MB members special report: How and when will this business cycle end?

The melange that is contemporary ideology finds no better expression than in the world’s two largest national economies. In communist China an opaque clique of Schumpeterian capitalists has declared that its economy will undergo a final transformation to free markets. Across the Pacific rim in the uber-capitalist United States, the Federal Reserve has ascended to Keynesian triumph as markets twist themselves around every utterance of the central bank, in the process abandoning their value-determining role.

This juxtaposition is intellectually fascinating but for investors it is also the key to understanding our current business cycle, as well as when and where it is likely to end. Needless to say, that insight is worth money, probably a lot of it.

Let us define our terms. Joseph Schumpeter is a doyen of the Austrian school of economics and most famous for defining the notion of “creative destruction”. Purists will be horrified to learn that the term actually derives from Karl Marx but Schumpeter adapted it to, in his mind, the capitalist engine of growth as innovation and productivity drive new capital to supplant old. Monopolies are toppled, efficiencies ruthlessly achieved, dead-wood removed and wealth expanded. Creative destruction is, above all, a business cycle theory of economic development. Take the pain and you will prosper!

That brings us to Keynes, the doyen of his own school. It was Keynes who most usefully observed that there is only so much pain the people or the polity can take. Sometimes, if left to their own devices, markets will destroy themselves by over-liquidating investment and consumption. It was Keynes who most popularised the notion that government should step in and stabilise the creative destruction of the business cycle from time to time, lest it devour the aggregate demand that underpinned it.

What is often forgotten is that Keynes too was a classic liberal and believed that even as government stepped in from time-to-time, it should do so while preserving the moral underpinnings of capitalist individualism.

These two theorists of the twentieth century business cycle tower above all others but in some ways that is times past. The economies of yesterday were more “real” than they are today. The dominant evolution in the twenty first century global economy has been in finance. Today more capital, debt and derivatives of both circumnavigate the globe on a second by second basis than at any time in recorded history. The finance cycle – cross-border accumulations of debt and equity and their role and creating and mitigating national imbalances – is now central to the fates of all economies.

One more titan of business cycle analysis is needed for our framework then. His name is Hyman Minsky. Minksy is sometimes referred to a post-Keynsian analyst because it was he that described how the stabilisation of economies, in part resulting from the embrace of Keynsianism, creates its own financial instability. That is, when a government supports a business cycle through Keynesian counter-cyclical spending it also injects moral hazard into the economy. The greater stability leads to greater and more reckless borrowing, leading in turn to financial crisis…and the end of the business cycle!

Three titans, four economies

So, what would our three titans make of the global business cycle today? Let’s break it down to the world’s four major economic regions.

In Japan, Schumpeter would find vindication. Its long stagnation has arisen from a fusion of Keynsian economics with oriental values. Following its great late eighties asset bust, Japan’s monolithic culture has refused to address declining demographics via immigration and a fierce egalitarian culture has protected “salarymen” at the expense of entrepreneurs. Completing the stagnation, Japan has spent the better part of 25 years holding back creative destruction through public spending and notorious “bridges to nowhere”:

Keynes too would find vindication but also disgust. He’d see an economy that has managed through one of the great asset busts of the twentieth century without a debilitating rise in unemployment. But he’d also see an economy in need of a sizeable shock from live individualist electrodes.

Minsky, likewise, may not be overly perturbed. Japan’s public debt may be awesome in scope but it owes it to itself so the likelihood of markets turning to discipline is low. Japan issues its own currency and is a global reserve, two factors that make it difficult for markets to assault either its currency or bonds. The final proof of which came over the past year in which Abenomics has been able to comprehensively debase the value of the currency without precipitating crisis. While stagnation will roll on, collapse is unlikely. They don’t call shorting Japan the “widow-maker” trade for nothing.

Next up is Europe, where Schumpeter would be pleased. The European project may be only half-born but monetary and fiscal policy has been kept tighter than elsewhere to allow creative destruction to run its course. The resulting rise in competitiveness in the region’s periphery is beginning to suck in capital and growth has returned on the basis of rising exports and external balances are all looking much more healthy.

