of the “Ice Age’ thesis of decadal credit crunches and bond bull markets, is out today with forecasts for global deflation:

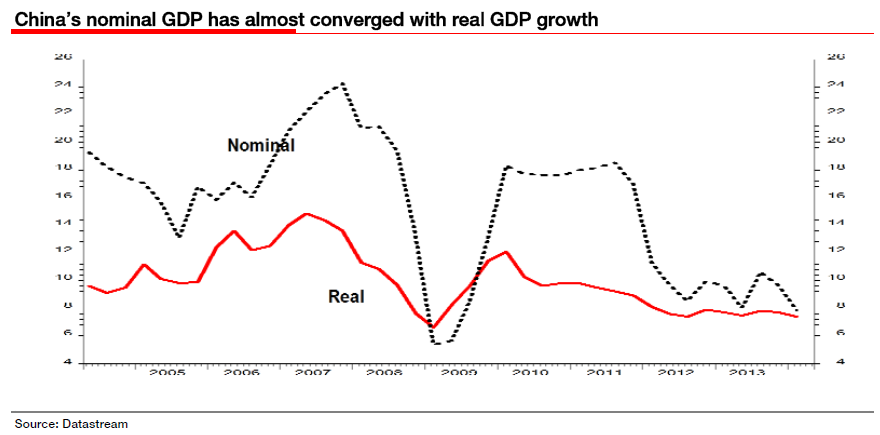

The China data have been on the soggy side recently. The most important figure published recently was not the news that Chinese manufacturing continued to contract in April viz the weak 48.3 outturn in the HSBC/markit PMI. It was not even the news that March industrial production, housing activity and money supply were all much weaker than expected. It was the GDP data, which by contrast did not attract much attention, mainly because headline real GDP growth came in a touch better than expected at 7.4% yoy (see chart below).

For me, the real big data event out of China was the news that China’s nominal GDP growth slumped from 9.7% yoy in Q4 to 7.9% yoy (see chart above). That is the weakest nominal growth since the 2008 Great Recession. Very few people tend to focus on these nominal data and what they imply for economy-wide inflation. Our very own Wei Yao is an exception and highlights that the GDP deflator dropped by 1.4ppt to 0.4% yoy (see front cover chart). While markets may debate (and then dismiss) the deflation risk in the US and eurozone, let us make sure we do not miss the fact that China is sliding inexorably towards outright deflation.

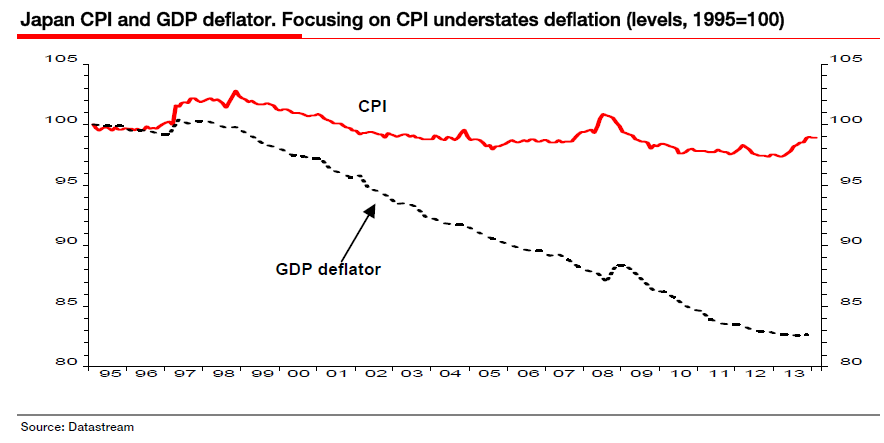

The continued advance in the Chinese CPI above the 2% level (it rose to 2.4% in March) may be giving investors an overly reassuring impression of underlying deflationary pressures in the Chinese economy overall. The situation in the company sector is dire, with producer prices in March dropping for the 25th successive month (see chart above). Typically when producer prices are this weak, the CPI would also be declining marginally. That sort of outturn would have the markets in a real flap, with global bond yields significantly lower than they are now. Looking at the overall economy-wide inflation/deflation situation gives us a far better indication of how intense the pressures are. The GDP deflator includes a wider basket than just consumer goods and services, and includes investment goods, housing and exports. Indeed, focusing on the CPI in Japan, rather than the GDP deflator, would have underestimated the deflationary hurricane that was raging in Japan destroying solvency for the highly indebted corporate sector (see chart below). Let us not make that mistake for China.

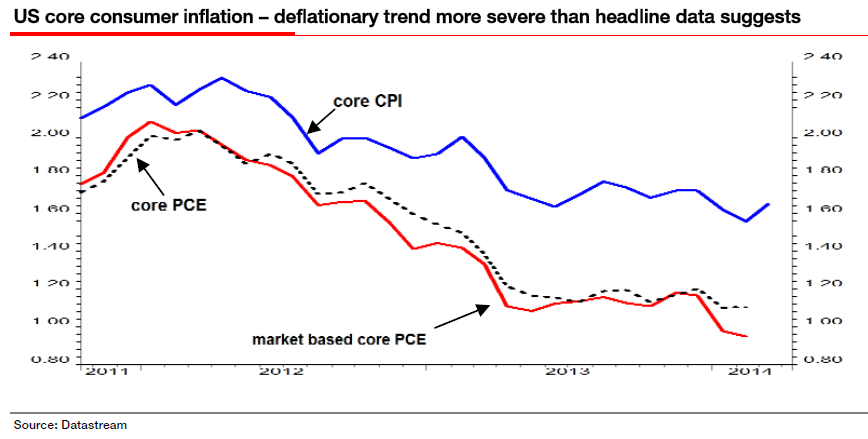

While most recognise that the eurozone is already at the edge of the deflationary precipice, few recognise just how close the US also is. The core consumer price data the market focuses on (CPI and the personal consumption expenditure (PCE) deflator, excluding food and energy) both remained stable last month (see chart below). But our preferred measure for core PCE (which excludes numbers the statisticians have to make up) continued to slide (red line below). US core consumer inflation – deflationary trend more severe than headline data suggests

If the US is so much closer to outright deflation than most realise, that might explain why the US Treasury has turned very aggressive again on Chinas renminbi policy. The FT report that The US Treasury slammed China for resuming large-scale efforts to hold down the renminbi just hours after official data showed the country has amassed nearly $4trn in foreign exchange reserves . Renewed focus on China was the main feature of the Treasurys semi annual currency report. We have long banged the drum that deflationary developments in China would force renminbi devaluation and trigger outright deflation in the West.

But if you dont believe me, listen to an oracle on the subject. Russell Napier in his latest note wrote, “Mercantilist alchemy transmutes China’s external surpluses into foreign exchange reserves and renminbi. But with capital outflows from China at record highs, those surpluses are only maintained due to its citizens’ foreign-currency borrowing. Bank-reserve and M2 growth are already near historical lows and are driving tighter monetary policy. This will lead to severe credit-quality issues and force the authorities to accept a credit crunch or opt for a major devaluation of the renminbi. They will do the latter; and despite five years of QE, the world will get deflation anyway.”

One does not need to be an uber-bear for this analysis to be useful. I take Edward’s thesis as framework rather than literal forecast; deflation is the big battle front and acknowledging such is no more than embracing PIMCO’s notion of the new normal in which debt is reviled, asset prices slow to rise and unsustainable when they do and investment returns are generally lower than the preceding period. This keep me focused on the basic principle of investment in such an era, that return of capital is every bit as important as return on capital and, hence, when opportunity rolls around, the money is still there, ready to pounce…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.