SQM Research released its weekly email newsletter which contained some interesting analysis on Australian house prices, as well as the level of overvaluation across the Australian housing market.

On house prices, SQM does not believe the hype of yesterday’s RP Data house price release for March, which recorded the highest monthly price growth in the series’ 18 year history (+2.3%), 3.5% growth over the quarter:

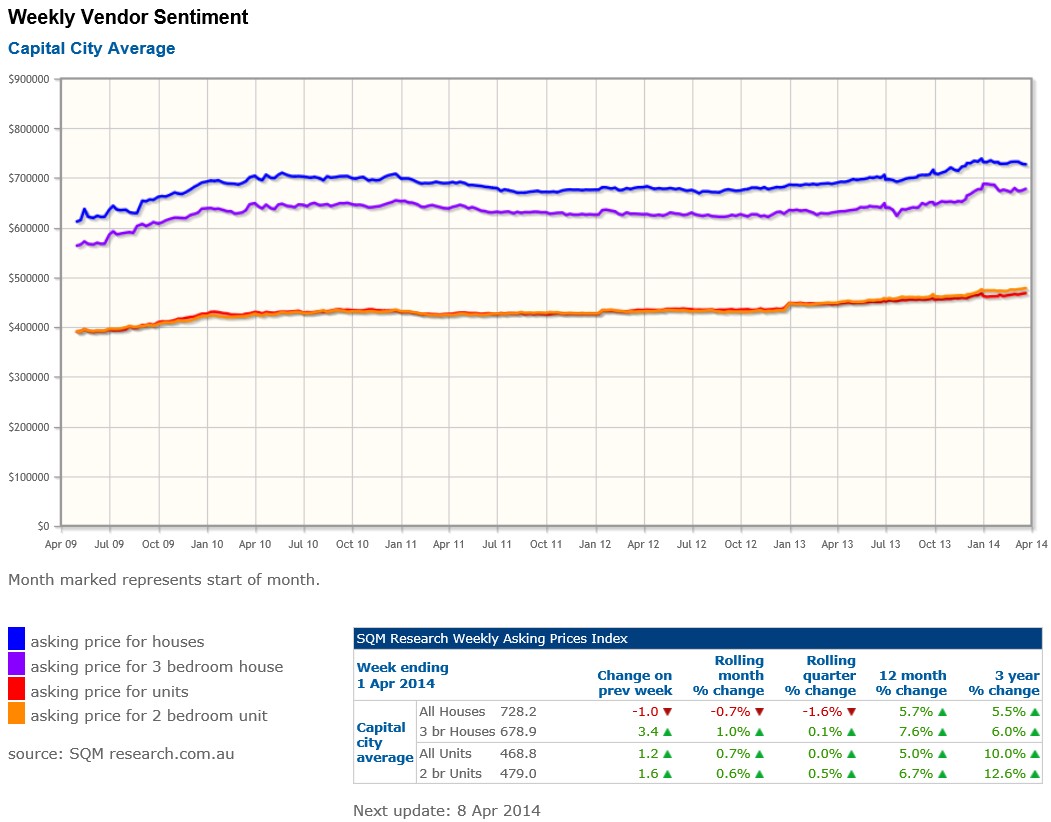

SQM’s asking prices were updated today covering the last week of vendor activity and this now completes the first quarter of the new year. The index for the quarter recorded asking prices for houses falling 1.6% for the capital city average, while unit asking prices were flat for the quarter.

So it was a weak result for the quarter with vendors struggling to lift their asking prices. Surprisingly, weakness was recorded in Sydney with asking prices for houses falling by 1.6% for the quarter. Units rose by just 0.2%.

Adelaide recorded the strongest result for the quarter, with asking prices for houses rising by 0.9% and units rising by 3.5%.

This is all in contrast to the very bullish findings from the RP Data daily dodgy index, which among other things, reported a very sharp rise in Melbourne dwelling prices of 5% in the Quarter and now has Sydney up over 15% for the year. While that index may be meeting our forecasts this year of 15-20% rises for Sydney I am still very dubious of it and I strongly recommend for you to follow the ABS and APM versions of house price sold data, which will be reporting early next month based on a lot more sold data for the quarter gone by.

SQM then turns to the issue of market valuations, and attempts to ascertain the extent of market overvaluation. According to SQM, Australian housing is only mildly overvalued, with median prices only slightly outpacing nominal GDP since 1986:

The big rises reported out of this index this week had Mr Chris Joye – a columnist for the Australian Financial Review, declaring there was a heightened risk of up to a 20% decline in dwelling prices across the national housing market because presumably, the market was massively overvalued and entering into a “bubble”.

One of SQM’s preferred measures of valuation are house prices to nominal GDP. We have for a long time given this method of valuation some precedence simply because we are believers that one can’t have a situation where house prices indefinitely rise faster than income growth.

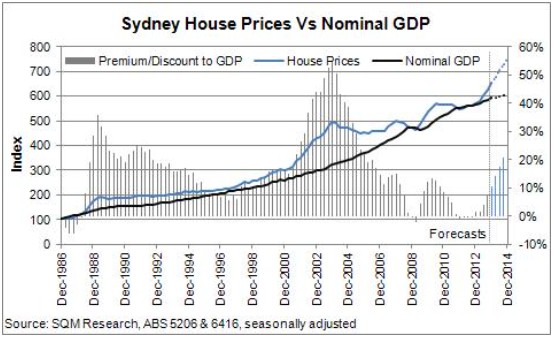

Based on this measurement the evidence is clear. Sydney itself is going into overvalued territory.