Keynes, on the other hand, would see Europe as a failure. For him, the internal deflation that corrected external imbalances has been brought about by a calamity in peripheral labour markets where unemployment has been as high as 27.5%. He would at least be pleased that growth has also returned, in part, because severe austerity has been recognised as self-defeating and government spending is allowing the private sector adjustment to transpire more humanely.

Minsky would worry that private sector deleveraging rolls on and that the leverage in the banking system remains extreme.

Combining the three perspectives yields a cycle that is as unfinished as it is malformed, but it can probably continue without crisis so long as an external shock does not disrupt its export growth. Europe is no longer a cycle-ending concern.

This brings us to the two economies that are most at risk of ending the global cycle: the United States and China. These two economies took their Keynesian responses to the last global recession far farther than others. In the process they both built up worrying financial and economic imbalances that could unwind and pull down much of the globe with them.

The US took the precise opposite course to that of Europe and Schumpeter would be more displeased with the US than any other major economy. Although its recession was deep, it wasted huge resources on propping up inefficient “too-big-to-fail” firms in both the financial and industrial economy. Moreover, its Federal Reserve has shown total disregard for the value of money, the defence of which is a central tenet of Austrian economics.

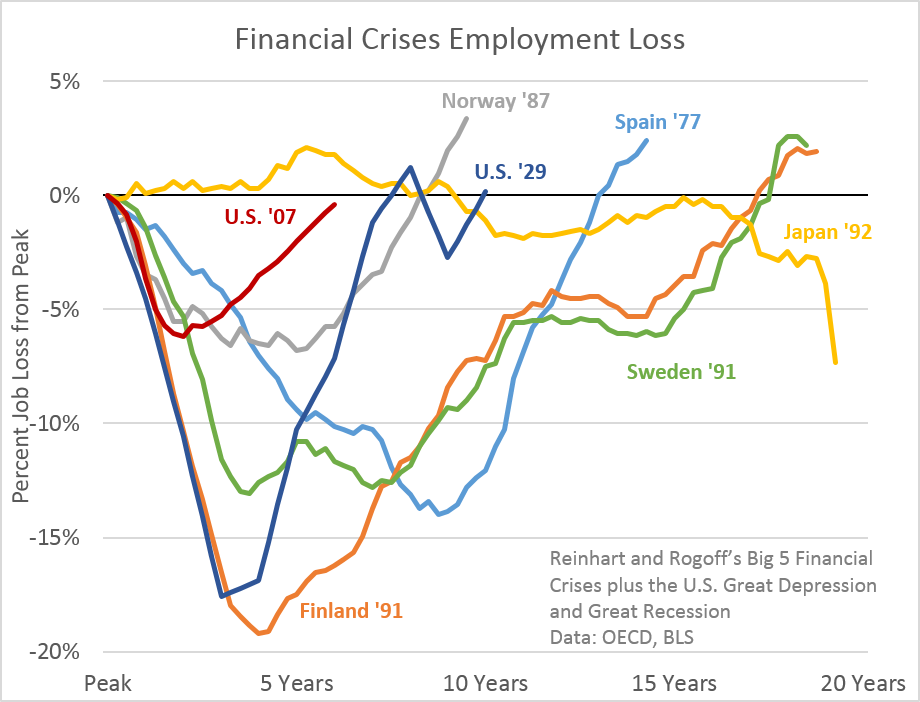

He would find an unlikely ally for his disappointment in Keynes. The recovery of its post-crisis labour market has been swift by comparison with other nations:

But it has largely been achieved not through counter-cyclical fiscal spending, for which there are tremendous productivity-enhancing opportunities given the nation’s fading infrastructure, but through re-leveraging and the re-inflation of a series of bubbles.

Minsky would look on with a wry “I told you so” grin as he surveyed the NASDAQ mini-bubble, a broader stock market bubble built upon corporate capital management not economic growth, a housing market echo-bubble built upon a Wall Street revival and bond markets that having given up pricing anything other than free money from the Federal Reserve.

