Over the years, we have heard a range of questionable arguments on why negative gearing should be retained, despite its huge cost to the Budget and the upward pressure it places on house prices.

Today, Professor Bob Officer has joined the phalanx of defenders around negative gearing arguing in the AFR that removing it would be a mistake:

House prices attract everyone’s attention… Among those in the too-high camp have been proponents of removing “negative gearing”, as at least a partial solution to their perception of a problem of a resource misallocation with adverse wealth distribution effects. It would be a big mistake, theoretically and practically, to target property with such an action…

One of the basic principles of optimal resource allocation in an economy is to treat all asset classes the same way when applying a tax…

All asset classes, again as a generality, can be negatively geared; there is no good reason to single out housing for special treatment, and to do so will result in a misallocation of resources.

Let’s be clear. Few proponents for abolishing negative gearing – whether it be Saul Eslake or me – believe that only property should be targeted. Rather, most of us believe that negative gearing should be “quarantined” for all forms of investment, be it property or shares, so that income losses (e.g. the shortfall in rent or dividends over interest repayments) can only be carried forward and offset against future income gains (e.g. when rent or dividends exceeds interest payments), rather than deducted against current unrelated wage or salary income.

“Abolishing” negative gearing equally for all investment classes removes the likelihood for distortions, and overcomes Officer’s concerns that removing negative gearing would “result in a mis-allocation of resources”.

Back to Officer:

The only time that rule should be modified is if an asset class delivers a cost or benefit to the community that is not borne/received by the owner of the asset…

What is the social cost associated with home ownership or investment in housing? As a generality there is none…

Forcing-up the cost of housing by encouraging increased investor speculation has deleterious distributional impacts for younger and lower income Australians, who are forced to either dedicate a higher proportion of their lifetime’s earnings to achieve home ownership, or are forced to remain in the rental system. Given that Australia’s retirement system explicitly favours home owners over renters, such a situation also has deleterious implications for security in retirement for those locked into rental accommodation.

Back to Officer:

Removal of negative gearing effectively double-taxes debt capital since the interest is taxed in both the hands of the borrower and the lender…

To remove negative gearing on property that would result in a double tax on interest on debt is going backwards.

The most glaring anomaly in Australia’s tax system is the way that different forms of saving are treated. Someone that invests $25,000 into a term deposit is taxed at their full marginal rate, whereas if that same person buys a negatively geared property, they receive full tax breaks on their rental losses, and then pay a reduced rate of capital gains tax when the property is eventually sold.

Such anomalies have created over-investment in housing and created a dearth of savings – one of the reasons why Australia’s banks have such a high reliance on offshore borrowings. Indeed, the Henry Tax Review recognised these anomalies and recommended to lower taxes on deposits while reducing tax breaks on negatively geared investments by 60%.

Back to Officer:

It is sometimes asserted that negative gearing does nothing to increase the supply of housing because most investment property is for established dwellings.

What causes negative gearing to suspend the laws of supply and demand? To the extent that negative gearing increases the demand by investors for housing, causing house prices to rise, resources will be attracted into housing, thus increasing the supply of housing.

There are studies suggesting that our relatively high house prices are a supply issue… But this has nothing to do with negative gearing. It is a separate set of issues.

Again, Officer has used fuzzy logic. On the one hand, he argues that the higher prices caused by negative gearing stimulates supply. Then straight after, he argues that supply is unable to respond due to regulatory barriers, but that this is an entirely separate issue from the excess demand caused by negative gearing!

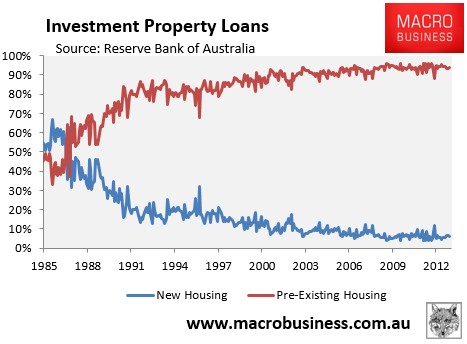

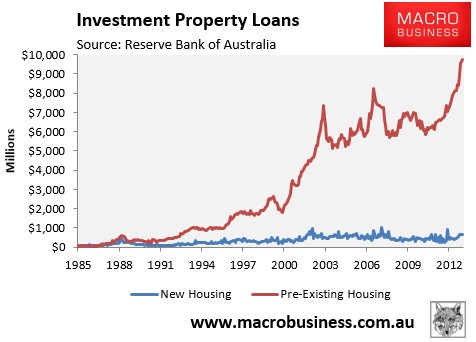

If he was to objectively examine the data, he would soon see that around 19 out of every 20 loans for investment properties are for pre-existing homes. As such, negative gearing is overwhelmingly turning homes for sale into homes for let and not improving the supply situation one iota (see below charts).

While I clearly agree with the need to liberalise land/housing supply, and believe that it is the more important issue for housing affordability, the fact remains that negative gearing has even less justification under Australia’s current urban planning system. As long as supply is strangled, the additional demand from tax subsidised investors will place even greater upward pressure on home prices and continue locking-out would-be first time buyers.

The billions of dollars of foregone funds used to subsidize property investors could also instead be used to fund schools, hospitals, housing-related infrastructure, or any number of other worthwhile endeavours, providing far greater benefits to society at large.