The AFR has published a detailed report today summarising the arguments for quarantining negative gearing. The article cites a number of commentators, including Saul Eslake and the Grattan Institute’s John Daley, who essentially argue that winding back negative gearing would:

- Save the Budget money: around $4 billion per annum initially and $2 billion over the longer-term; and

- Improve housing affordability, by removing speculative demand from the housing market, increasing home ownership in the process.

It’s all fairly stock standard stuff, and nothing that hasn’t been read on MacroBusiness a number of times before (for example here, here and here).

One vocal dissenting voice on abolishing negative gearing is the Housing Industry Association (HIA), which over the years has gone to great lengths to defend the tax lurk (see here and here).

Today’s AFR article is no exception, with the HIA’s chief economist, Harley Dale, making the following statement:

Housing Industry Australia chief executive Harley Dale warned tinkering with the system would have a “massive negative impact on investor sentiment”. He said rental supply wouldn’t increase if investors were not confident. If the government really wanted to increase housing supply it should look to the Henry Review recommendations which suggest other changes such as cuts to inefficient state taxes like stamp duty, ahead of negative gearing, Mr Dale said.

While it is true that winding back negative gearing would have a “massive negative impact on investor sentiment”, why would this be such a bad thing?

Removing some speculative demand from the housing market would take the pressure off house prices, improve housing affordability, and increasing the rate of home ownership by allowing more first home buyers to enter the market.

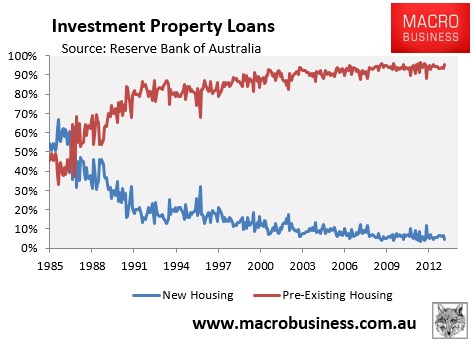

As for Dale’s claim about rental supply, Reserve Bank of Australia (RBA) data clearly shows that the overwhelming majority of investors – almost 95% – buy pre-existing dwellings, not newly built dwellings, and that the proportion of investors buying new dwellings has fallen spectacularly since negative gearing was re-introduced in September 1987 (see next chart).

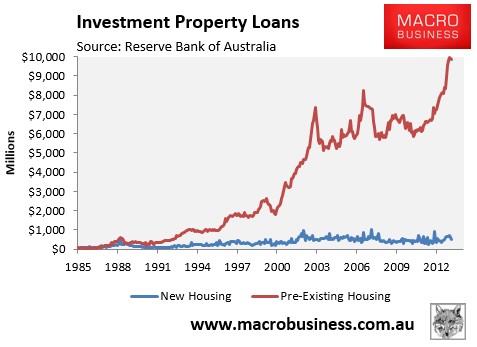

Moreover, the amount of investor funds going into new housing has barely shifted in 25 years, whereas investment in pre-existing dwellings has skyrocketed:

Since investors primarily purchase pre-existing dwellings, negative gearing in its current form simply substitutes homes for sale into homes for let. Accordingly, the policy has done little to boost the overall supply of housing or improve rental supply or rental affordability.

In the event that negative gearing was wound-back and a proportion of investment properties were sold, who does Dale think they would be sold to? That’s right, renters (or other investors that would rent them out). In turn, those renters would be turned into owner-occupiers, reducing the demand for rental properties and leaving the rental supply-demand balance unchanged.

Indeed, Saul Eslake makes similar claims in The AFR article:

“One of the arguments from the defenders of negative gearing is that it increases the supply of rental housing by attracting investment into the property market” said Mr Eslake, now chief economist of Bank of America Merrill Lynch. “That’s a very poor argument because over 90 per cent is used to buy existing dwellings. Moreover, most countries that don’t have negative gearing, have higher vacancy rates.”

Previously, the HIA has also claimed that negative gearing “keeps a lid on rents”, suggesting that its removal would force rental costs up. Again, this is a spurious claim in light of the above data.

And to illustrate why, the below chart plots the Australian Bureau of Statistics (ABS) rental series from 1972, with the period where negative gearing losses were last quarantined (i.e between June 1985 and September 1987) shown in red. As you can see, there was nothing spectacular about this period, with much higher rental growth recorded in earlier periods when negative gearing was in place:

Similarly, if we deflate the above series by CPI, in order to remove the effects of inflation, we again see that rental growth over the period when negative gearing was last quarantined was nothing special, with periods of higher rental growth recorded both prior to and subsequently:

Finally, Dale’s suggestion that the Government should instead abolish stamp duty is meaningless unless he can identify an alternative source of taxation revenue for the states. My pick would be replacing stamp duties with a broad-based land tax, but would the HIA support such a move?

As noted last week, negative gearing is costing the government billions in lost tax revenue, but is doing absolutely nothing to boost supply. It also creates additional demand from tax subsidised investors, placing upward pressure on home prices and locking-out would-be first time buyers.

There is little policy rationale in favour of keeping negative gearing in its current form, whose foregone funds could instead be used to fund schools, hospitals, housing-related infrastructure, or any number of other worthwhile endeavours.

The Government would do well to ignore the screams from vested interests, like the HIA, which seems more concerned about protecting the value of its member’s land banks, rather than actually boosting supply.

unconventionaleconomist@hotmail.com