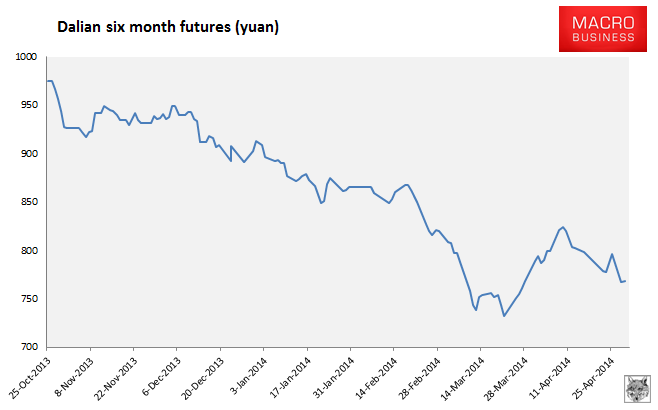

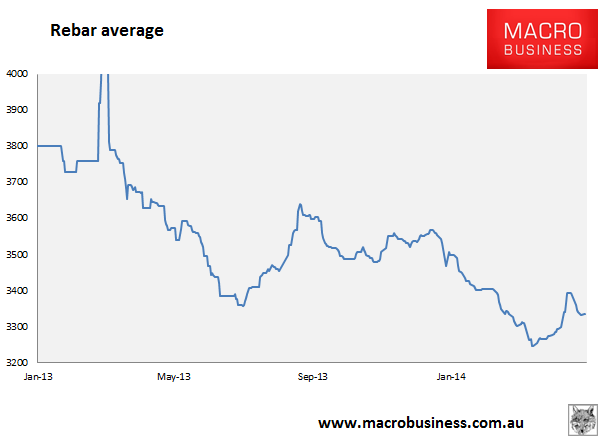

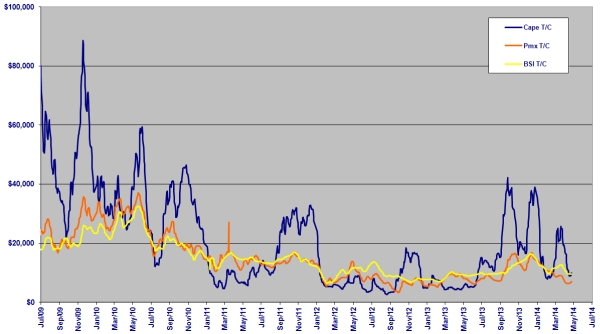

Here are the iron ore charts for April 29, 2014:

Paper markets managed weak bounces only with rebar futures joining in. Physical is going nowhere fast either with the Baltic Dry capesize index falling 3.5% and now languishing at levels associated with weak demand and even destocking:

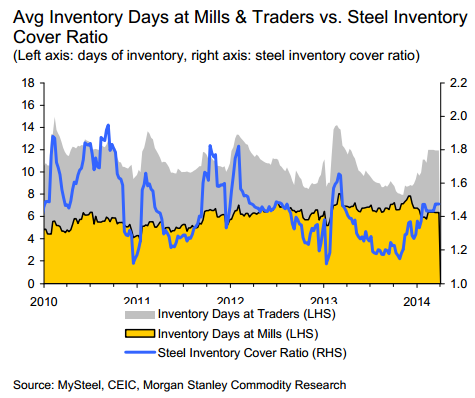

I’ll be a little surprised if we get another round of destocking yet given we’re well into peak steel season. Mill ore inventories are below their long term average, according to Morgan Stanley:

But, days of cover is also falling because of the supply glut and associated lack of need to store material so we may roughly be at parity in this new normal. The huge port pile complicates this too.

The steel coverage shows the same pattern.

In sum, then, Chinese ore and steel stocks are high enough to destock but not excessive given recent production jumps so my base case remains no destock until Q3 but then look out.

That has bearing on a story from The Australian today:

Fresh from an all-embracing tour of China, institutional funds manager JCP Investment Partners has told its clients that it now expects iron ore to transition to its “long run’’ expectation of less than $US80 a tonne “more quickly than we had previously forecast’’.

JCP said that while it expected iron ore prices this year would remain relatively robust at more than $US100 a tonne, next year would be a different story. “Flat to declining Chinese steel demand means the wave of Australian and Brazilian supply hitting the market in 2015 will push prices down to $US80 a tonne,’’ itsaid. “This change has lowered our valuations of Rio Tinto, BHP Billiton and Fortescue … which has resulted in our portfolio exposure being reduced slightly for these companies.

“A consistent message from steelmakers was that pellet and high iron (content) premiums will increase, while at the same time the discount for lower iron (content) ores (in particular with impurities like silica and alumina) will suffer a relative increase,” JCP said.

“From a company perspective the biggest negative impact will be on Fortescue, which is a key reason why we maintain an underweight/short position in this company. BHP and Rio remain highly profitable at our reduced iron ore price forecasts.”

As usual, this misses the point, although it’s probably the paraphrase’s fault. It’s not about remaining profitable. It’s about rate of change in profits. Every major iron ore producer is mis-priced for $80 iron ore and FMG is in a world of pain in a Q3 destock scenario.