We estimate that as at the end of December, the market was about 11% over valued. And if our forecast comes into reality the market will be about 24% over valued. In context, the market would be above its longer term average price to nominal GDP premium but nowhere near the point in 2003, when it was dangerously overvalued – where at one stage it was 55% over nominal GDP.

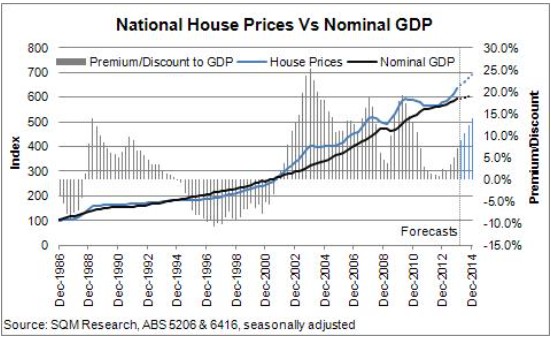

Now, let’s now consider the overall market based on the weighted average of the 8 capital cities. In this chart the market is currently recording a modest overvaluation running at the long term average since 1986.

If we actually stripped out Sydney, the market would now be trading at a discount to nominal GDP. Hence my comments made in the Financial Review over the weekend.

Taking into account our forecast of 7-11% for national dwelling price growth in 2014, the premium would then increase to about 14% at the end of this year. That would take it above the long term average premium to incomes once again, but nowhere near the dangerous levels recorded in 2003 and still below the peak recorded in 2007 and 2010.

The reason why the market is not as massively overvalued as what Chris Joye would have you believe becomes all too apparent in the chart. For an extended period in the last four years, the market underperformed compared to nominal GDP. Indeed it went through a correction between 2010 to 2012. Something which we forecast was going to happen. That allowed income levels to catch up and reduce the premium in the market.

So no, the market is not massively overvalued. Eventually, when we get to the market peak we might be well into overvalued territory. Presuming that rates do rise early next year as what the money markets are forecasting, then I suspect that would slow the market down during 2015, thereby creating a soft landing for the housing market.

One thing in all this is we do know the market is sensitive to interest rates, so SQM Research does expect a reaction when rates go up again. But it is very unlikely in our opinion, that one would get an across the board, large scale 20% fall in the market.

For that to happen, we think the RBA would have to lift rates aggressively going into 2015 by at least 200 basis points in a very short space of time and/or unemployment dramatically rises above 7.5%. And at this time, those scenarios seem very unlikely.

Let me be clear, I disagree strongly with SQM’s choice of valuation metric, which has simply compared the growth of median house prices (as measured by the ABS) against the total growth of the economy (as measured by nominal GDP). This is the wrong approach as nominal GDP includes the impact of population growth, which has risen strongly over the period.

A more consistent methodology would be to compare either:

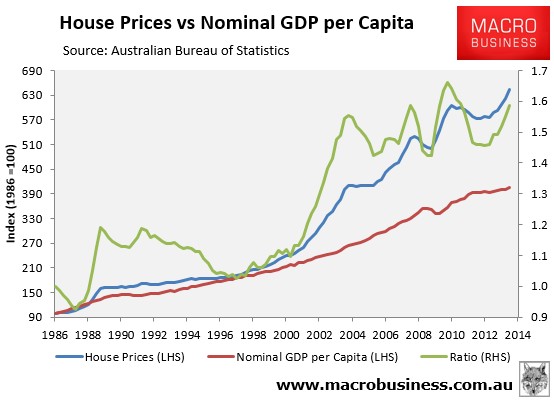

Median house prices against nominal GDP per capita; or

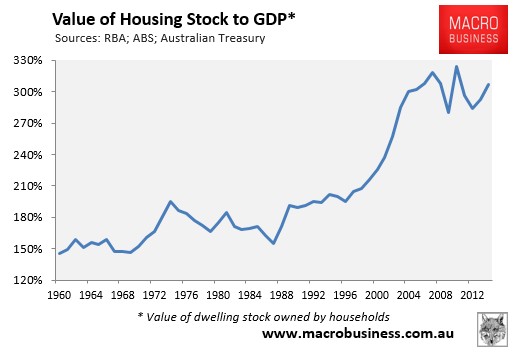

The total value of dwellings against nominal GDP.

And the results under both methods are not pretty.

First, consider the below chart plotting median house prices against nominal GDP per capita:

According to this metric, Australian housing is severely overvalued, with valuations also above the levels of a decade ago.

It’s a similar story when total dwelling assets are measured against nominal GDP, with values again hovering near all-time highs:

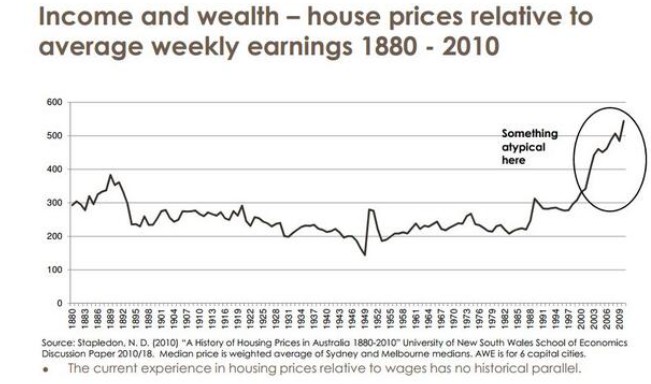

And for an alternative super long-term view, check-out the below chart posted on Twitter yesterday by Matt Cowgill (via Matthew Butlin):

While obviously today’s record low mortgage rates improve the ability of households to service their mega mortgages, based on GDP and incomes alone, it is incorrect to assert than Australian housing is only mildly overvalued.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.