All three would see the distinct possibility that any and all of these market distortions could unwind as Federal Reserve uber-stimulus is withdrawn. That has already begun, in fact, in the high-beta end of the stock market.

But for all of these challenges, it is in China that all three business cycle analysts would find the greatest risks. China’s post-great recession Keynsian binge was beyond anything, anyone could have imagined in advance. It issued more credit, built more stuff, leveraged more balance sheets and pushed its primary imbalance – too much investment driven by debt at the price of lower household incomes and consumption – much further than most even thought was possible.

Schumpeter would have looked on with great displeasure through much of this period but would be much more pleased with what he sees now. China now seems determined to inflict creative destruction upon its economy. It has reined in corruption and centralised power around the Schumpeterian reformers, and is spending that political capital on slowing its public spending on un-economic infrastructure projects, as well as keeping monetary policy relatively tight to squeeze mal-investments in its industrial and property economies.

The pattern of policy is clear for the period ahead. Keep pressure on marginal borrowers but don’t wind-in public spending too fast to hit growth. One foot on the monetary break and other on the fiscal accelerator may not be entirely to Schumpeter’s taste, but he’d certainly approve of the goal.

Keynes, too, would look on with some approval. He would have approved of the huge post-recession fiscal push but would now also approve of the push to revitalise the reform process towards a greater role for private enterprise.

But Minsky would look on with deep trepidation. It is he that would most keenly recognise that the kind of reform process that China has undertaken is rarely achieved without major financial and economic disruption. He would recognise that his description of the financial cycle is mature in China:

Hedge financing units are those which can fulfill all of their contractual payment obligations by their cash flows … speculative finance units are units that can meet their payment commitments on ‘income account’ on their liabilities, even as they cannot repay the principal out of income cash flows. Such units need to ‘roll over’ their liabilities or issue new debt to meet commitments on maturing debt.

…Ponzi finance units are those whose cash flows from operations are not sufficient to fill either the repayment of principal or the interest on outstanding debts by their cash flows from operations. Such units can sell assets or borrow. Borrowing to pay interest or selling assets to pay interest (and even dividends) on common stocks lowers the equity of a unit, even as it increases liabilities and the prior commitment of future incomes.

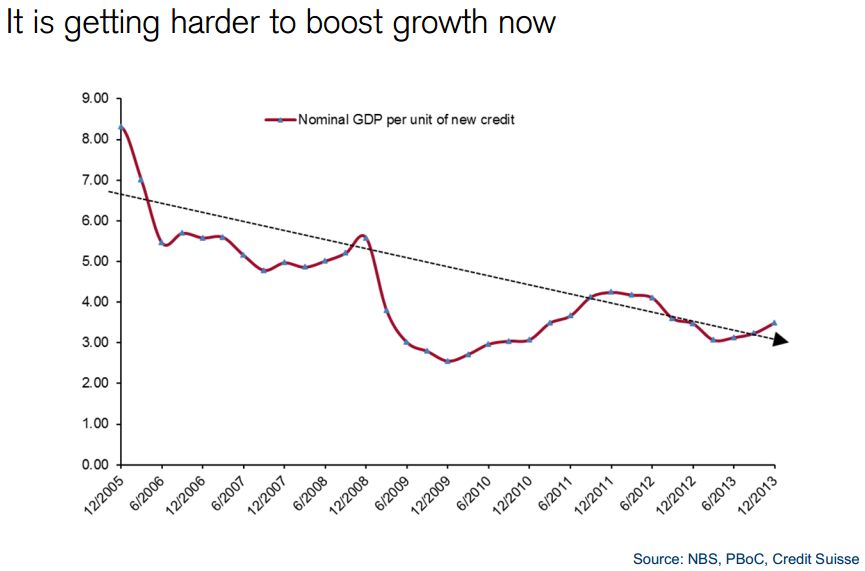

Chinese reform is a wrestle with Minsky’s Ponzi financing units. Such is apparent in the slipping of its relationship between credit creation and growth:

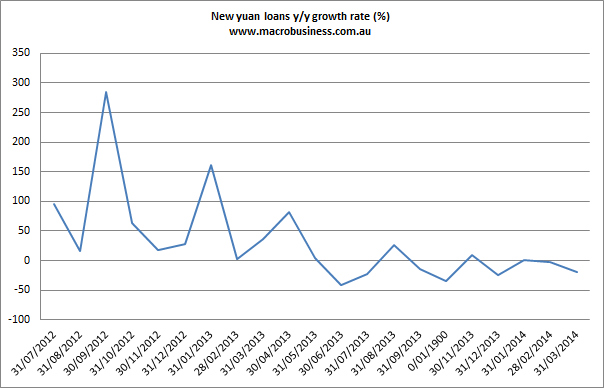

It is in evidence in the flourishing (and now crimping) of its shadow banking sector, which although not as complex as its dark Western cousin, is still wild cat finance. New yuan loans year on year have turned negative:

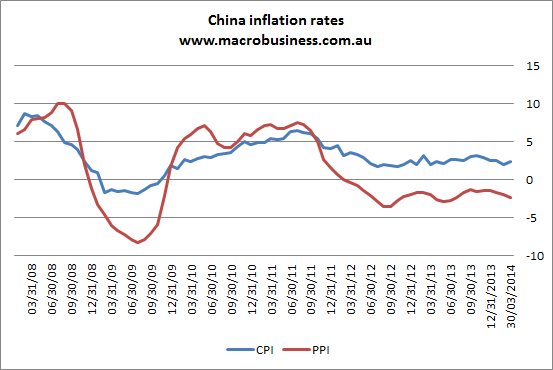

It is also apparent in the persistent deflation that has taken hold of its industrial economy where endemic over-capacity has seen producer prices falling at 2% and more per annum since the end of 2011.

It is evident as well in growing anecdotal evidence that has established crony-like relationships between highly leveraged sectors like steel, ship-building and property development in which vendor financing from steel mills to marginal borrowers is common and property developers have begun buying banks to ensure the flow of their Ponzi finance is not interrupted by the reform program.

And it is surely in evidence most clearly in the drive by a communist party towards free market reform, given the risks, because the current growth model is recognised as an even greater danger to its power if it were to grow larger before collapse.

Minsky would say that China has reached a moment when Ponzi finance is unable to continue its balance sheet stretch and will now default, which is what we are beginning to see.

The danger, then, is that at some point in its reform process, China pushes a large enough Ponzi borrower to default that it rocks confidence in its shadow banking system (and possibly conventional banks as well). In such an event China could enter an accelerated reform process as lenders pull loans to many marginal businesses all at once. As it were, a credit crunch.

China’s federal public debt is very low at just 20% of GDP and there is little doubt that it has the fire-power to step in with bailouts and guarantees to stabilise the system in such an event but, even so, that takes time, and it would almost certainly involve a sufficiently hard Chinese landing to disrupt global markets and describe an end to the global growth cycle.

The lines of contagion from China into the global economy are obvious enough. Commodity prices would crash, taking down much of the growth in emerging markets with it because a lot of their growth is reliant upon high commodity prices. That, in turn, would cause a major flight of capital from both China and its emerging markets satellites (Brazil, Chile, South Africa, Russia, India etc). This would make all of the problems worse as currencies collapsed and interest rates had to be raised at the worst possible moment. We’ve already had a taste of this dynamic in the mini-emerging markets crisis that accompanied the “taper tantrum” of 2013.

In developed markets, there may also be financial contagion from a Chinese banking freeze. Western banks would likely be OK but there is research suggesting that a lot of equity capital has been deployed in Chinese and emerging market corporate debt. Defaults on this would hit Western fund managers hard with unknown consequences.

However, the major transmission mechanism is likely to be growth. Europe would be hit hard by falling Chinese and emerging market imports of its goods. The US would be better off but its equity bubble would bust as it discounted big hits to overseas profits and sharp falls in global growth, exacerbated by a rise in its currency owing to the flip side of emerging markets capital flight. Japan would be similar.

The sum total for the world would not be as bad as 2008 but it would still end the global business cycle.

Australian implications

As often happens, Australian trends follow those of our hegemons. We have ourselves just elected a Schumpeterarian government. We are embarked upon the end of the age of entitlement with fiscal austerity and creative destruction the touchstones of our new parliamentarians.

But the Australian economy uniquely straddles the emerging and developed worlds. On one hand, we live off the income generated by commodity exports to China. On the other, we leverage up those gains using the magic of US-style financial capitalism. In the event that a Chinese credit event ends the business cycle, the first is going to tumble and the second is going to get more expensive.

Given Australia is already struggling to find growth in its post-mining boom adjustment, a major Chinese and global shock would be much more difficult for the economy than the global financial crisis.

With gross debt at around 22% of GDP, the federal budget is still in good enough shape for a substantial counter-cyclical spending package, but not a repeat of the huge 2009 Rudd stimulus program. A package perhaps half that size would be possible and almost certainly forthcoming irrespective of who is in power.

Interest rates also have less fire-power. With the cash rate already at 2.5%, the RBA could perhaps cut another 1% before it was forced to stop lest it risk capital flight. Australia still runs a substantial current account deficit that must be funded by an interest rate spread to the rest of the world.

This is far lower relative borrower relief than that delivered in the GFC when interest rates fell 4.25% and given the likelihood that the banks’ cost of funds would already be rising materially, not all of the cuts will get passed on.

With house prices already elevated, there is unlikely to be much follow-through there, either, and there is a real risk of a house price bust as consumers and investors simultaneously bunker.

Hence, although a Chinese hard landing would be easier for the world to digest than the GFC, it would generate and an external shock for Australia that was more difficult to weather through the boosting of internal demand. It is also highly likely that said shock would spell the beginning of a new phase of slower (but more sustainable) Chinese growth. So, for Australia, it would not be a one-off event so much as it was a permanent reset, as commodity prices never recovered their former highs (but remained elevated relative to history).

That raises the difficult possibility that it could trigger a lasting structural adjustment in Australia as the Federal budget refused to recover post-stimulus and is ultimately stripped of its AAA rating. All credit rating agencies have made it plain that the major banks enjoy a two-notch upgrade owing to their explicit and implicit public support. Any downgrade to the budget will flow directly through to higher funding costs for the banks and so any hope a swift housing rebound may also run into ongoing headwinds.

Authorities would have to rely more on the currency and a revival in Australia’s non-mining tradable sectors for growth. The shift in the gas boom to the production phase would help considerably but more will be needed, much more.

After many successful years of living the Keynesian dream, Schumpeter would arrive for a long and difficult stay Downunder.

Timing

So much for theory. Business cycles are never so simple. They run as much on animal spirits as they do structures and identifying tipping points as well as policy actions in advance is impossible. All one can do is to map out the risks and imbalances and take an educated guess! Most global business cycles last about eight years and this one is into its sixth.

The current NASDAQ mini-bust is a warning sign in the US that rising interest rate will be painful for equity. But that is OK given the US Federal Reserve has a habit of reversing course when markets get upset enough. The NASDAQ bust is unlikely to spread too far beyond a more general stock market correction, though one can never discount the possibility of an unexpected leveraged player going under and spreading panic through US finance once more, much like Long Term Capital Management in 1998 or Lehmnan Brothers in 2008.

My guess is that it will be China that will end the cycle and on that front we’re currently somewhere around the equivalent of early 2007. Chinese growth will likely decelerate over the next two years and the defaults will mount. At some point one will be large enough that the dynamics described above will take hold.

Or not, of course! Chinese authorities could pull off the highly improbable. But in that event, success will still mark a very different looking Chinese economy, with much lower investment and much higher consumption, virtually ending growth in commodity demand from China.

Whether you reckon on crisis or not, the matrix of risks and imbalances for the Australian business cycle points to one investment outcome above all others. The Australian dollar is going to fall a long way once its current little flush passes. That’s something upon which all three of our titanic business cycle analysts would agree.